Household, corporate and bank balance sheets are more resilient today than during past crises.

Economic slowdown but no recession!

We normally start our letters on a positive note.

We live in unprecedented times.

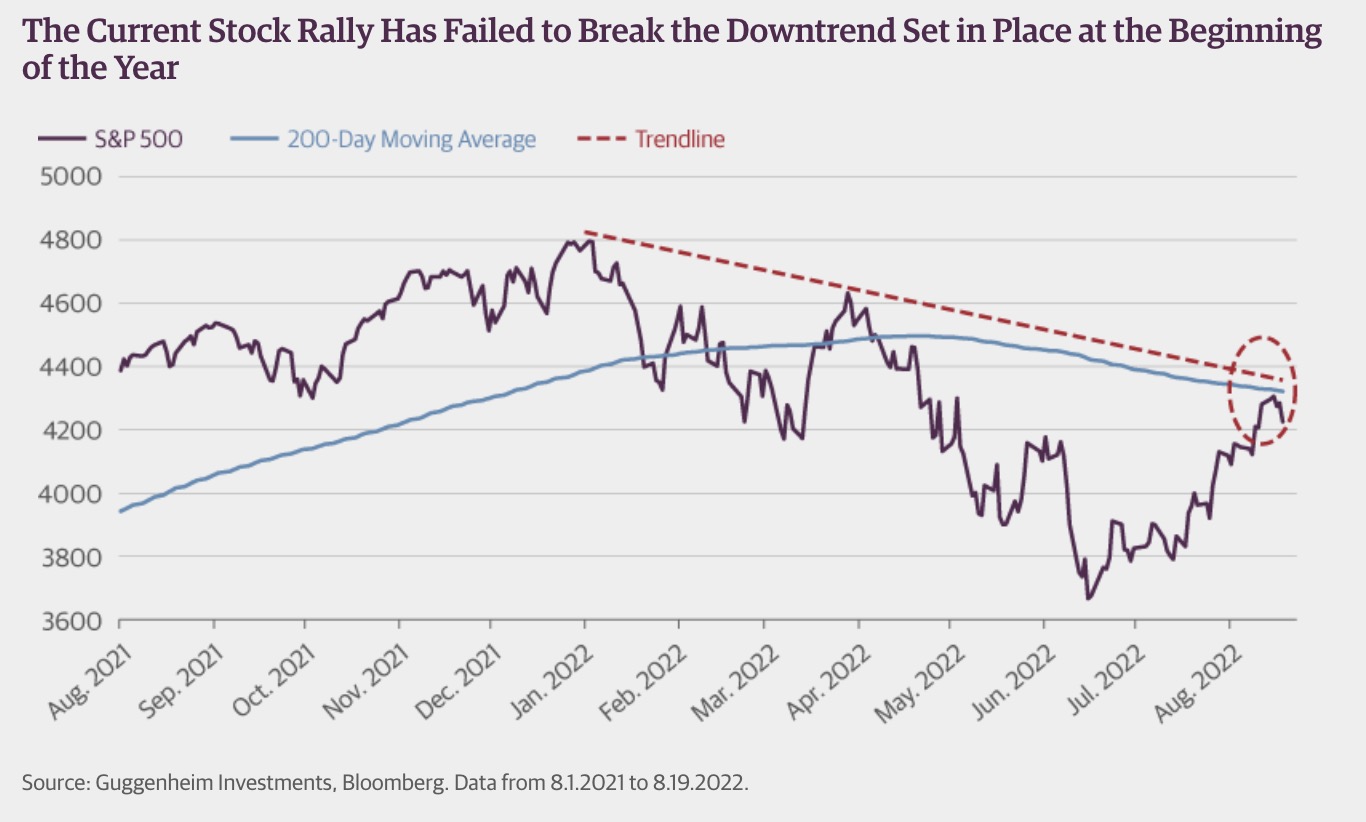

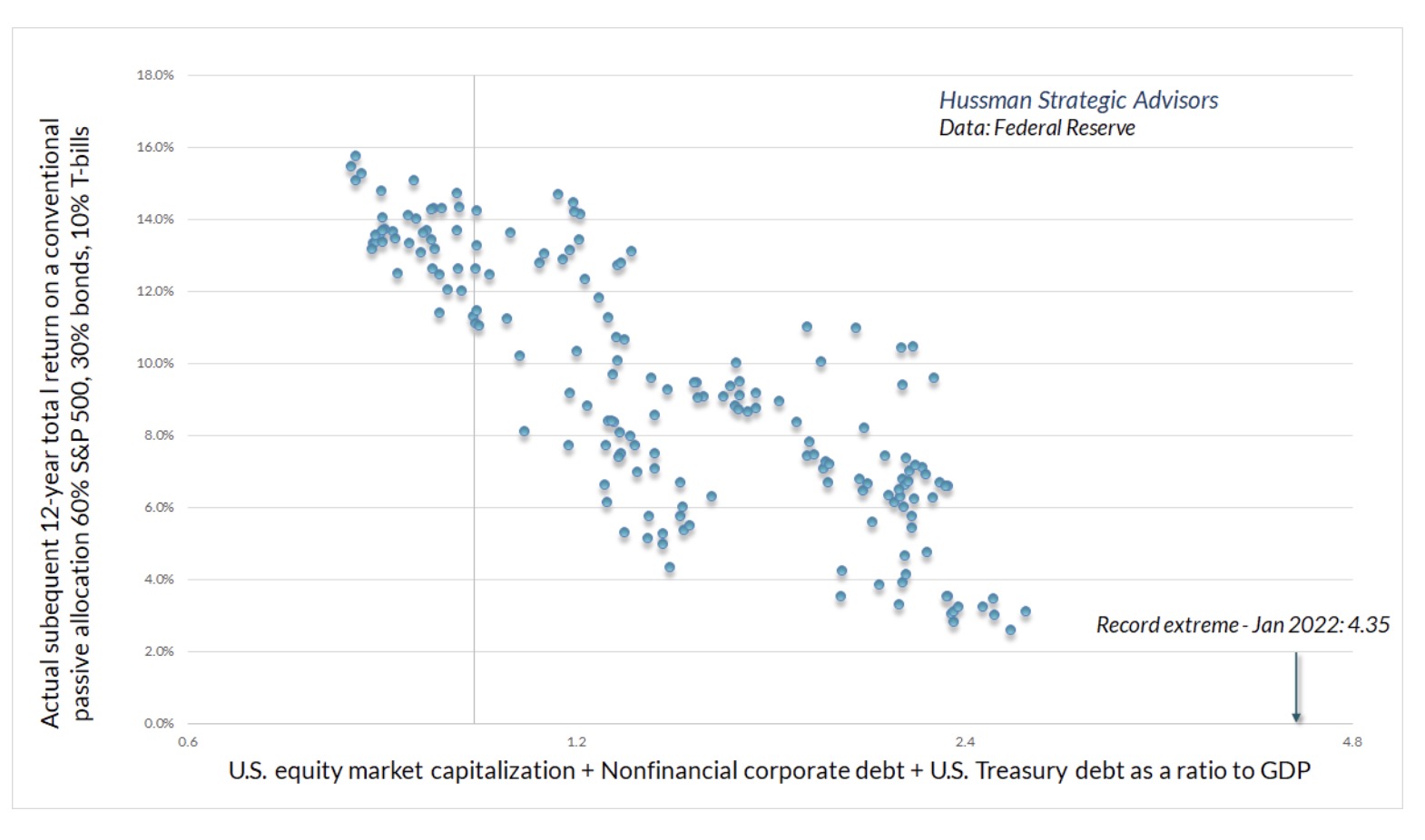

Deeper losses for equities may lay ahead.

Rick Friedman from GMO’s Asset Allocation team offers the following comments about the updated forecasts.

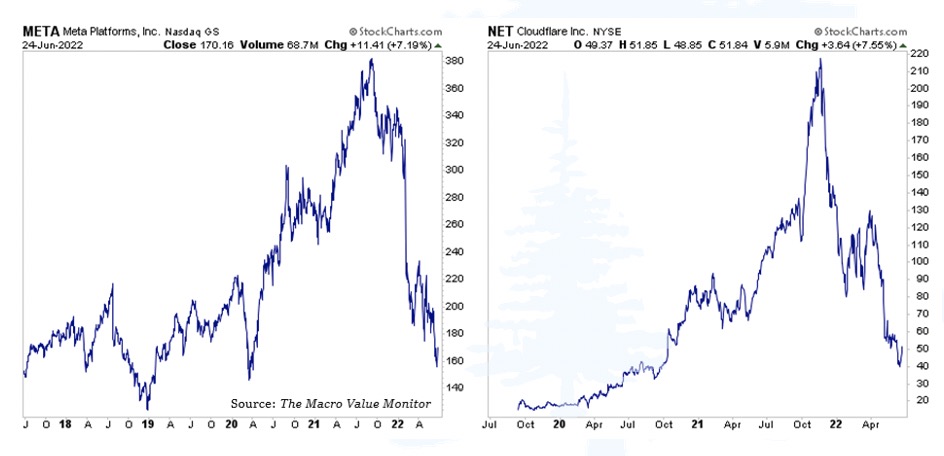

This is part 1 of Volume I Issue VI of the Macro Value Monitor, a publication focusing on Monetary History, Market Myths, Investing Legends, and Real Global Value.

