The Northern Trust Economics team shares its outlook for key markets in the month ahead.

As we enter the third year of the pandemic, recent economic developments have been both encouraging and troubling. The good news is that economic recovery has continued, even as policymakers continue their efforts to balance economic and public health. On the other hand, the challenges presented by Omicron have impaired both supply and demand as 2022 begins.

Fortunately, case counts in many Western countries are in decline, promising another round of reopening as spring approaches. This expectation has allowed policymakers to focus on elevated inflation and tightening labor markets. Multiple rate hikes are in store in the U.S. and the U.K.

2021 brought challenges that not many would have foreseen, from new virus variants to lasting supply chain disruptions. With headwinds fading and tailwinds present, the outlook for this year remains very good.

Following are perspectives on how major economies are poised to perform.

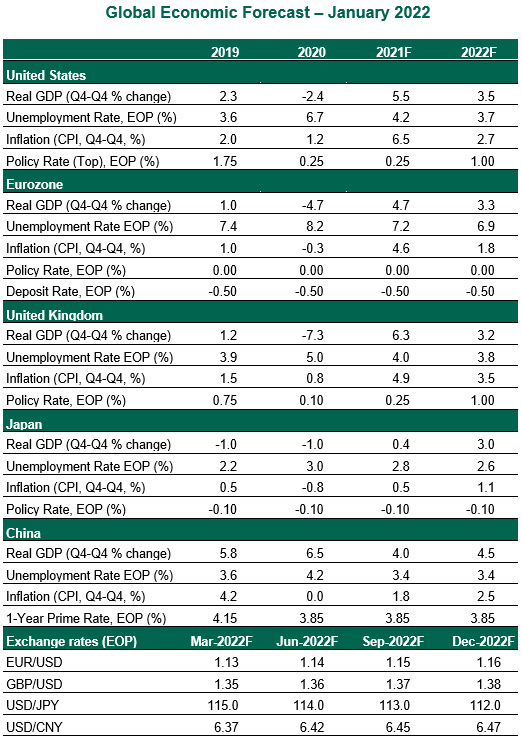

Japan

- The Japanese economy likely posted a robust recovery in the fourth quarter of 2021. But the country has seen a sharp rise in Omicron cases recently, leading to tighter restrictions. This will weigh on domestic consumption in the first quarter. The release of pent-up demand and the ongoing recovery in exports should lead to a rebound in growth in the balance of the year.

- Uniquely, Japan has been less impacted by consumer inflation, despite producer prices surging to a four-decade high. Lack of pricing power is a key factor behind firms not being able to pass on higher costs to consumers. As a result, the Bank of Japan (BoJ) maintained the status quo across all policy parameters at this month’s meeting. However, a weaker yen and higher commodity prices did lead to an upward revision of the BoJ’s inflation forecasts.

China

- Growth continued to decelerate in China from double digits in the first half of 2021 to 4.9% year-over-year in the third quarter and 4.0% in the last quarter of 2021. The Chinese economy had benefitted from strong demand for goods during the earlier waves of the pandemic. However, its zero-COVID policy is now putting the economy at a disadvantage relative to other markets. Sluggish consumption amid virus-related uncertainty, supply bottlenecks, and the property downturn have weighed on the Chinese economy. These factors will continue to resonate in 2022, but the risks around Evergrande and other developers will likely be ring-fenced.

- The slowdown has caused a shift in policy tone and stance with emphasis being given to stabilizing growth. The People’s Bank of China, earlier this month, cut policy rates by 10bps and pledged to “open its monetary policy toolbox wider”, implying more easing is on the way. Fiscal measures in the form of infrastructure spending and tax cuts are also likely.

© Northern Trust

Read more commentaries by Northern Trust