Bitcoin and other cryptocurrencies didn’t do much of anything following last week’s crypto summit at the White House.

As we wade into March, market volatility is at the forefront, leaving investors grappling with uncertainty surrounding tariffs and mixed economic signals. Though the S&P 500 experienced a bounce towards February's end, it slipped 1% overall, revealing lingering challenges for iconic tech stocks and the broader equity landscape.

As the consumer goes, so goes the U.S. economy. Consumers make up roughly 70 percent of U.S. GDP.

Volatility across financial markets has become a persistent theme in 2025. The recent volatility has stemmed from a range of factors, including:

For decades, the U.S. dollar’s dominance has rested on two pillars: America’s deep capital markets and its global security alliances. Today, both are under strain.

Economic growth, earnings performance, and rising fiscal spending coupled with "America First" policies are driving international stock markets.

Global investment themes are shifting toward infrastructure, cybersecurity and energy expansion as demand outpaces supply in key sectors.

Short-term deadlines will complicate long-run plans.

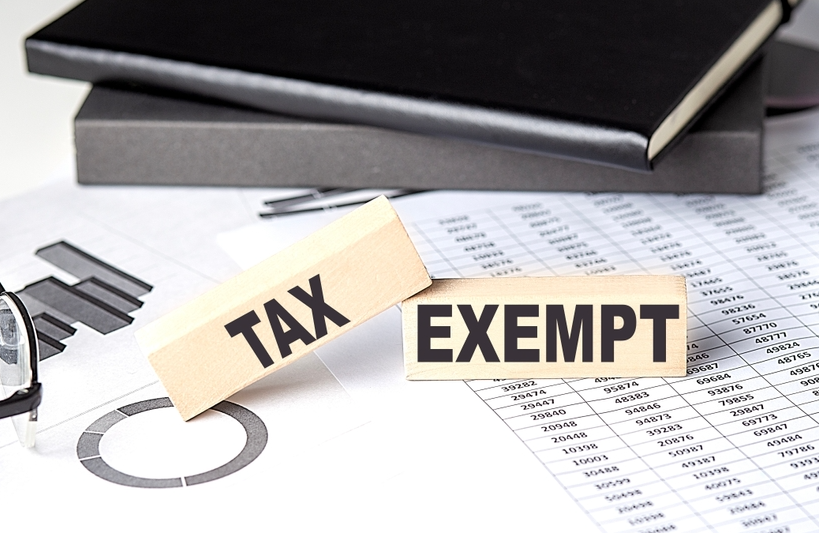

Parametric’s tax optimized ladders (TOL) solution may help to enhance after-tax yield by seeking to optimize the allocation between tax-exempt and taxable bonds, based on an investor’s own tax rate and the relative value between sectors.

The EV shakeout is underway. When the dust settles, only a few players will remain. Many more will be relegated to the scrapyard of failed ambitions.

Costco's earnings may have disappointed in the near-term, but the company may be in a prime position to perform during a tariff showdown.

Stock/bond divergence allows investors to reap the benefits of portfolio diversification, giving bond exchange-traded funds credence.

At the start of the year, our Investment Strategy Committee outlook was positive for both the economy and the equity market, supported by strong consumer, labor market, and corporate fundamentals.

Though mergers and acquisitions were expected to roar back in 2025 thanks to the new administration, uncertainty around Washington policy appears to be holding back new deals.

Trade policy clarity is a long way off.

Last week brought another wave of volatility to the markets, with investors grappling with mixed economic signals, geopolitical developments, and ongoing trade policy uncertainty.

It is true that tariffs are a tax. It is also true that tariff policies have been volatile…on and off again…different carve outs…different countries…phone calls that change things. All of this clearly has an impact on the market. So, we are not surprised to see stock market volatility.

There’s a lesson for financial advisors in this story. If you demonstrate a genuine intention to engage and connect with your female clients, it will build relationships that could drive the growth of the business for years to come.

Investor’s bearish sentiment has surged to levels that generally align with previous market corrections and crashes.

Last week's economic reports presented a narrative similar to what we’ve seen over the past few months: growth coupled with concerns.

I will again join forces with Ed Easterling of Crestmont Research to explore this data more deeply. Currently we have several powerful trends that have combined to create a nirvana-like market.