Winter is coming for Europe, and energy prices are soaring as international sanctions on Russia curb the supply of natural gas, on which many European Union (EU) countries have increasingly become dependent.

Our own government cannot afford a short end of the curve much higher than it is now, and our own fiscal and monetary decisions have held down the long end of the curve in what I believe is a multi-decade period ahead that is best referred to as “Japanification”

U.S. Economist Matt Bush discusses the fast-moving economic data, and Managing Director Aditya Agrawal reports on developments in the Agency MBS sector.

July offered investors a slight reprieve from the market volatility that has characterized the first half of 2022.

Given all the confusion in the world around COVID, supply chains, inflation dynamics and war, there are lots of potential externalities that could resolve themselves unexpectedly.

We have had a rally in equities, and successfully traded Biotech on the way up, per our last article.

Growth stocks can be very powerful long-term investments.

The Northern Trust Economics team shares its outlook for key markets in the month ahead.

In the face of what was the largest first half decline in the S&P 500 since 1970 and the worst ever start to a year for high yield bonds, short duration credit was not immune

U.S. stocks are subdued following yesterday’s release of the minutes from the Fed’s July monetary policy meeting.

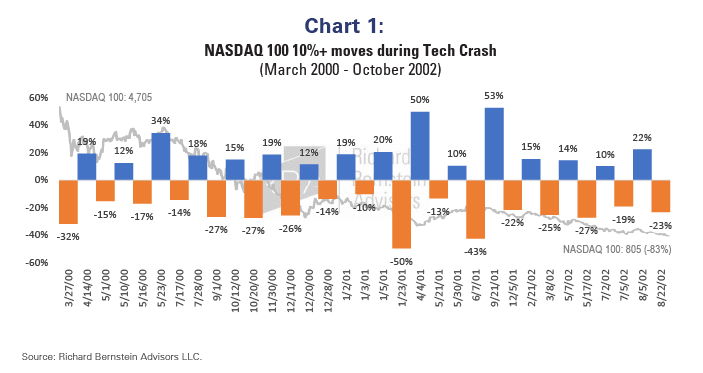

It is my belief that the bear market is over.

With the ever-increasing need to decarbonize our global economy, investors are now focused not only on the why behind decarbonizing, but also the how.

If you are looking for safety when buying stocks, consider stocks with strong balance sheets, and GOOGL has one.

Pinterest is a virtual bulletin board for finding and sharing ideas for food, home, style, inspiration, and more.

The market contraction presents better opportunities than we’ve seen in years to generate income, which we balance against the need for resilience in the face of a potential recession.

As prologues go, the first six months of this year have been a doozy.

Bubbles don't deflate overnight and bear markets always signal a change in leadership, yet investors appear eager to jump back into owning prior cycle winners.

Over the weekend, we got a slew of data showing a generally weak economy.

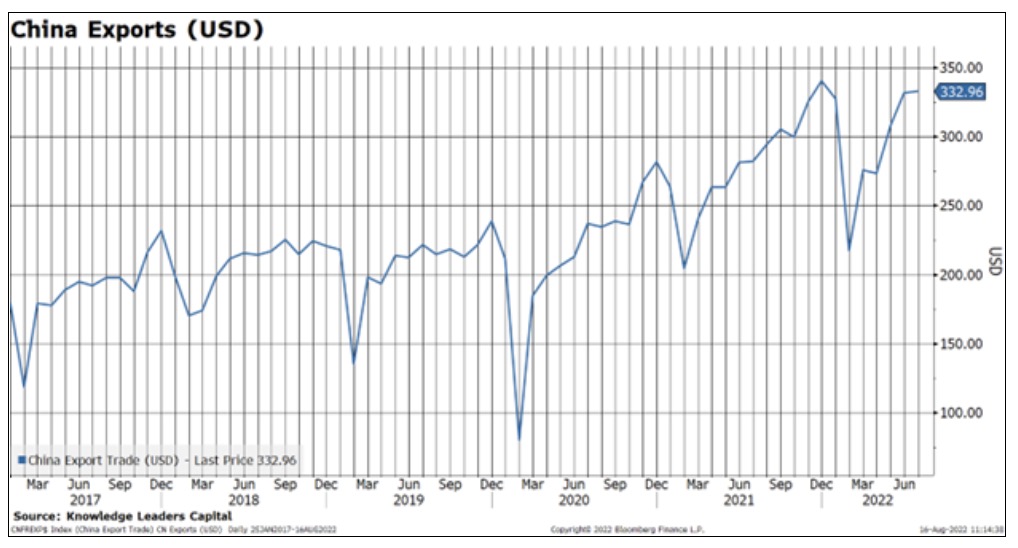

The Democrats in the Senate and House of Representatives narrowly passed the mis-named Inflation Reduction Act last week, which is expected to be signed into law by President Biden this week.

