Taxes are a constant thread in the history of the United States. Early settlers sought independence from Great Britain due to the monarchy’s taxation of its colonies, with the Boston Tea Party protest of 1773 serving as a prelude to the Revolutionary War. Following this experience, the Constitution limited the federal government’s ability to tax its residents. The modern income tax system only became possible after the ratification of the Sixteenth Amendment in 1913. From that point, Federal taxation incrementally grew in its scope and complexity, with only occasional efforts to simplify.

In the early 1980s, the U.S. Congress began lowering tax rates. The Tax Cuts and Jobs Act of 2017 (TCJA) is the most recent expression of that trend. Today, Congress is deliberating how to extend, update and even expand the TCJA before its year-end expiration. While our leaders debate its future course, we will take this opportunity to refresh our memory of what TCJA accomplished…and what it did not.

The Act generally lowered American tax rates, though different income groups received different levels of relief. The lowest-earning 40% of households do not owe federal income tax, so they were relatively unaffected. The marginal rate of the top tax bracket was lowered from 39.6% to 37%; only the top percentile of earners reach this tier (individual income over $626,350 in 2025).

In the middle of the income spectrum, TCJA reduced the rates on most individual tax brackets while simplifying deductions and exemptions. Larger standard deductions and child tax credits yielded a net tax reduction for most households, while creating a simpler filing process. The threshold for alternative minimum taxes on higher earners was raised, as was the tax-free exemption for inheritances. Some of the revenue loss associated with the TCJA was offset by a cap on the deductions allowed for state and local taxes, a provision that still stings taxpayers in higher-cost locations.

Several important elements of the TCJA did not affect households. First, the corporate tax rate was lowered from 35% to 21% -- the only provision of TCJA that is not set to expire this year. At the time, the U.S. stood out as having an especially high corporate tax rate among developed nations, creating incentives for multinational firms to expand and keep their profits abroad.

TCJA prompted a welcome increase in corporate investment, but the Act did not pay for itself.

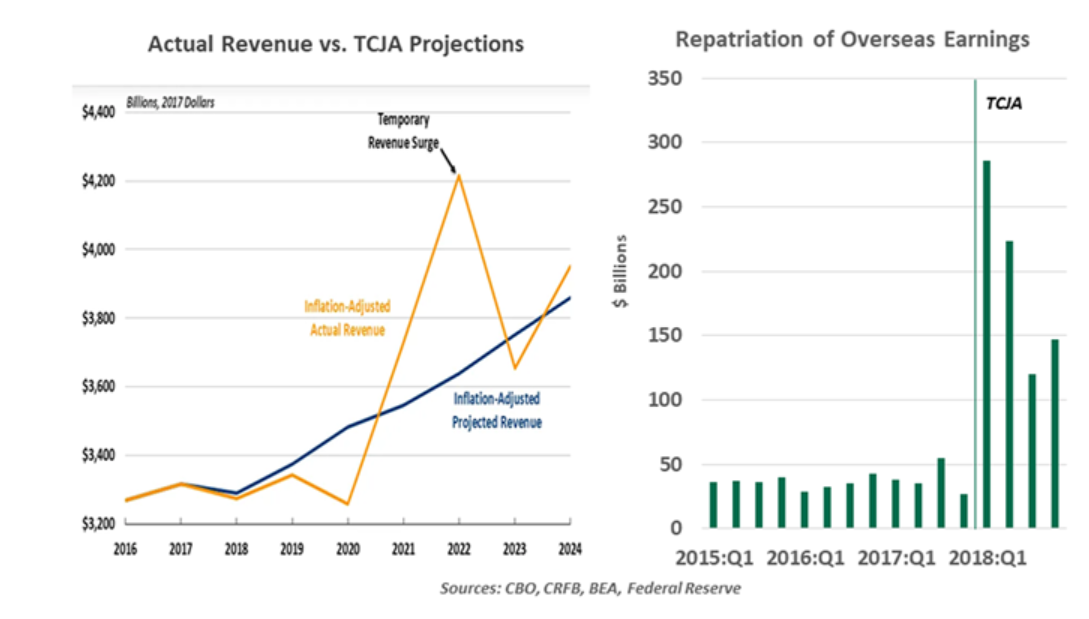

The Act also reformed the treatment of corporate income earned outside of the U.S. International tax policy is tricky; it attempts to balance raising revenue with avoiding profit shifting. Prior to TCJA, U.S. multinationals owed U.S. taxes on income earned abroad in addition to taxes paid in those locales. However, domestic levies were only due when the profits were repatriated, a process which was often deferred indefinitely. TCJA brought the U.S. into better alignment with global standards, prompting a flood of profit repatriation.

Federal Reserve research found that firms repatriated roughly 78% of accrued offshore earnings in the year following TCJA’s passing. However, the same study found that much of that cash flow was directed toward share buybacks. Though beneficial to shareholders, the repatriation did little to support new investment. TCJA has since kept a territorial tax regime in place that has reduced the incentive to shift profits.

