Valid until the market close on July 31, 2026

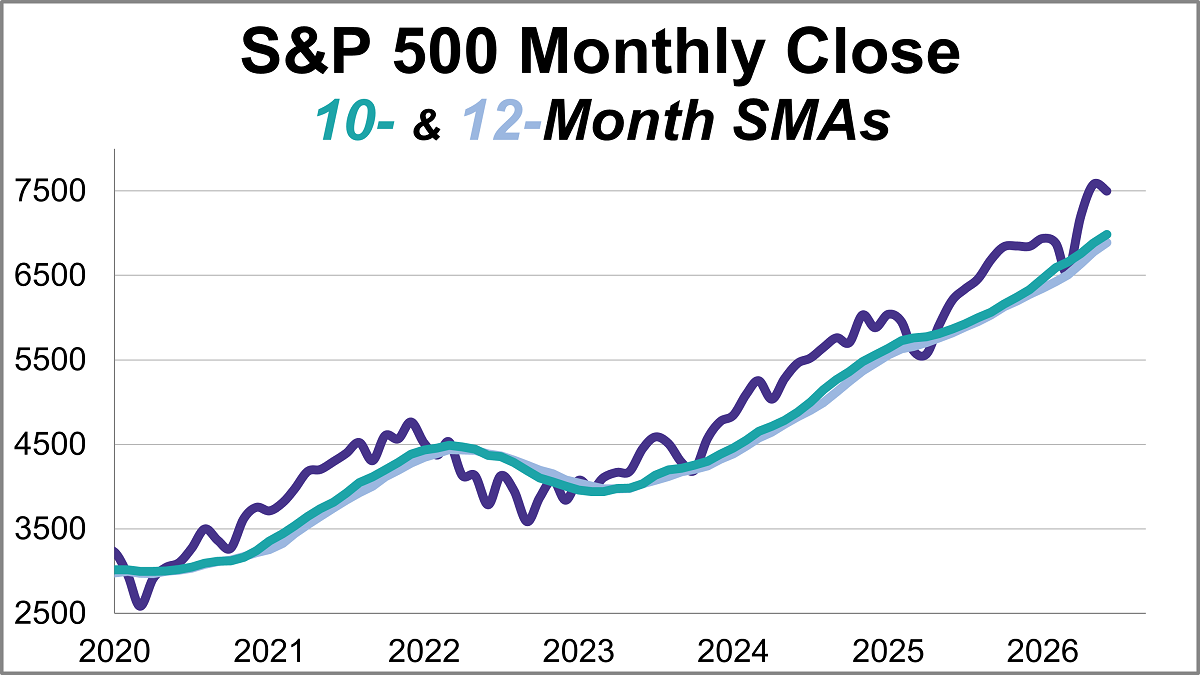

This article provides an update on the monthly moving averages we track for the S&P 500 and the Ivy Portfolio after the close of the last business day of the month.