It’s been a tough first half of the year, with the MSCI All Country World Index down by 21.7% and the Bloomberg Global Treasury benchmark losing about 9% as of June 17.

We believe one of the hardest things to do in common stock investing is to hold winners for a long time. This is especially true with what are normally cyclical industries.

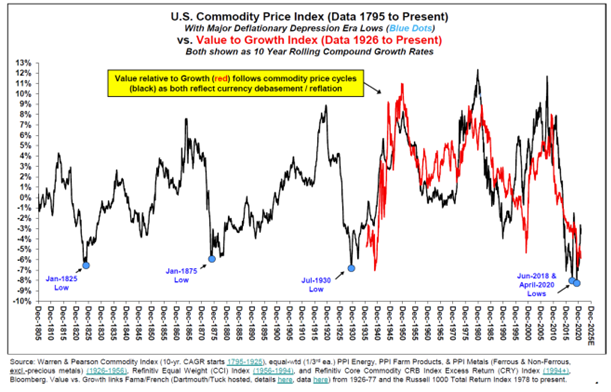

After more than 40 years of work in the financial markets, studying all the data I could get my hands on, I’ve found it to be universally true that those who argue “history doesn’t matter” have never actually studied history.

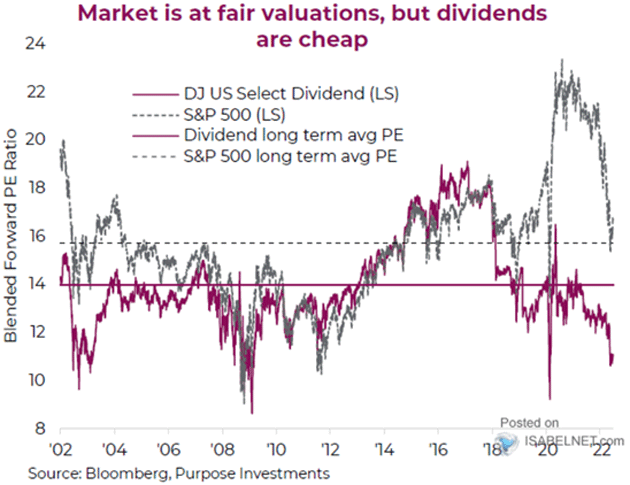

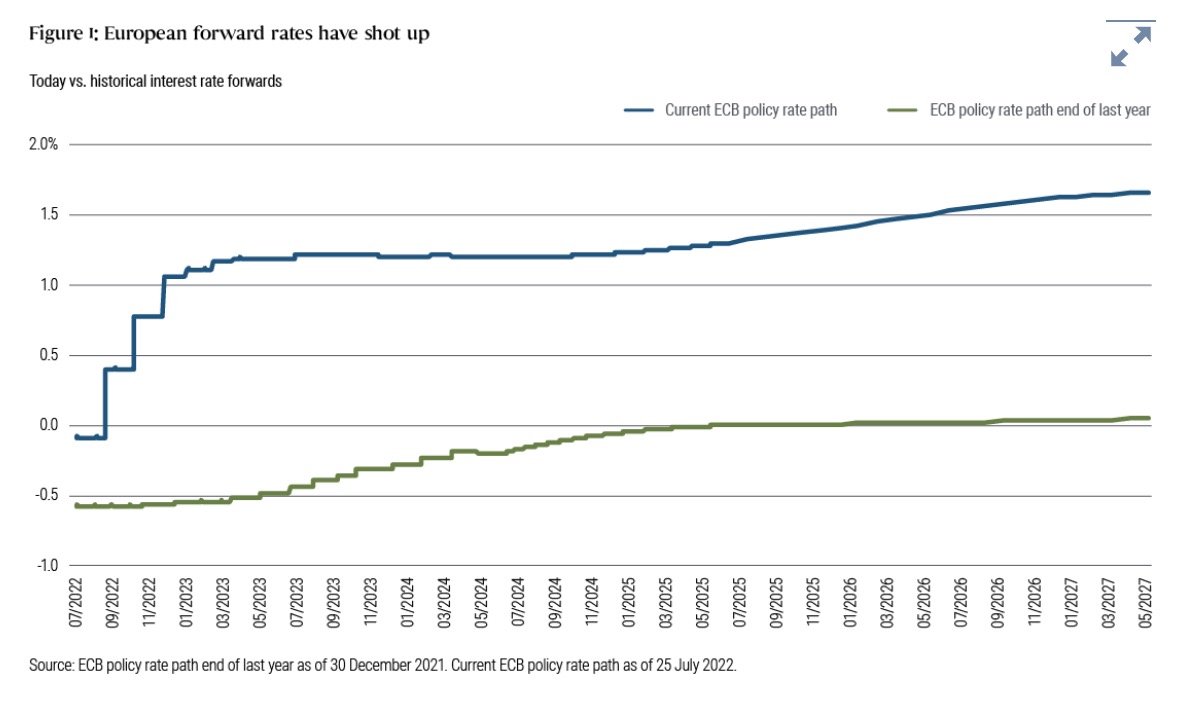

As the European Central Bank leaves negative policy rates behind, attractive valuations herald a much-improved total return potential.

Crude oil prices dropped substantially to start the week after the dollar rallied.