The U.S. has poured more than $120 billion into Ukraine since its war with Russia began three years ago, but with a new administration in Washington, that support is grinding to a halt.

The European Central Bank will likely continue to cut interest rates, but future decisions could be more contentious.

On March 4, 2025, the Trump administration imposed tariffs of 25% on Canada and Mexico and increased tariffs on Chinese imports to 20% from the previous 10% imposed earlier in the year.

We highlight some underreported positive developments that could keep economic growth on track and support higher equity prices in the months ahead.

On the latest edition of Market Week in Review, Senior Investment Strategist and Head of Canadian Strategy, BeiChen Lin, discussed how markets are reacting to U.S. trade policy uncertainty.

Cambria Investments CIO and founder Meb Faber explores David Swensen’s legendary investment strategy at Yale’s endowment, comparing its long-term performance to traditional portfolios and examining whether individual investors can replicate its success.

Q4 company earnings offered a lot to cheer at the start of the year, even as U.S. stocks contended with bouts of volatility.

As the debate heats up on Capitol Hill about extending the TCJA, there are several issues to watch including potential SALT cap relief and whether more tax cuts will be added to the final bill.

In this video Chuck Carnevale, Co-Founder of FAST Graphs, a.k.a. Mr. Valuation will go over three super growth stocks that Chuck is often asked to cover but reluctant to because of valuation issues.

One month into President Donald Trump’s new term, financial markets are adjusting to a rapidly shifting economic and policy environment. Investors are watching closely as tariffs, interest rate expectations and regulatory changes take center stage.

Volatility is back in town. Tariff jitters and concerns about growth and inflation have resulted in an S&P 500® dip and the Cboe Volatility Index (VIX) jumping above 20. Investors grapple with a very sanguine backdrop painted by the fourth-quarter earnings season and policy uncertainty.

The municipal bond tax exemption is back in focus. We believe the threat to infrastructure investment outweighs the modest revenue benefits, which could keep the risk of elimination or significant curtailment low.

In his testimony before the House Financial Services Committee February 12, Federal Reserve Chair Powell was questioned about why mortgage rates had not declined.

The "2025+ Outlook Report" offers an analysis of how robotics, AI, and healthcare technology are converging to reshape industries globally.

U.S. fixed income ETFs garnered strong flows in February, uncovering insights into investor behavior and risk appetite in 2025.

Ever since interest rates got up off the floor in 2022, there’s been increased interest in credit, and that’s why I’m devoting this memo to it. It’ll come a little closer than usual to “talking my book,” but I think the subject justifies that.

The value today of quality bond exposure in your high yield portfolio.

Opportunities have increased significantly in frontier markets debt as more countries have made a conscious effort to open their capital markets to international investors and currencies have become more fairly valued.

Treasury yields have been falling for weeks. Yet inflation expectations remain high and recent growth data have been fairly strong—not a traditional backdrop for declining yields. What's happening?

Though the new US policy focus is on oil and gas, wider opportunities still beckon.

One of the most referenced valuation measures is Dr. Robert Shiller’s Cyclically Adjusted Price-Earnings Ratio, known as CAPE.

Many ASEAN members punch above their economic weight in international trade. But their power may also make them targets in the mounting global trade battle.

As daily headlines drive volatility, the market has avoided overreacting thus far.

With U.S. tariffs on Mexican and Canadian imports now in effect, yesterday’s risk-off market mood continued today. Both Canadian and U.S. equities modestly sold off.

High fiscal deficits from tax cuts and tariffs raised concerns about inflation. However, markets have since shifted their focus.

We view quarterly earnings season as a critical checkup on how markets are handling current challenges.

We manage risk tactically over the short-term by investing across a broad array of themes and asset classes including cash.

Unlike most of the rest of the world, I will attempt to minimize all there is to say about the beginning of the next 4 years, as the persistent yack and what to make of it reverberates in all corners of the financial globe.

According to Research Affiliates’ Asset Allocation Interactive (AAI) online capital market expectations tool, U.S. large-cap equities are expected to yield 3.4% annually over the next 10 years compared to 9.1% for EM equities and 7% for REITs. This left many webinar participants wondering, How does this extra return square with these assets having similar betas?