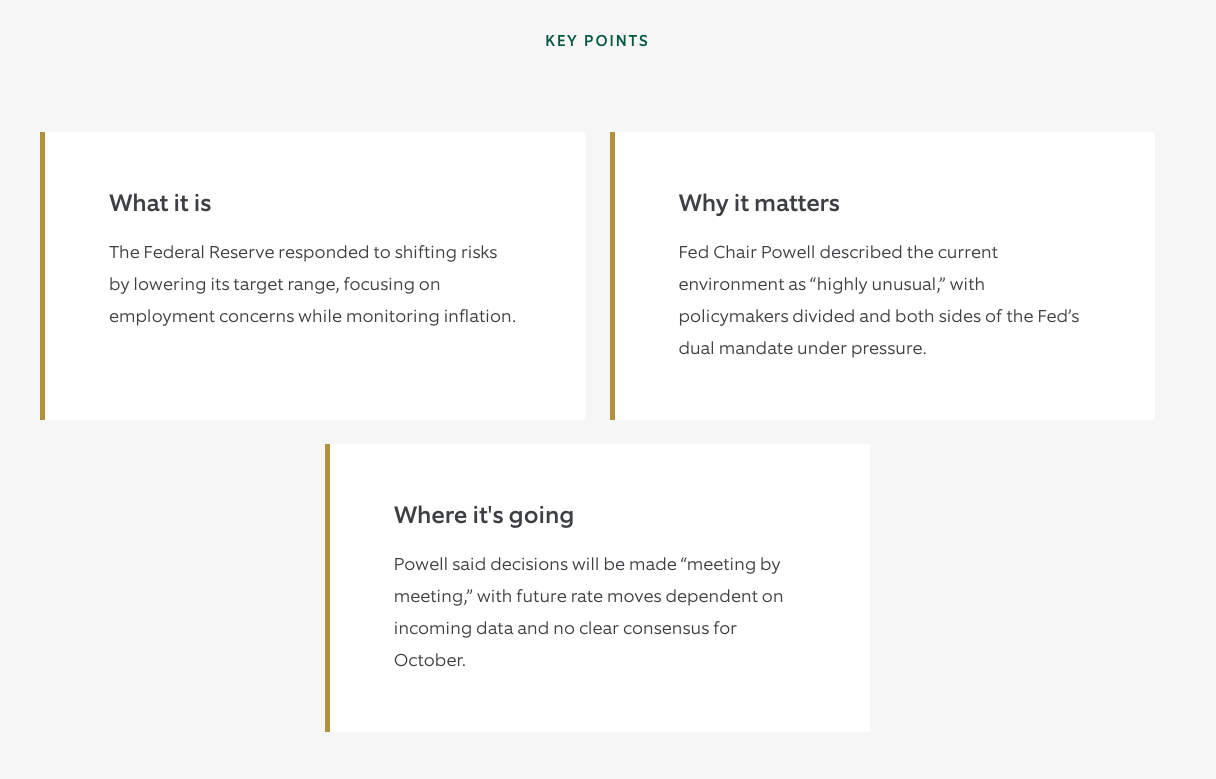

Chair Jay Powell described the Fed’s decision to lower its target range for the federal funds rate as “a risk-management cut.” In other words, the move was meant to address growing risks to the job market, even though inflation risks remained tilted to the upside. Powell acknowledged there is a wide range of views among Fed policymakers about whether to cut rates further this year. But he stated that such diversity of views is “very unsurprising,” given what he called the “highly unusual” circumstances the Federal Open Market Committee—or FOMC—now faces. We read his remarks as suggesting that a rate cut in October, while a reasonable base case, may not be as likely as currently implied by market pricing. Let’s take a closer look.

When addressing the main rationale for the rate cut, the FOMC’s policy statement characterized it as a “shift in the balance of risks” around its two goals: price stability and maximum employment. During the press conference, Powell repeated the statement’s language that downside risks to employment had increased, but he added that “the risks of higher and more persistent inflation have probably become a little less.” Still, he made it clear the risks are “not quite at equality,” suggesting that upside risks to inflation remained somewhat greater than downside risks to employment.

Powell pointed out several times that the FOMC is facing “quite an unusual situation,” because its two policy goals are currently “in tension.” Referring to the so-called “dot plot,” which summarizes policymakers’ views of where rates should go, he noted that it should not be surprising those views are currently so dispersed. In fact, we noticed that, if it weren’t for newly appointed Governor Stephen Miran, the group would have been evenly split between those who favored two additional 25-basis-point cuts this year, and those who favored, at most, only one more.

Commenting on the outlook for policy, Powell emphasized that the Committee is “in a meeting-by-meeting situation.” We take that to mean a higher-than-usual sensitivity to incoming data as they weigh the risks around their two goals. Given the potential for data surprises between now and the October meeting however, the chances of another rate cut in October may not be as high as current market pricing implies, particularly for a Committee that seems nearly evenly divided on what to do at its two remaining meetings this year.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee

© Northern Trust

Read more commentaries by Northern Trust