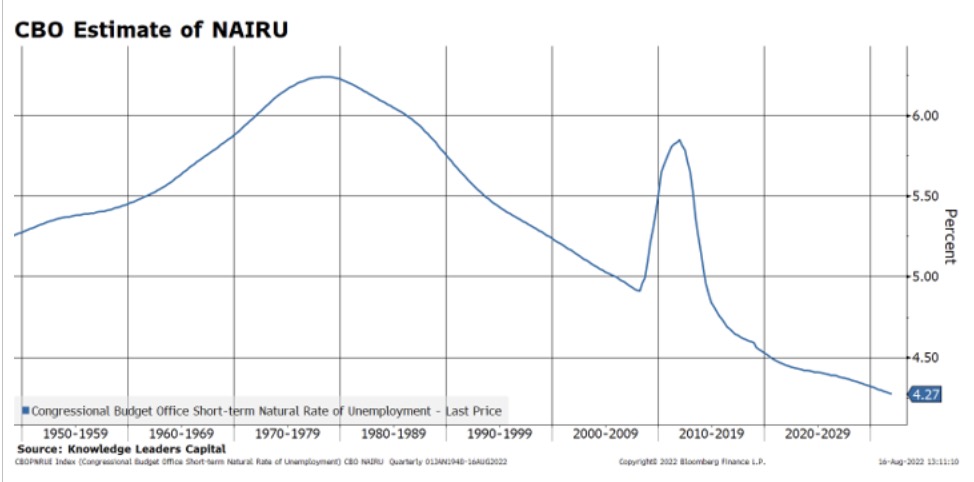

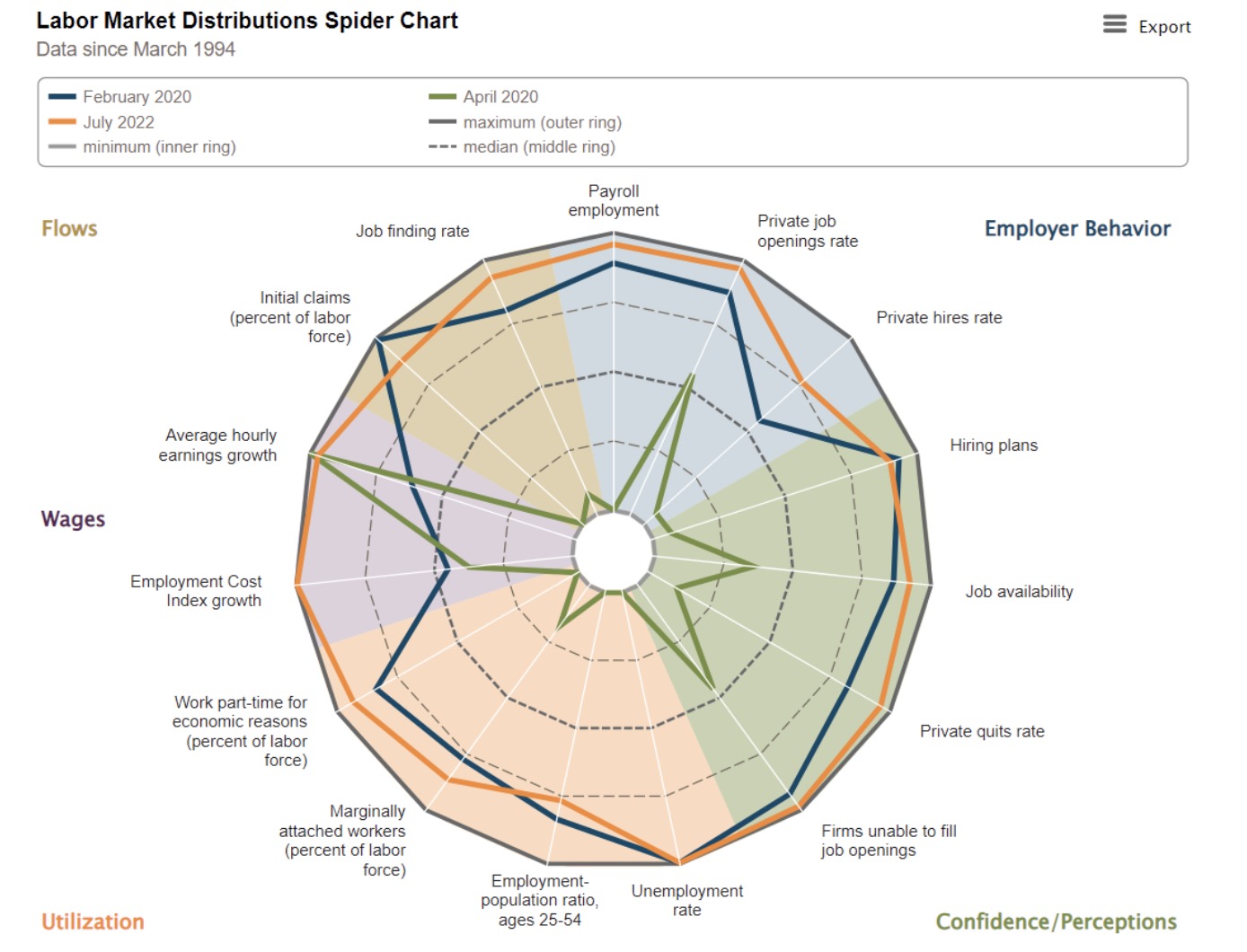

Labor force participation is the greatest shortfall in an otherwise thriving labor market.

Our last update was on August 1st.

U.S. stocks have come off the worst levels of the day and are threatening a move into positive territory.

Major EMs are more resilient to U.S. interest rate hikes today than they were in past cycles.

With less than three months left before the 2022 mid-term elections, it is officially silly season when it comes to interpreting economic reports.

Review the latest Weekly Headings by CIO Larry Adam.