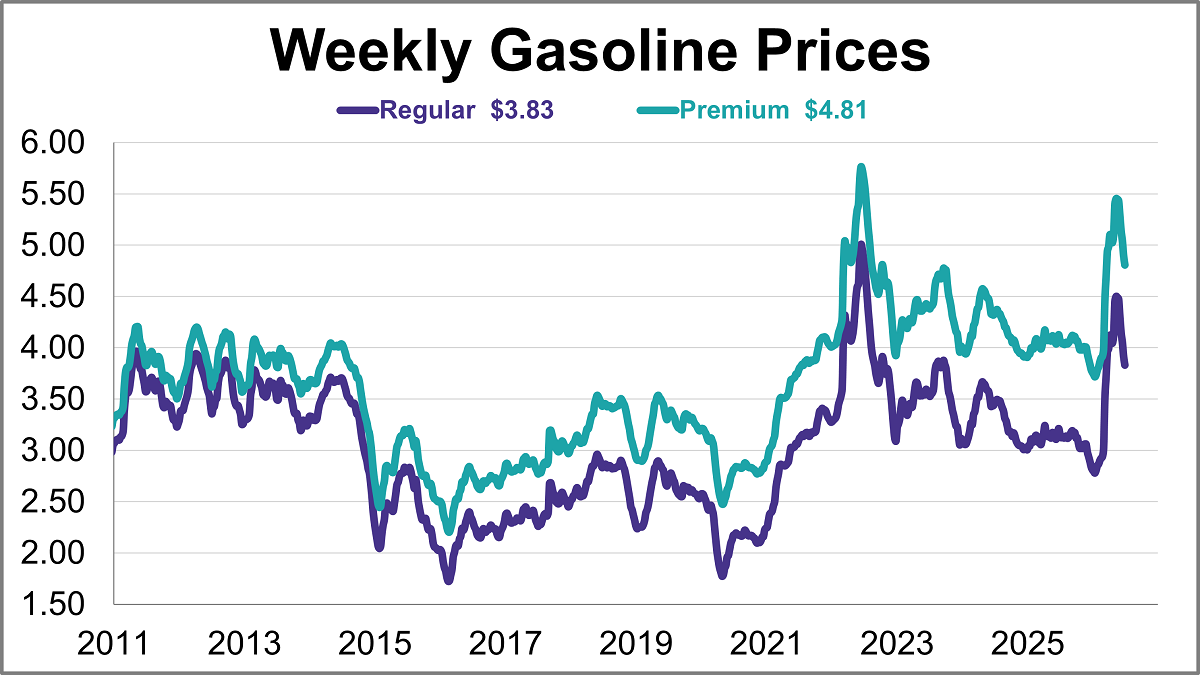

Gasoline prices fell for a seventh straight week, reaching their lowest level in 3.5 months. As of June 29th, weekly prices were down 8 cents for regular and down 9 cents for premium gasoline.

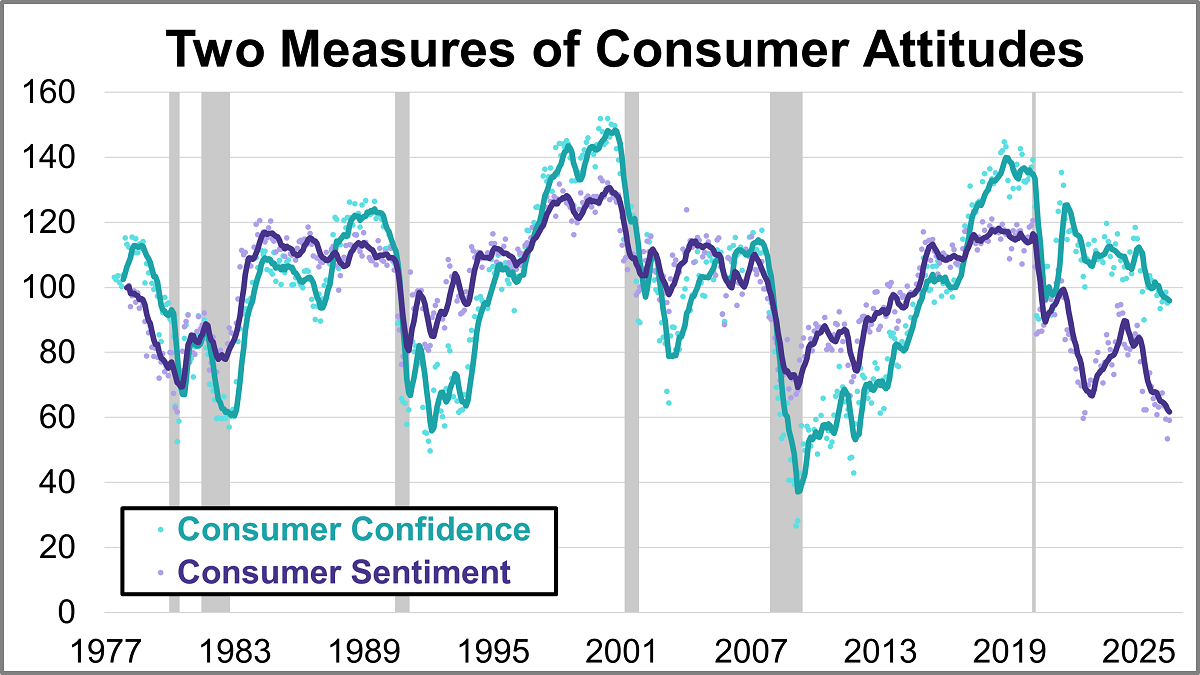

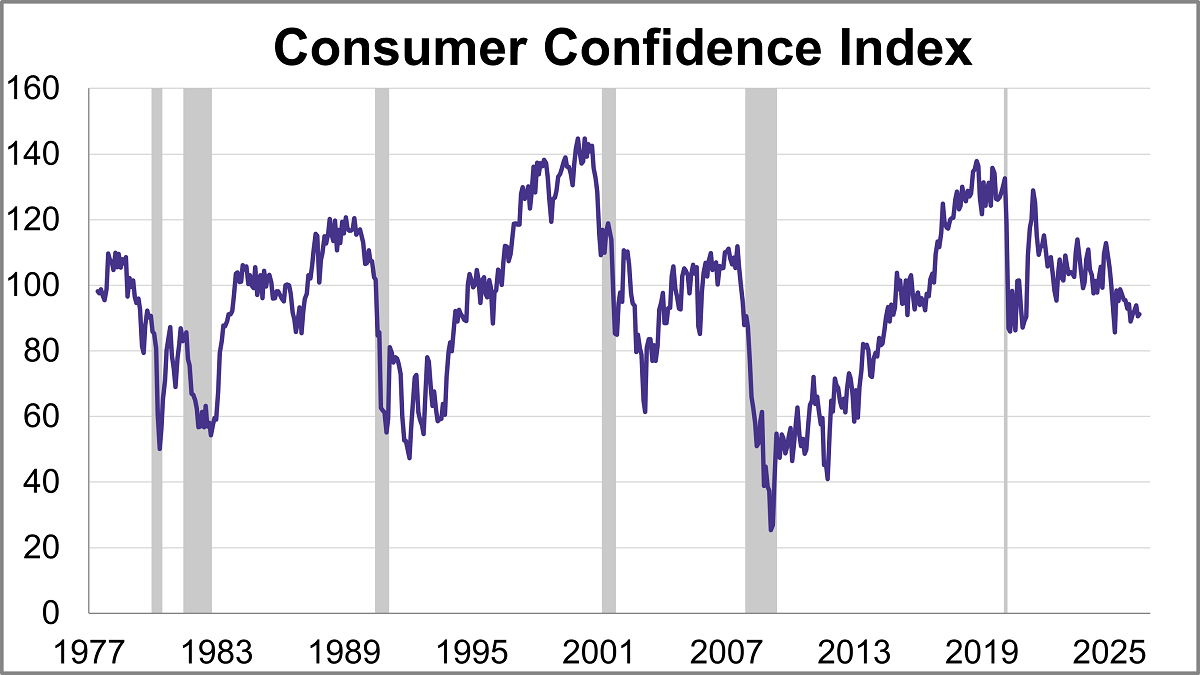

What are consumers thinking about the economy? Their collective mood offers crucial clues for businesses, investors, and policymakers alike. In June, the two leading benchmarks, the University of Michigan’s Consumer Sentiment Index (MCSI) and the Conference Board’s Consumer Confidence Index (CCI), offered similar views with both showing slight improvement despite ongoing inflation concerns.

The OBBBA created something the industry rarely gets: a defined planning window without a hard deadline attached. Exemptions are historically high, the law has no sunset, and there's a real body of existing work that needs revisiting. The advisors who treat this as an opportunity, rather than waiting for a client to ask, will drive much stronger outcomes compared to those who don’t.

Even people whose money beliefs and behaviors align more closely are not necessarily an ideal match. Partners whose predominant money scripts fall into the money vigilance category may both track expenses, openly discuss finances, and hold similar values around saving.

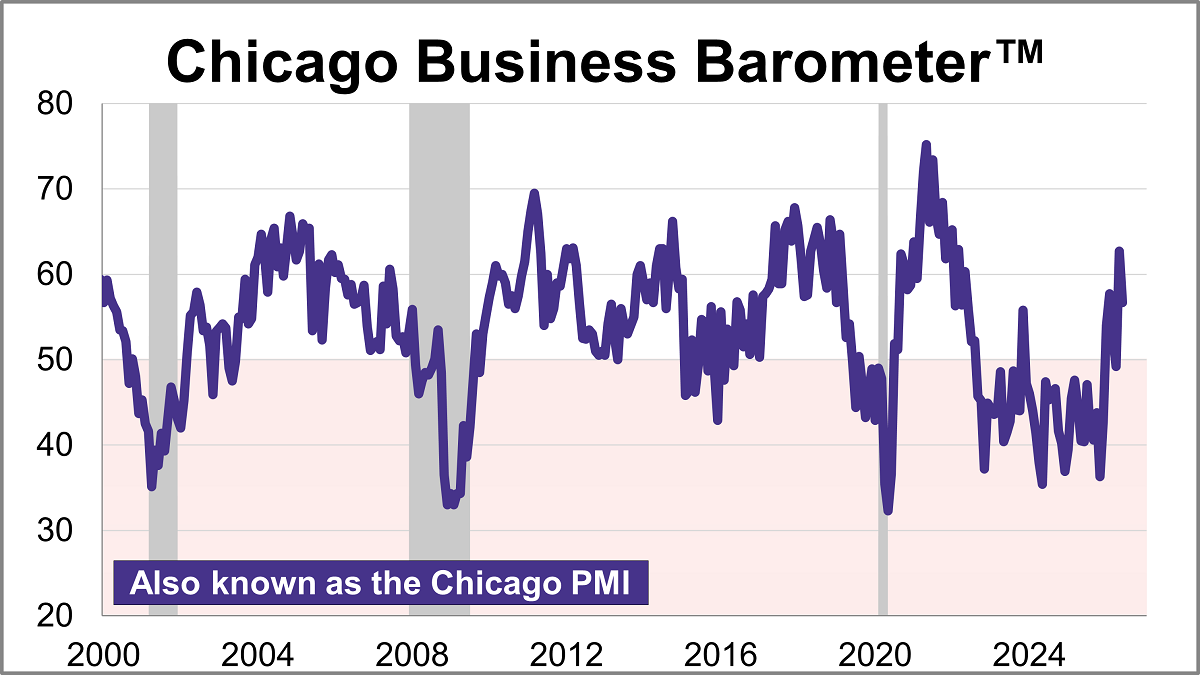

The Chicago Purchasing Managers’ Index cooled 6.0 points in June to 56.7, signaling an expansion in regional business activity for a second straight month. The latest reading was higher than the projected 55.7.

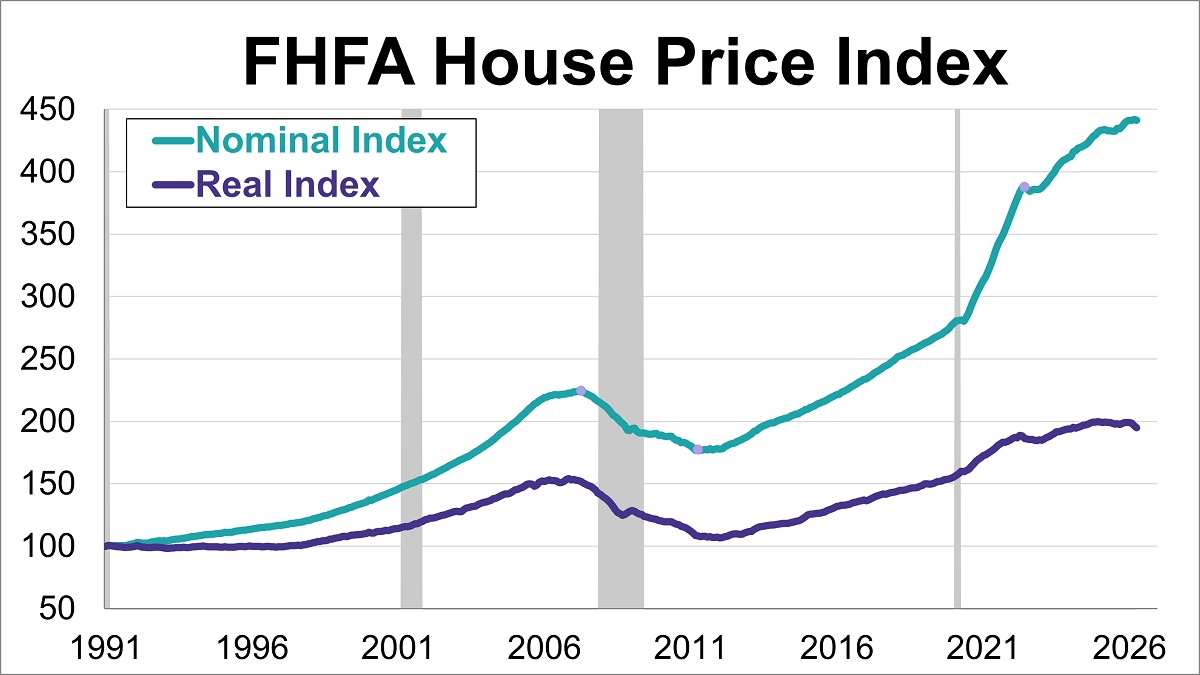

The Federal Housing Finance Agency (FHFA) House Price Index (HPI) retreated in April, falling 0.1% from the previous month's record high to 441.4.

