Over 50 years ago, U.S. Treasury Secretary John Connally summarized the dollar succinctly to his European counterparts: “The dollar is our currency but your problem.” Today, the U.S. administration seems to think that the dollar is America’s problem, and is considering steps to solve it.

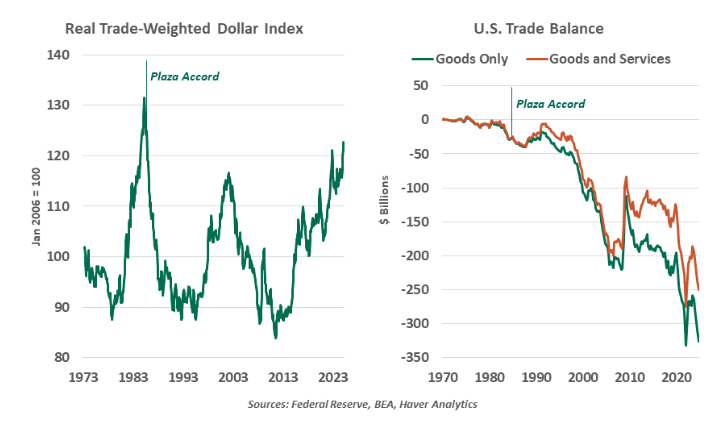

The last time the dollar needed policy intervention was in 1985. The dollar was ascendant, and that put American exports at a disadvantage. The White House arranged an international response, with five nations agreeing on the “Plaza Accord” to realign global exchange rates. The effort succeeded in devaluing the dollar, but it did little to bring better balance to the U.S. trade position.

In recent years, the dollar has once again been persistently strong. Its standing stems (in part) from its role as the world’s reserve currency. As we discuss in our interview with Northern Trust’s chief foreign exchange dealer (linked below), we do not expect that to change. The dollar remains a highly liquid currency which is used most frequently to settle international transactions. The U.S. dollar also represents the majority of central banks’ foreign reserves

Having the reserve currency can create complications. Offshore demand for the dollar subjects the U.S. to the Triffin Dilemma: The reserve currency must keep its supply of money in check to maintain stability, while also meeting increased global demand. The nation that offers a global reserve currency will inevitably run a trade deficit, as exports of currency are offset with imports of goods.

The U.S. has also borne the cost of its wide defense umbrella, helping to ensure a peaceful world order that supports global trade and growth. The nation’s military budget of $842 billion is multiples higher than any other country. Its dominant military and currency have given the U.S. its position of “exorbitant privilege,” running fiscal and trade deficits without adversely affecting its borrowing costs or currency stability.

Could the U.S. bring about global currency coordination today?

Viewed across centuries of history, the United States’ run as the leading global power has generally been a time of peace, prosperity and advancement for the world. Viewed transactionally, though, U.S. hegemony has been costly. The strong dollar eroded the competitiveness of U.S. manufactured goods. Americans without higher-skill training have been left behind. The nation’s debt is rising and getting more expensive to service amid higher interest rates, forcing contentious discussions of government spending cuts.

Enter what has been called the “Mar-a-Lago Accord.” To be clear, an Accord is not a stated policy goal of the Trump administration. However, it offers hints of how the Trump agenda could be achieved.

The outlines of the Accord—and the first appearance of its name—took shape in a position paper titled “A User’s Guide to Restructuring the Global Trading System.” The author, Stephen Miran, was an investment strategist when he published the paper in November 2024; he now chairs the president’s Council of Economic Advisers. After describing the Triffin dilemma and its outcomes, Miran offers a strategy to balance the conflicting objectives of weakening the dollar while maintaining its reserve status.

The Plaza Accord set a precedent for governments to devalue their currencies cooperatively; the dollar’s appreciation was distorting global economies. The Mar-a-Lago Accord aspires to another adjustment. The U.S. dollar could be weakened through U.S. acquisition of foreign currencies. These interventions would likely lead to higher U.S. interest rates as Treasuries are sold off. To avoid higher yields, foreign nations would be encouraged to swap their current U.S. Treasuries into very long-dated, low-yield bonds. The U.S. would thus avoid the risk of higher debt service costs from higher rates.

This is not an attractive proposition for counterparties to the United States, who would not welcome lower interest receipts or stronger currencies. To overcome this resistance, Miran’s paper proposed to use tariffs and security as leverage. Nations who cooperate will receive lower duties and the support of the world’s largest military. Those who resist will struggle to sell into the U.S. market and may lose an important ally.

Major changes bring major risks.

We are skeptical of the Mar-a-Lago Accord. The dollar is strong based on its fundamentals, and not overvalued in a meaningful way. China runs the largest surplus with the U.S. and is the nation’s second largest foreign holder of Treasuries (behind Japan). China would be least amenable to a higher exchange rate as it pushes to maintain its export sector; it would also not be compelled by an offer of mutual defense. Moves by nations to enhance their militaries, notably in Germany, illustrate a rising suspicion of the durability of U.S. alliances.

The strong dollar has been a modest impairment to the export prospects of U.S. manufactured goods, but weakening it would not immediately alter the global trade landscape. The U.S. will still have higher labor costs, more environmental restrictions and older infrastructure that will limit its competitiveness. And a lower-value currency will raise the costs of imports required for raw materials and many consumer goods, raising the risk of inflation.

The Plaza Accord did not arrest the decline of U.S. manufacturing jobs, and it is not clear that the current proposal would be much more successful. And if the Mar-a-Lago Accord’s demands erode the dollar’s position as global reserve currency, the U.S. could pay dearly over time.

The year to date has been marked by a high degree of policy uncertainty and volatility. To its authors, the Mar-a-Lago Accord places these actions into a more cohesive policy agenda. But obstacles to its implementation are legion, and it could easily create more harm than good for the United States. Today, the dollar’s value is neither a problem nor a solution to global trade issues.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust