How an election affects stock market performance depends more on how close and contentious it is than on whether the winner is Republican or Democrat, liberal or conservative.

No one enjoys getting dumped. This holds true in finance and investing as much as it does in romantic relationships. When companies are dumped from the major indexes, their managers and shareholders may feel jilted and their stock may flounder post-breakup.

Following Russia's invasion of Ukraine in the early months of 2022, and the subsequent sanctions imposed by the U.S., some investors were forced to liquidate their Russian investments. Many investors, uncertain about the potential scope of the coming war, also took the opportunity to liquidate their investments in all of Eastern Europe.

First-generation low carbon equity benchmark indices were developed almost a decade ago with the goals of mitigating climate risk and preparing for the transition to a low carbon economy.

While governments responsibly issue debt to fund public investment and dampen the business cycle, the US federal government has borrowed at an increasingly prolificate pace over recent decades.

These are only some of the exciting new applications on everyone’s lips at business gatherings these days, where the conversation often veers to artificial intelligence, which has become the latest “new new thing.”

Over recent decades, the hot tech trends (from search to cellphones to social media to the digital economy and now to AI) have been a predominantly American story.

Nobel laureate Harry Markowitz famously asserted that diversification is the only free lunch in investing. His insight was simple yet profound: by diversifying across assets, investors can achieve higher returns without necessarily increasing risk.

After a decade in the wilderness, value investing roared back to life in 2022, led by long-forsaken sectors such as energy, industrials and even certain retailers. Many portfolios had either intentionally or unintentionally migrated heavily towards “growth at any price” exposures and were caught wrong-footed that year.

It is certainly a confusing economic environment. Jobs growth is strong yet there are constant reports of high-profile company layoffs. The yield curve is inverted suggesting a recession yet the stock market is at a record high.

As the calendar closed on 2023, investors were once again treated to magnificent returns in their stock and bond portfolio.

Following a period of relatively calm asset markets from 2013-2019, in which the CBOE Volatility Index (VIX) averaged just below 15, volatility in asset markets has returned1 and investors have been looking for ways to protect themselves.

“The current fiscal path is unsustainable”. This stark warning comes from the US Treasury Department’s Bureau of the Fiscal Service’s fiscal year-end projections1. Based on current appropriations and tax law, these projections display steadily rising federal spending and flat tax receipts, as a percentage of GDP.

Trench warfare in the early 20th century has been described as long periods of boredom punctuated by moments of terror.

Higher interest rates and inflation are likely to usher in a decade of policy restraint, limited liquidity and macro volatility, pressuring equities and motivating investors to reconsider tactical asset allocation and embrace real assets.

As with most new expressions, “smart beta” is in the process of seeking an established meaning. It is fast becoming one of the most overused, ill-defined, and controversial terms in the modern financial lexicon.

In smart beta, we find that factor returns—net of changes in valuation levels—are much lower than recent performance suggests. In fact, many of the most popular new factors (some 458 at last count) have succeeded solely because they have become more expensive.

With artificial intelligence, systematic investing is entering a new era of disciplined decision-making. Yet, firms face many snags. Rigorous implementation requires collaboration among skillful investment, technology, and quantitative capabilities.

With negligible incremental risk, a RAFI Global Index hypothetically outperformed a Cap-Weighted Global Index by 40 bps per annum and a Cap-Weighted Global Value Index by 2.2% from 2007 to 2022—a 16-year period covering the long value rout and its aftermath.

Research Affiliates explain why their long-term return forecasts have risen across asset classes and the implications of their near-term outlook for U.S. recession.

While inflation dipping below 3% has been welcome news for investors, it’s still early to claim that inflation has been reined in. Our simple analysis shows that inflation rising in the latter half of 2023 would not be surprising.

The Fed’s refusal to pause rates through the first five months of 2023 raises the odds of a hard landing. The magnitude of the yield-curve inversion has increased the risk inherent in the US banking and financial systems. The impending recession is unnecessary and self-inflicted.

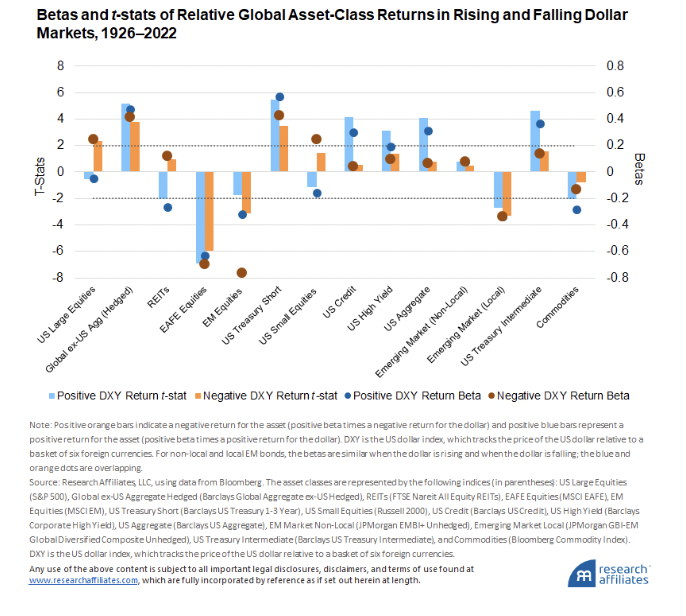

US dollar cycles are long.