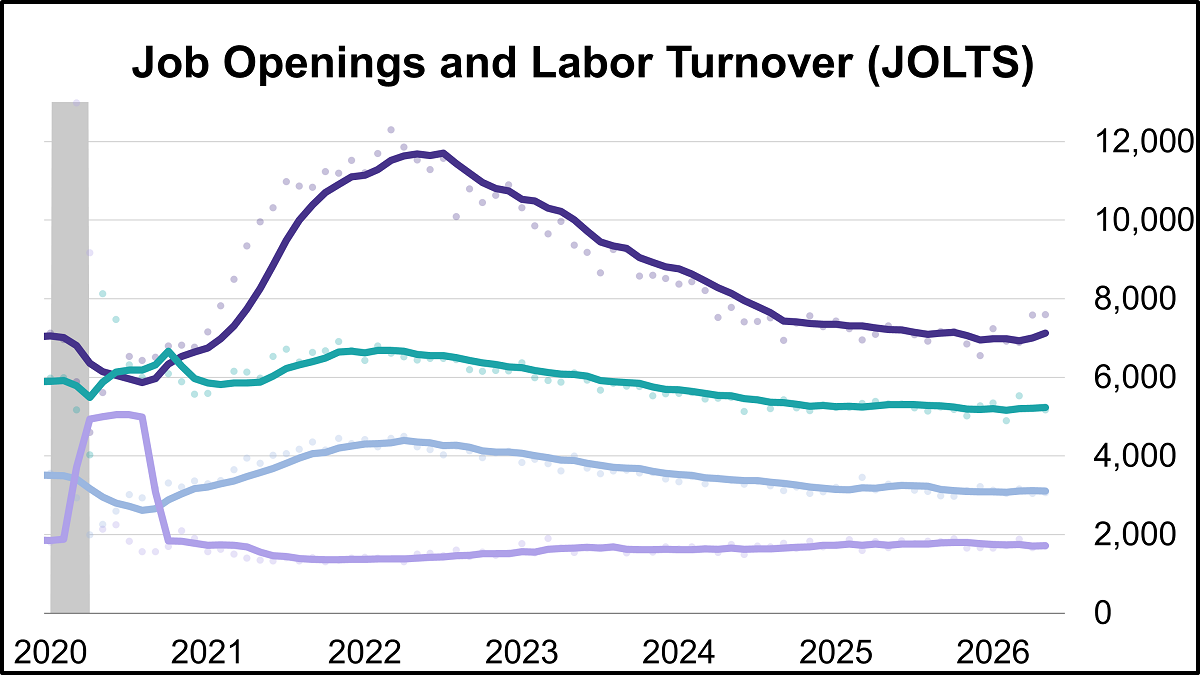

Job openings reached their highest level in two years in May, hitting 7.594 million vacancies according to the latest Job Openings and Labor Turnover Survey (JOLTS). The latest reading was higher than the projected 7.280 million openings.

The Conference Board's Consumer Confidence Index® inched up in June, rising 0.6 points to 91.2. Despite the improvement, the index came in below the forecast of 94.4.

These are dark days for free-market economists when one of the few areas of bipartisan consensus is for a terrible idea: Both Vice President JD Vance and Senator Bernie Sanders want the federal government to take an explicit stake in AI firms.

The ETF ecosystem is always changing and growing. Thanks to the ETF’s flexibility, transparency, and tradability, it can help investors achieve plenty of bespoke goals. That even includes investing with an eye towards philanthropic causes as with philanthropic ETFs ASD and DUTY.

Oil headed for the biggest quarterly decline since the pandemic as flows through the Strait of Hormuz accelerated following progress on a peace deal, with Morgan Stanley warning of a potential glut ahead.

Chip stocks are heading for their best quarter ever, extending an extraordinary start to the year driven by insatiable demand for artificial intelligence equipment. But after recent jitters sent the stocks tumbling, investors are wondering how much further the rally can go.

A sharp rise in the dollar may emerge as one of the biggest “pain trades” in the second half of the year, according to HSBC Holdings Plc.

Meme mania swept through Wall Street in 2021. Retail investors gathered on social media and coordinated trading strategies to short squeeze high-profile hedge funds.

The money is REAL. The question was never whether it exists. It’s who’s spending it, and what they borrowed to do it. When the wall of cash and the bottom half finally commit to risk at the same moment the Fed turns hawkish, that’s not the start of something. That’s the part of the cycle where the careful investor gets paid to be careful.

Ten years ago this week, the world watched the United Kingdom vote to walk away from the European Union. While the political class was clutching its pearls and every talking head on television was promising Armageddon by Christmas, I told you something different.

Alan Greenspan passed away last week at the ripe old age of 100. Other than presidents, few Americans have wielded as much power in the arena of economic policy as Greenspan did during his roughly eighteen years and five months at the helm of the Federal Reserve.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

Despite strong gains in 2026 so far, commodities have remained supported by constrained supply, resilient demand and long investment lead times, pointing to a cycle that seems to remain fundamentally intact.

Whether you’re a seasoned RIA owner looking to accelerate organic growth or a next-gen Advisor building your practice from the ground up, the same fundamentals apply: say clearly who you help, show up consistently where prospects look, and make sure your online presence tells the right story.

Investing is hard enough - This video explains why avoiding overpaying for stocks is one of the most important principles of successful long-term investing. Chuck Carnevale argues that while investing is never risk-free, many costly mistakes can be avoided by understanding a company's intrinsic value rather than reacting to market emotions.

A widening confidence gap in non-traded investment vehicles is testing private credit valuations, sharpening the case for manager selection and diversification beyond direct lending.

It’s hard to believe we’re nearing the halfway point of 2026 – and what an eventful start it’s been. Markets have pushed through a geopolitically driven energy shock, rising inflation pressures and accelerating disruption from the artificial intelligence boom.

AI infrastructure spending is driving record equity market raisings and has lifted expectations for long-term GDP growth in the US. But what will happen to growth when the AI capex surge has peaked? Today’s elevated long-bond yields suggest that the market expects AI-related productivity gains to support faster growth over the longer term.

What has started to stand out more recently is not the opportunity itself, but the behavior forming around it. The conversation has shifted. It is no longer centered on understanding what is being built or how it will be monetized over time.

The top 10 active ETFs YTD by fund flows show some intriguing trends and successful names that may pique the interest.

