The Trump administration has announced new tariffs for three weekends in a row. The first round, against Colombia, was quickly reversed. The next, targeting Canada, Mexico and China, was limited only to China, with North American nations getting a reprieve. The latest move, involving metals, is likely to be permanent.

During his first administration, President Trump’s trade team initiated an investigation and justified tariffs under Section 232 of the Trade Expansion Act; the Act affords the president the right to impose tariffs to protect national security. The Biden administration temporarily loosened policy in 2022, with a quota system allowing many metal imports to arrive duty-free. In exchange, the European Union revoked its retaliatory levies on U.S. products like motorcycles and whiskey. Notably, tariffs on Chinese steel were never rescinded.

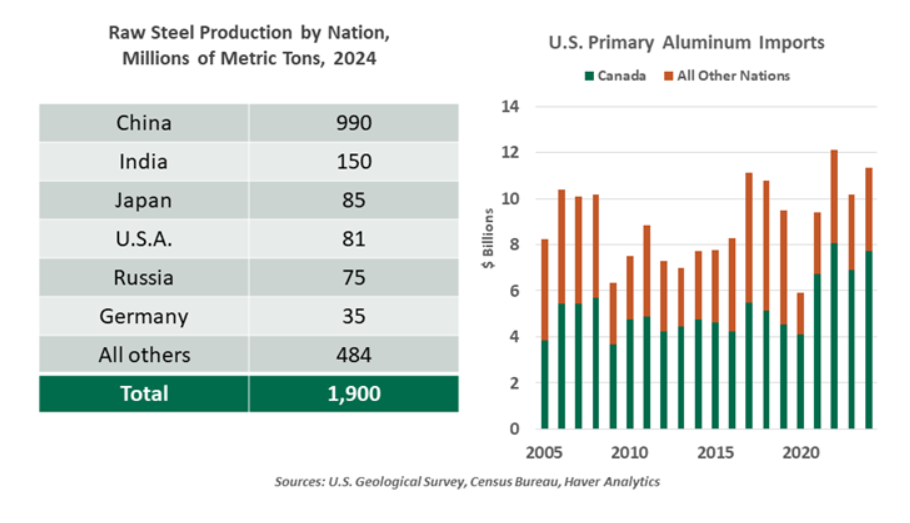

Biden’s détente was set to expire in March 2025, requiring renewed negotiations. The conclusions of the 2018 trade investigation remain valid, and the national security rationale is justifiable. U.S. primary production of steel peaked in 1973, and its production of aluminum peaked in 1980. Today, roughly a quarter of the steel and half of aluminum used in the U.S. are imported.

This represents a security risk. In times of conflict, sources abroad may no longer be reliable. Sudden national defense demand would quickly overwhelm the nation’s capacity. And while not the primary rationale of the action, many nations do subsidize their metal manufacturing sector, putting U.S. exports at a disadvantage.

Tariffs on metals are unlikely to bend.

These industry-specific tariffs are meant to bring about a change in trade patterns, rebuilding productive capacity in the U.S. while limiting China’s competitive prospects. Transitions of such a scale will not come quickly. A complete restoration of the heyday of U.S. metallurgy is unlikely, with the nation accounting for less than 5% of global capacity.

Expanding production won’t be easy. American steel plants are utilizing about 80% of their capacity, and many shuttered plants are too antiquated to be brought back online. In an industry long in decline and consolidation, appetite for new capital investment in steel foundries is limited and will run afoul of environmental regulations. Even if pollution standards were lifted, the availability and cost of energy will constrain domestic expansion. The disruption from new tariffs will be swift; the upside from supporting domestic industry will be gradual.

Production of new (primary) aluminum is energy-intensive, with an especially large requirement for electricity. Factories (smelters) are typically located near abundant sources of energy, like large rivers. Primary aluminum is made from bauxite, a mineral of which the U.S. has limited reserves and few active mines. Domestically-produced bauxite is typically used for other chemical production processes. Amid these constraints, about 80% of current U.S. aluminum production is secondary, recycling scraps from primary production and post-consumer waste.