To clear our notebooks entering 2025, here are quick perspectives on a range of topics.

We prefer equities over fixed income, in particular U.S. equities as the outlook for the U.S. economy is solid and promising.

We look back on six themes that defined another eventful year.

We believe that there are several guardrails in place that considerably limit the extent of presidential influence over monetary policy decisions.

As the year comes to a busy conclusion, we’re still catching up with news that didn’t make the front page. In the first week of November, the U.S. Bureau of Labor Statistics published a data release that’s even less frequent than the four year presidential election cycle.

Last weekend, the Cathedral of Notre Dame reopened after being severely damaged in a fire five years ago. It took thousands of craftsmen and a reported €840 million to restore the iconic structure.

International commerce often follows the simple rule: one nation’s loss can result in another’s gain. China’s loss from escalating trade tensions with the U.S. is generating gains for several Asian economies, but India is not one of them.

How a diversified liquidity strategy might help time-strapped corporate treasurers reduce vulnerabilities and improve adaptability in uncertain markets while maintaining access to cash.

We expect high yield bond issuers to maintain healthy balance sheets and defaults to remain low.

We examine how a potentially complex bond market in 2025 could still offer opportunities in high-yield bonds, municipal bonds, and inflation-protected securities.

We are prone to animal analogies when describing disorderly situations: like herding cats, like a barrel full of monkeys, like a dog’s breakfast.

Not everyone is ready to give thanks for moderating food prices.

New ideas are never as easy as they sound in campaigns.

Sticky underlying price pressures could prevent a faster return to neutral monetary policy.

Lost in the excitement of election week was a meeting of the Federal Reserve. At its conclusion, interest rates were lowered by another quarter-point. But where they are heading from here is a matter of increasing uncertainty.

In sport, play is limited by time or innings. Lineups are set, rules are fixed and boundaries are defined. Winners are determined objectively.

The Northern Trust Economics team shares its outlook for U.S. growth, employment, inflation and interest rates.

The people have spoken. While there are still some unknowns, the contours of the American government that will be seated next January are reasonably clear.

Western economies are inching towards soft landings, and their central banks are reducing interest rates. These developments will be helpful to economies in the Asia-Pacific region as they conclude 2024 and look forward to next year. However, the outlook for China remains a central concern.

The election is unlikely to influence monetary policy.

Enthusiasm for structural reforms is only going to wane.

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates in major markets.

Our analysis explores how potential post-election tax policy changes might impact dividends, capital gains, and municipal bonds and how investors might prepare for different election outcomes.

Equities continued to climb in Q3, with fixed income remaining steady despite international conflicts, inflationary pressure, and election-related uncertainty in the United States.

State and municipal budgets are adjusting to life after pandemic interventions.

An independent central bank supports better economic and market outcomes.

With the election looming, investors should prepare for potential changes in tax policies, particularly given the impending sunset of the 2017 Tax Cuts and Jobs Act.

The regulatory outlook is a question of direction more than extent.

Global oil markets are working through many disruptions.

Energy policy decisions today will have long-lasting implications.

Asia-Pacific economies will benefit from soft landings and easier monetary conditions.

New business formations have held up, but closures are also rising.

The election could alter the thriving relations between the U.S. and Europe.

The need for old age support is on the rise, as is its cost.

The latest S&P 500 rebalance introduced Dell and Palantir to the index, and Apple’s weight grew with annual float changes, signaling technology’s ongoing influence.

Our research shows that on average U.S. stocks performed well a year after the start of a Federal Reserve rate cut cycle.

Tougher stances on trade are a point of bipartisan agreement.

Sports fans know that a lot can change in the fourth quarter of a game. So too for the U.S. economy, as a substantial labor action commenced the minute that calendars turned to the fourth quarter of 2024.

Policymakers have recognized China's slower economy.

Our experts explore the implications of wider S&P 500 earnings growth, potential Fed rate cuts, and the outlook for global equities and bonds amidst ongoing economic shifts.

Tax cuts are popular but not affordable for most nations.

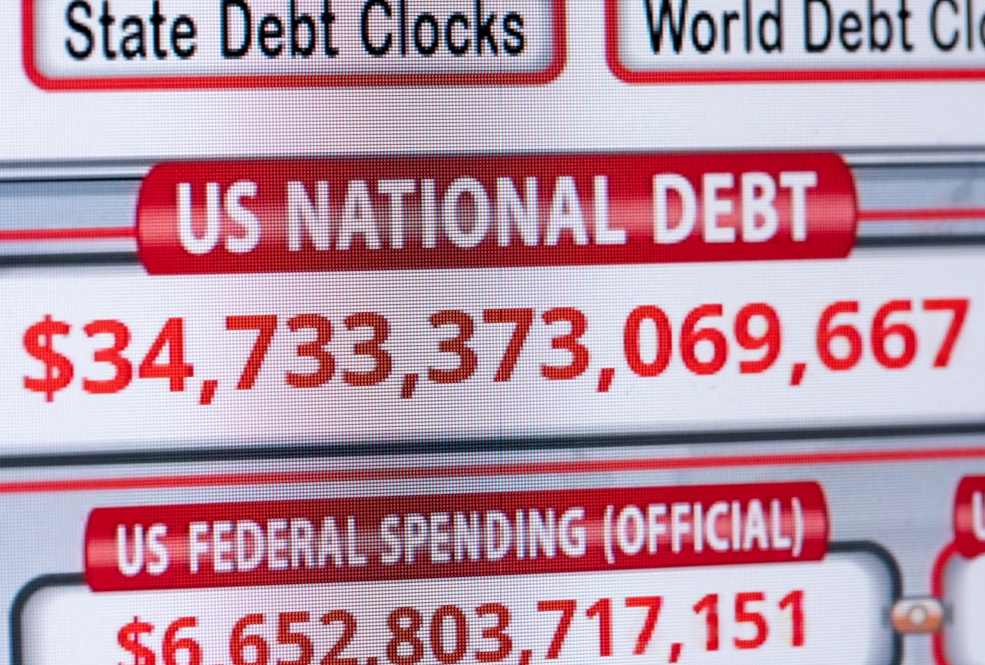

The next president will face a difficult fiscal context.

Fiscal responsibility is not a priority in this election.

Since mid-2022, when the Federal Reserve was in the midst of its aggressive hiking cycle, investors piled over $1.6 trillion into money market funds, which include Treasury bills.

The Northern Trust Economics team reacts to the Fed's decision and shares its outlook for U.S. growth, employment and inflation.

MSCI boosted India’s weighting in the MSCI Emerging Markets Index and reduced China’s in its latest quarterly rebalance, continuing long-term trends.

With attractive valuations, emerging market equities look like a good opportunity. A factor investing strategy, designed well, may enhance performance and help manage some key risks.

How rapidly should the Fed cut rates?