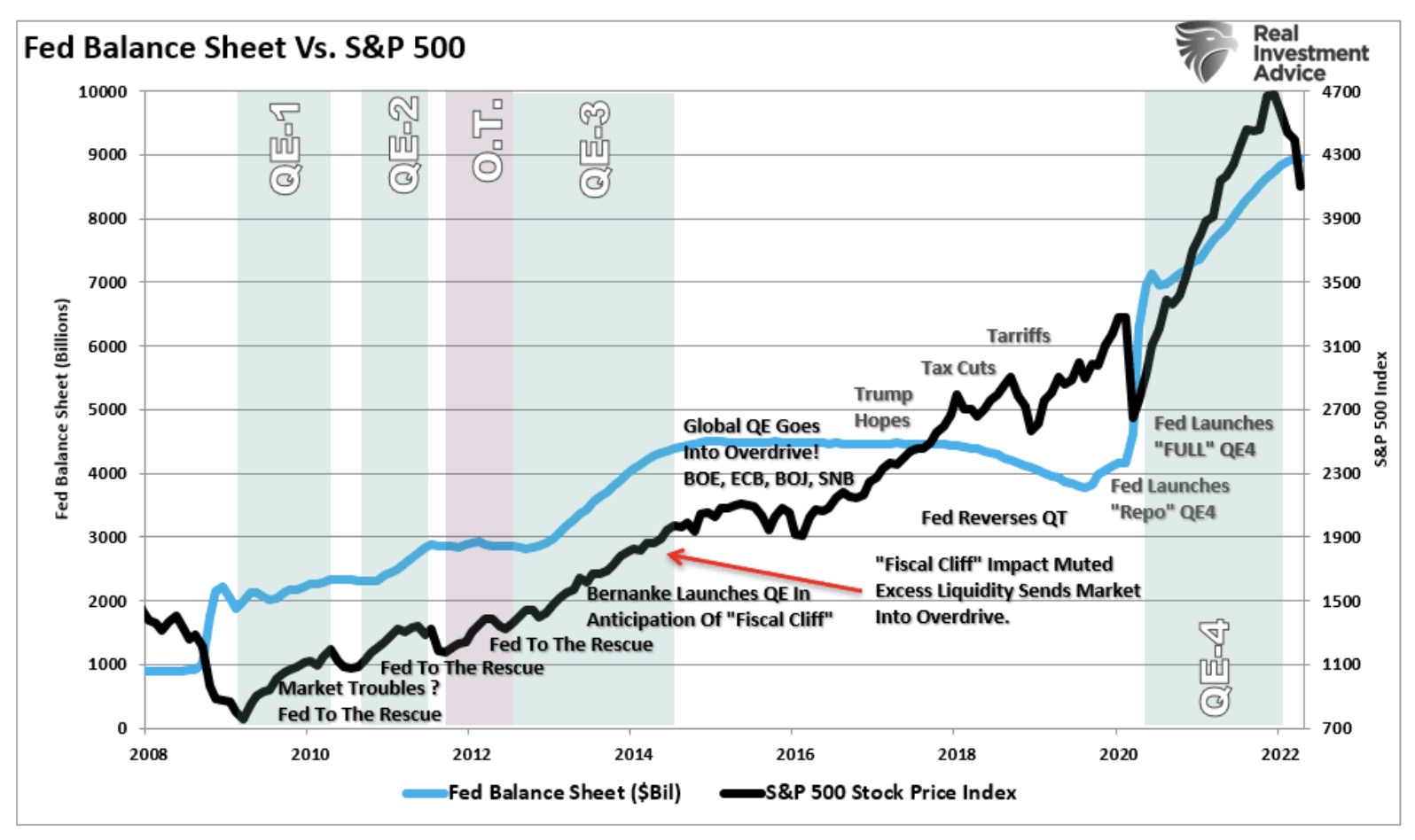

Pulling forward growth over the last decade remains the Federal Reserve’s primary tool for keeping financial markets stable while economic growth rates and inflation remained weak.

The bipartisan Creating Helpful Incentives to Produce Semiconductors for America Act, or CHIPS Act, was signed into law this week, setting aside $52 billion to boost domestic semiconductor research and production.

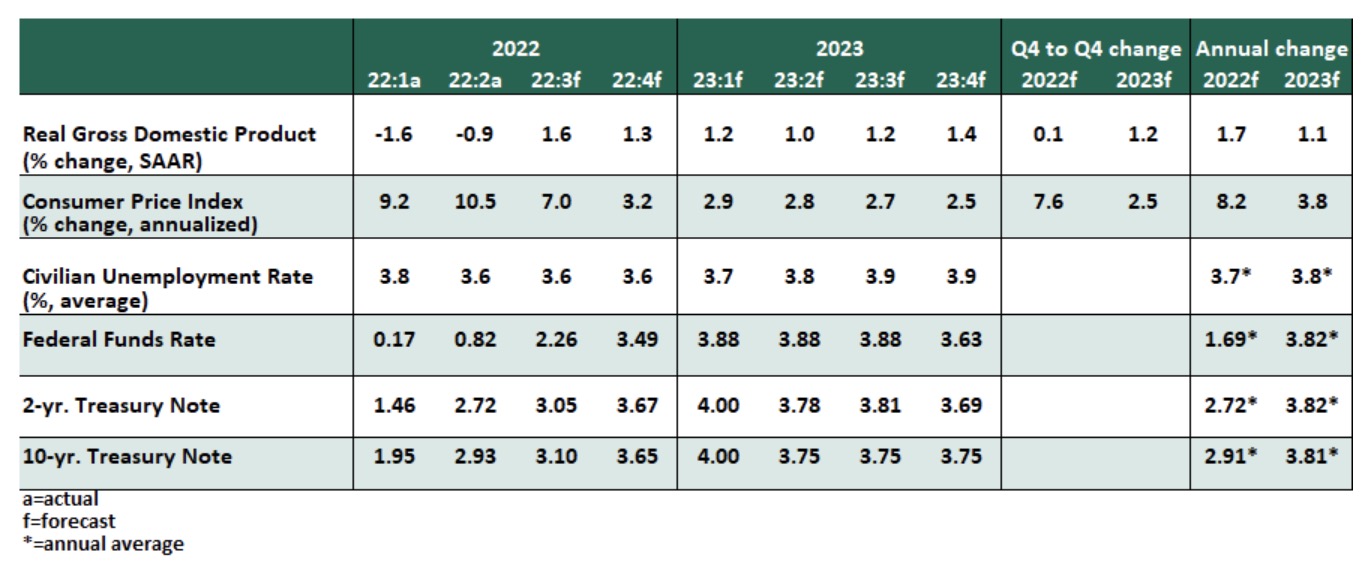

The latest data shows inflation is still with us at an 8.5% annual rate. That means we can expect the Fed to keep tightening, trying to reduce demand and relieve pressure on consumer prices.

Let’s talk about something few people have any interest in talking about this year.