The TCJA allowed corporations to immediately deduct the expenses of capital investment in assets with cost recovery periods of less than 20 years, like machinery and equipment. The previous requirement to depreciate those assets over their full life span created a disincentive to invest. And for closely-held businesses, TCJA established a 20 percent cut to pass-through income, intended to bring small business taxation in better alignment with larger corporations. Research found that bonus depreciation helped to lift the nation’s capital stock by 2%.

These business-friendly features required offsets to keep TCJA closer to the projected revenue neutrality required by the reconciliation process (which will also bind this year’s budget negotiations). The Act stipulated that bonus depreciation would be stepped down incrementally starting in 2023. And from 2022, costs of research and development (R&D) were required to be amortized rather than immediately expensed, creating a disincentive to invest in research.

Supply-side economists defend tax cuts by saying they pay for themselves. By freeing up funds that would otherwise be spent on taxes, households can spend more freely, while businesses can invest in projects, give raises and pay dividends.

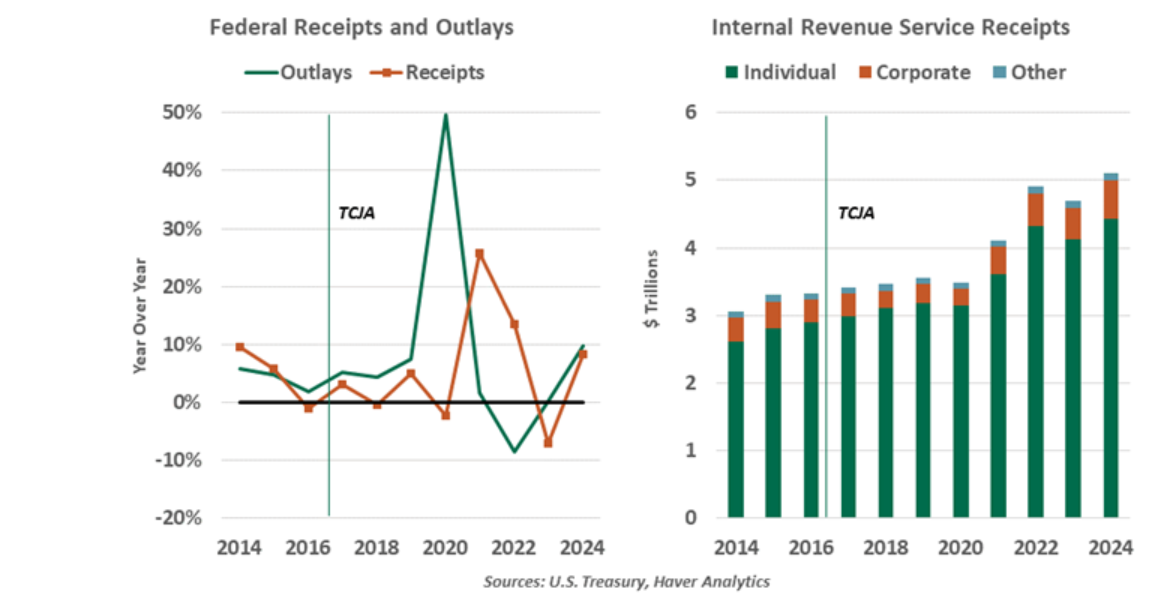

With the TCJA, it is difficult to test this thesis. During the first two years after its passage, Federal revenues fell short of what had been projected by the Congressional Budget Office (CBO). And then, the pandemic hit. Massive government stimulus was applied, generating a quick resurgence of economic activity and market performance. Federal revenue spiked in fiscal year 2022, with outsized economic growth and the 2021 market rally fueling high income and capital gains receipts. While very much welcome, this outcome cannot be attributed to the TCJA.

In a steadier counterfactual, TCJA would almost certainly have added importantly to the nation’s fiscal imbalance. Forecasts surrounding the upcoming reconciliation package therefore should not assume another windfall of tax collections if TCJA provisions are extended. The current CBO forecast shows the deficit growing by $800 billion (42%) by 2035, and that is with higher rates from the sunset of TCJA. Reducing tax rates will widen the deficit.

Preserving incentives for investment and hiring should be prioritized.

If we could prescribe a set of reforms to prioritize, we would favor those that most directly support business investment and hiring. The nation is reevaluating its trade strategy, with an eye toward restoring the competitiveness of American production. Immediate expensing of capital and R&D investment will provide critical support to this effort. The international tax treatment reforms reduced profit-shifting and brought the U.S. into better international alignment; reverting would be an impairment to competitiveness.

TCJA took shape after the modern-day Tea Party fought for smaller budget deficits. Assuring that the next reconciliation bill is budget-neutral will be critical to keeping debt sustainable and investors comfortable. The negotiations that will take place on this front in the coming weeks could be historic, indeed.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© Northern Trust

Read more commentaries by Northern Trust