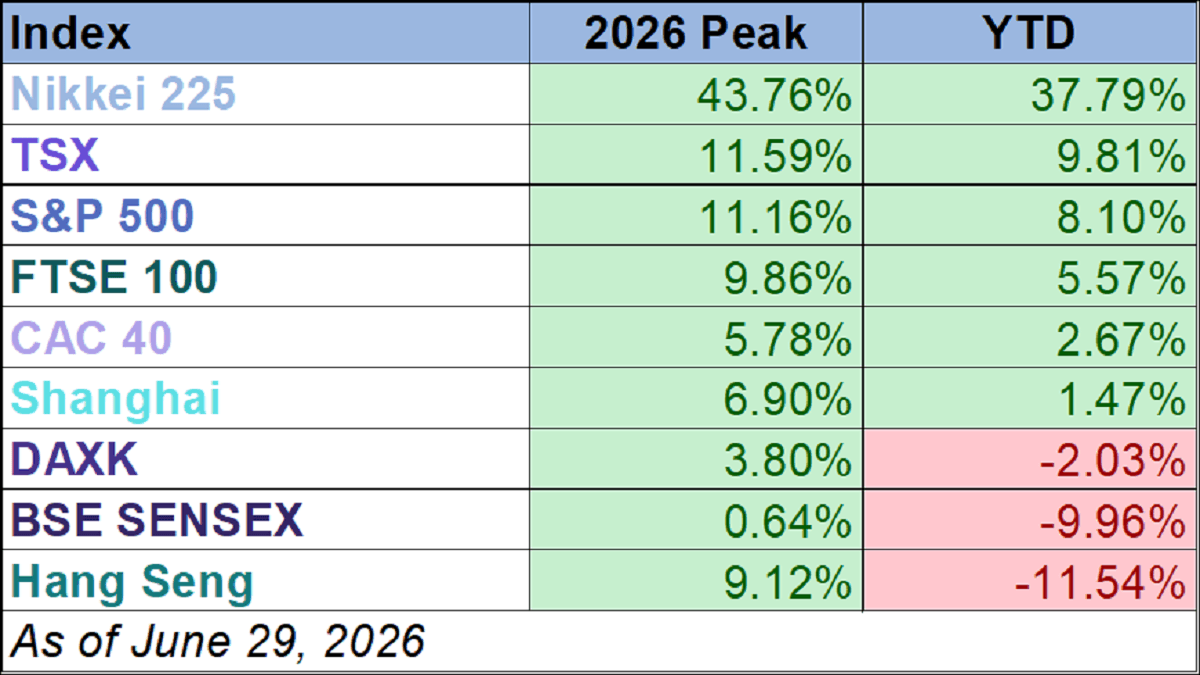

Six of the nine indexes on our world markets watch list posted year-to-date gains through June 29, 2026.

Join ProShares Global Investment Strategist Simeon Hyman and team for a discussion on how consistent share repurchases may reflect important characteristics of a company.

Markets will continue to shift. Headlines will change. Volatility will come and go. What endures is the value of having a thoughtful, well-constructed plan. Planning creates structure during uncertain periods and helps clients stay focused on long-term goals instead of short-term noise.

Jesse Livermore’s prolific trading stories about the fortunes he made and lost are well documented in two books. While his career was marked by the incredible volatility of his wealth, and some consider him a failure as he died broke, his market knowledge is invaluable. Accordingly, we share his 21 market rules.