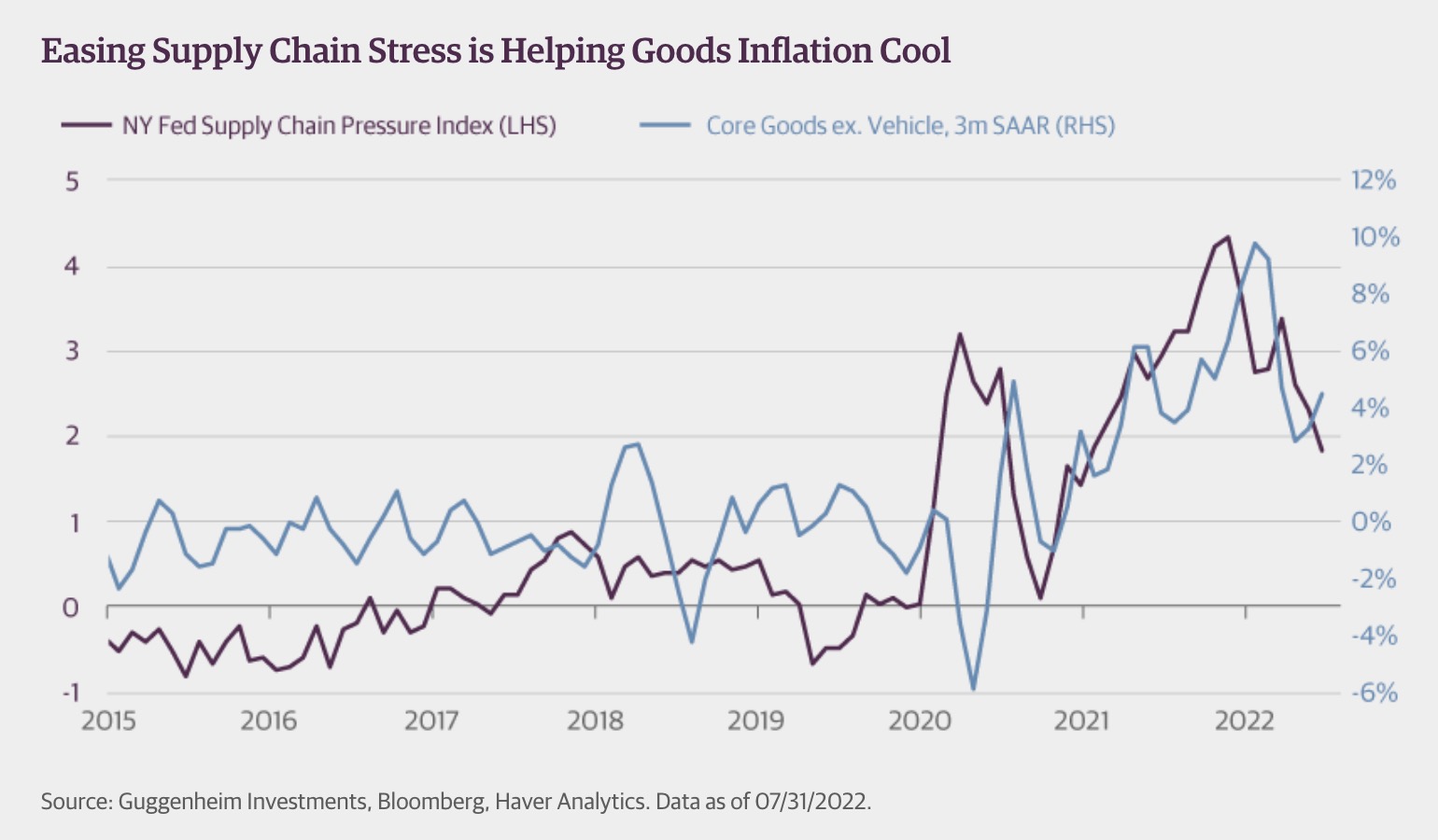

Lower July CPI inflation is likely the beginning of a trend.

PIMCO’s Global Advisory Board discusses the longer-term outlook for geopolitics, inflation, and other macro themes.

Take-Two Interactive Software makes games for consoles, computers, and phones

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates.

Jim Cramer recently stated it will be time to buy stocks when the Fed pivots.

U.S. stocks are moving upward, continuing yesterday's rally, as the markets digest the release of the Producer Price Index.

Despite price declines in many sectors, the Federal Reserve may continue its hawkish approach.

The outcome of next year's world championship chess match will likely hinge as much on technological superiority as on individual human ingenuity.

Twenty years ago, people on trading floors at investment banks worked in silos.