Nearly seven years have passed since the publication of our 2016 paper “How Can ‘Smart Beta’ Go Horribly Wrong?”

A common error of earnings aggregation from stocks to the market persists.

Tesla’s shares fell by more than 14% on Tuesday, after plunging by 65% in 2022.

The US Federal Reserve Bank’s expectations for the speed of reverting to 2% inflation levels remains dangerously optimistic.

In the 1980s there was a famous TV ad for Wendy’s with the tagline “Where’s the beef?”.

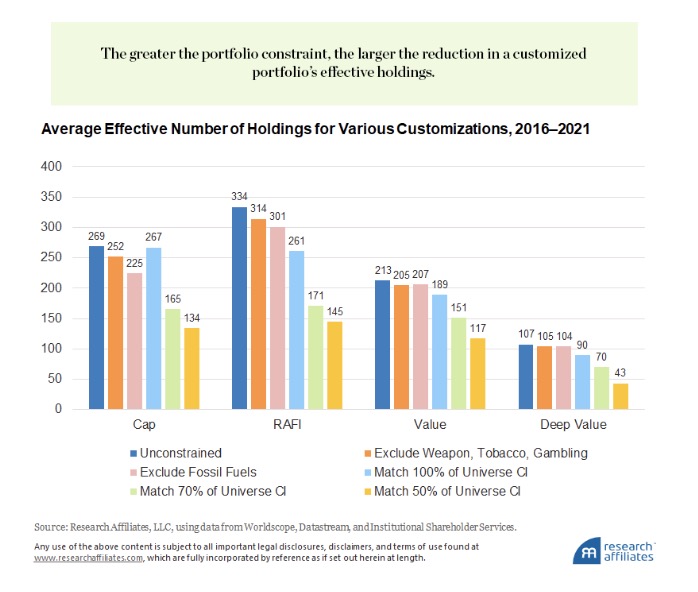

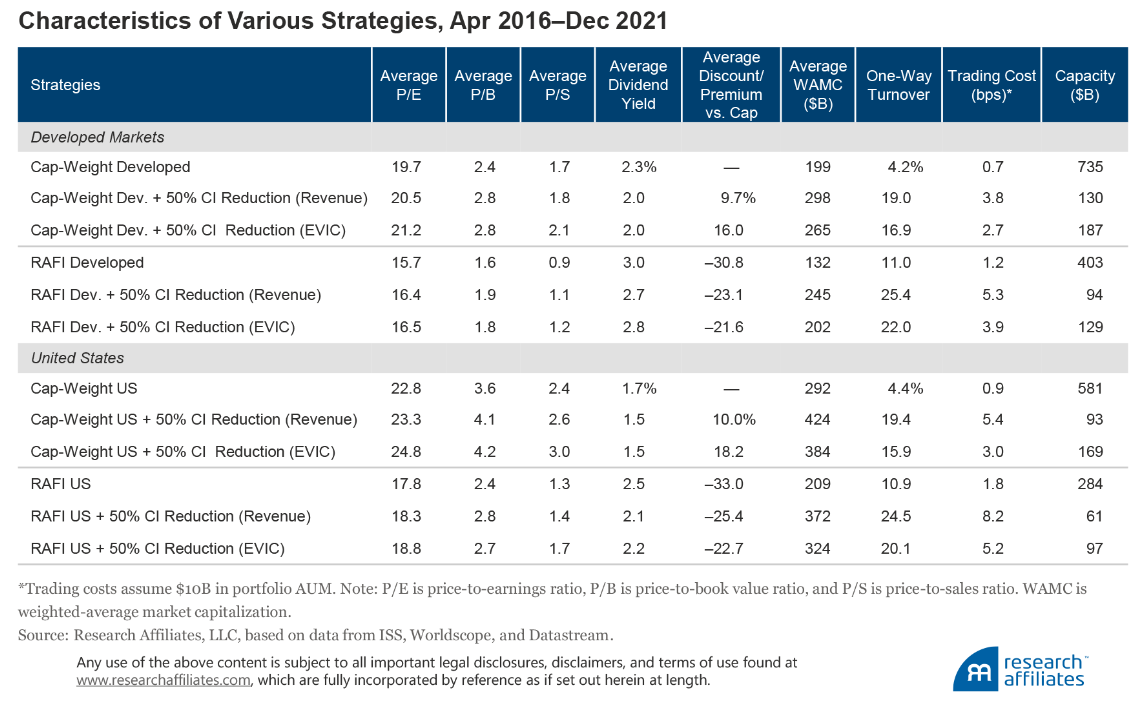

We apply five levels of customization to four developed-market equity strategies to quantify the impact of customization (or direct indexing).