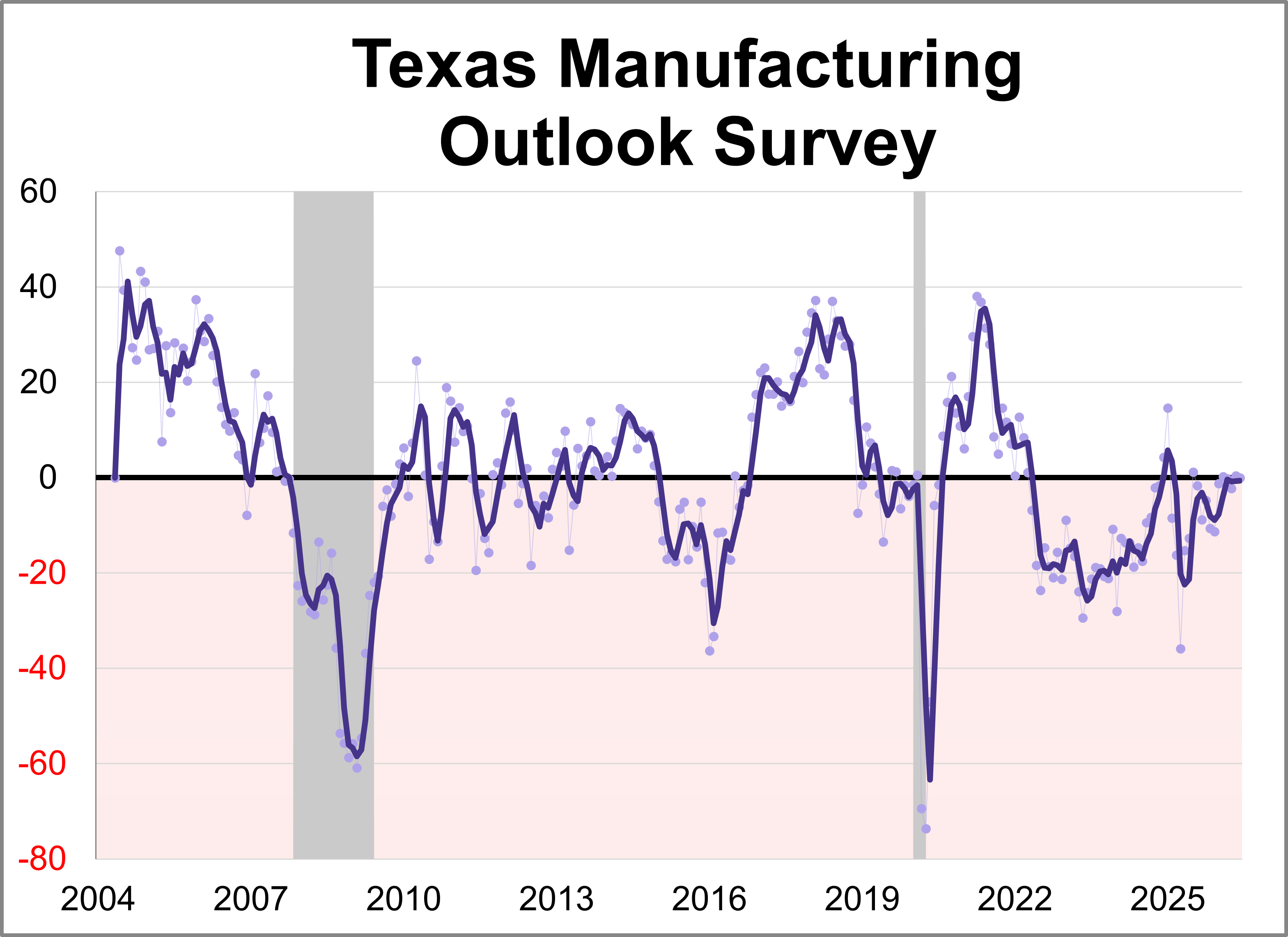

The Dallas Fed released its Texas Manufacturing Outlook Survey (TMOS) for June. The general business activity index fell 0.4 points to 0.0, indicating slower growth of manufacturing activity and stable business conditions perceptions.

The way the SPIVA U.S. Scorecard evaluates performance is not well aligned with the experience of investors. Adjusting for this reveals a more balanced view of active fund performance. While active and passive U.S. equity funds perform similarly, active bond funds tend to outperform.

Wall Street bankers are on a high after record-setting offerings from SpaceX and Google parent Alphabet Inc., lifting expectations for deal activity in the rest of 2026. More deals are on the way, including a steady stream of initial public offerings in the coming weeks, and a potential mega-deal for Anthropic PBC as soon as October.

European firms in critical sectors like nuclear energy and quantum computing are flocking to the US, despite efforts by European authorities and bourses to make the region’s markets more appealing and accessible.

Microsoft Corp. shares are heading for their worst month in years as investors continue to fret about how the software giant will fare in a world marked by artificial intelligence.

Social Security is now just six years away from insolvency, according to the latest annual assessment. Many in Congress might like to keep on ignoring the problem, as they have for years, but this won’t be an option much longer. Senators elected in November will see the system’s trust fund empty during their terms.

The Federal Reserve’s new chairman, Kevin Warsh, plans to convene no fewer than five task forces to review the central bank’s methods and operations. They will ask how the Fed can improve its communications, balance-sheet policy, use of data, understanding of “productivity and jobs in an era of transformation,” and delivery of price stability.

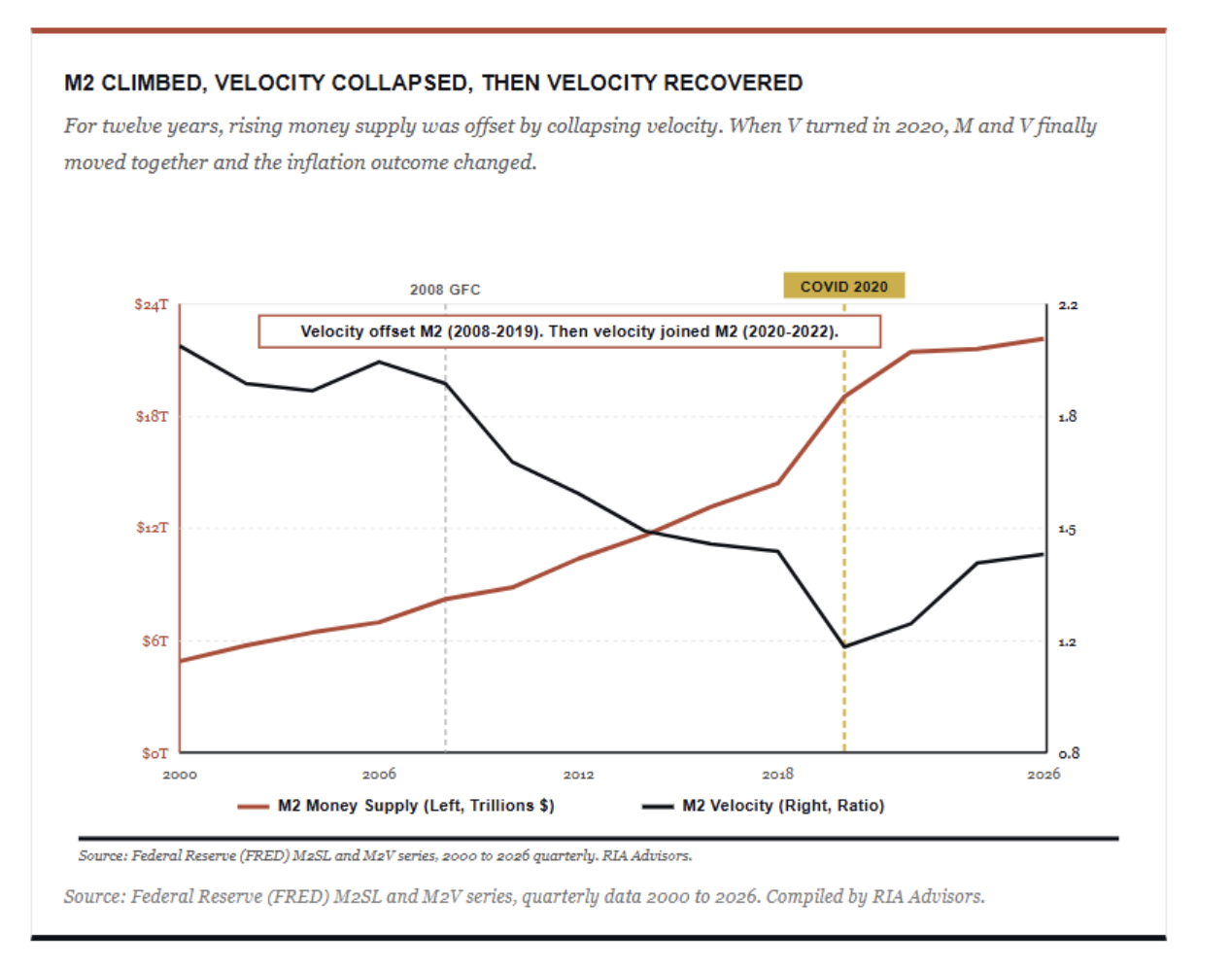

Friedman was reasoning from the equation of exchange, MV = PQ. Money times velocity equals prices times real output. It’s an identity, not a theory. Where it gets interesting is when you ask which variable does the work.

Transformative new technologies and geopolitical tensions have become powerful disruptive forces, redefining business models, global supply chains and the economy. These seismic shifts are upending competitive dynamics across industries and drawing trillions of dollars in capital flows that we believe are reshaping the sources of long-term equity returns.

The dominant theme this week was a tug of war between improving macroeconomic conditions and weakness in parts of the technology sector.

From our experience participating in Fed meetings, we know that the dot plot has never been universally embraced within the institution. The concern was not that it lacked informational value, but rather that markets interpreted it as a forecast, which was never its intended purpose. Forward guidance is meant to shape expectations and influence behavior, not to serve as a firm prediction of future policy decisions.

Markets have been hyper-focused on AI, crypto and buffer ETFs, but REIT ETFs have quietly staged an impressive comeback. The REIT terrain has shifted rapidly over recent years, and forward-looking investors and advisors have taken notice.

As expectations have shifted toward slower growth, higher inflation, and higher rates, investors have rotated back to sectors like large-cap technology and semiconductors, capable of delivering durable earnings in a tougher macro environment.

Circumstances since 2020 have repeatedly demonstrated how adaptable the economy is in the face of new challenges. We see no reason for that resilience to fade in the balance of the year.

During the past month, the ETF market has seen a wave of excitement surrounding a concentrated group of companies. While investors still want exposure to the tech giants that have dominated the past few years, the successful launch of SpaceX in early June created widespread anticipation for planned IPOs like Anthropic and OpenAI.

Last week’s data reaffirmed that inflation pressures remain the defining narrative across the economic landscape.

I’m hopeful new chair Kevin Warsh will help change the Fed’s inflation-tolerating institutional culture. Early signs look positive. Today we’ll talk about how insidious inflation is and why those who think a little inflation is fine should have their heads examined. It is not fine… for anyone.

The AI boom goes from strength to strength. Big technology companies are pouring hundreds of billions of dollars into chips, data centers and power-hungry infrastructure. One estimate puts annual AI infrastructure investment above $650 billion in 2025 and potentially over $800 billion in 2026..

Model portfolios have helped many advisors solve for scale. The next challenge is more nuanced: how do advisors keep that scale while delivering more personalization, tax awareness and differentiated value to clients?