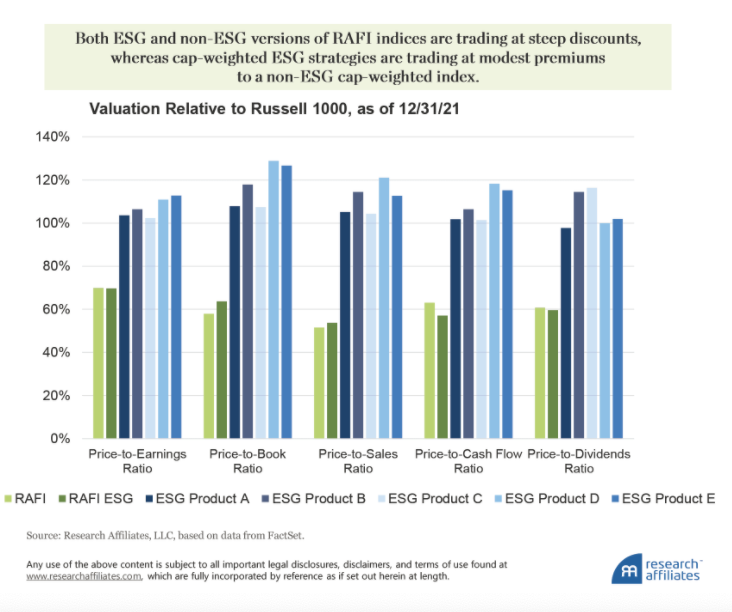

Investors can choose one of two popular scaling methods for carbon emissions comparisons across companies. Our analysis guides investors in making this important decision.

Now is the time to engage in risk management to retain your competitive advantage once the economy emerges from the slowdown.

Trillions of dollars of deficit spending financed by money creation over the past two years caused today’s soaring inflation.

Traditional long-only fixed income managers had one of the worst quarters on record in Q1 2022 as higher interest rates left “bottom up” portfolios overweight duration.

A portfolio’s return is driven by its investment strategy—a set of decisions that governs allocation and timing of capital among the portfolio’s positions.

Inflation is rising rapidly, not an unexpected outcome given governments’ pandemic policy response of ballooning deficits and soaring government debt.

The value rebound that started in September 2020 gave up nearly half its gains by mid-May 2021 as the recovery faltered with the onslaught of the highly contagious Delta variant. But vaccination has proven highly effective, and as the unvaccinated around the world become vaccinated, the prospect of a reinvigorated economy is good. Is now a second chance to rebalance into value stocks?

Rather than predicting what will happen to inflation in the future—a particularly arduous and humbling task—we ask a simple question: What can past inflation dynamics tell us about the equity market’s future returns?

We have observed that additions and deletions to the S&P 500 Index follow a dependable pattern: additions underperform and deletions overperform over the subsequent 12-month period.

The performance of a market-cap-weighted index is driven by a handful of stocks with the largest capitalizations, but these stocks do not remain at the top for long. A smart beta multi-factor strategy is a good solution for investors concerned about the concentration risk of a passive market-cap tracker.

Climate research informs us that in 2017 anthropogenic global warming reached1.0° C above pre-industrial levels (IPCC, 2018).

Factor timing is the ability to add value to an investment strategy by altering the exposure to various factors through time.

The “big market delusion” is when all firms in an evolving industry rise together, although as competitors ultimately some will win and some will lose.

We compare the current value of bonds versus stocks within the context of the equity risk premium. We couple this analysis with an evaluation of possible Fed policy direction. Our conclusion is that risk assets, such as US equities and corporate bonds, are poised to benefit as are gold and other commodities due to tumbling real yields and dollar weakening.

In late 2020, a new kid emerged on the bargain-of-the-decade block. UK stocks, and notably UK value, reached very cheap levels relative to value stocks in other developed economies. Today, UK value remains at remarkably low valuations relative to most of its fundamentals.

Rob Arnott: “There hasn’t been a better time to be a value investor at any other time in my career. I look back at the tech bubble and I never thought I would see valuations stretched the way they were then. We're back to that, and then some." We invite you to revisit “Reports of Value’s Death Have Been Greatly Exaggerated” now published in the Financial Analysts Journal.

By buying or overweighting characteristics-based factor exposure and selling or underweighting beta-based factor exposure, investors can position their portfolios to reap the rewards of factor investing while bearing less risk.

Massive growth in central bank balance sheets via quantitative easing, debt monetization, and firing of “big bazooka” stimulus packages brings renewed focus to potential shocks in the business cycle. An awareness of the macroeconomic “shocks” and their impact on asset prices should be incorporated in investors’ tactical asset-allocation decisions.

Over the last dozen years, investors holding the classic US 60/40 portfolio were substantially better off than their diversified peers, yet now is not the time to abandon diversification and diversifying asset classes. We believe it is imprudent to trust that escalation in valuations will continue unabated into the next decade...

The sage advice to “know what you are investing in” is being dangerously overlooked by both novice and seasoned investors when it comes to bitcoin. A former bitcoin miner explains why the price of BTC is nearly certainly a bubble and likely manipulated. Investors should proceed with extreme caution.

On December 21, Tesla will be the largest company ever to enter the S&P 500 Index. Tesla’s skyhigh valuation, which meets our real-time definition of a bubble, conforms to the observation that market-cap-weighted indices buy high and sell low—the antithesis of prudent investing.