Restructured debt has often outperformed the broader municipal bond market as issuers emerge from bankruptcy with higher debt-servicing capacity.

Conventional wisdom says urban residents will flee cities in droves in response to higher taxes and the COVID-19 pandemic. But will that really come to pass?

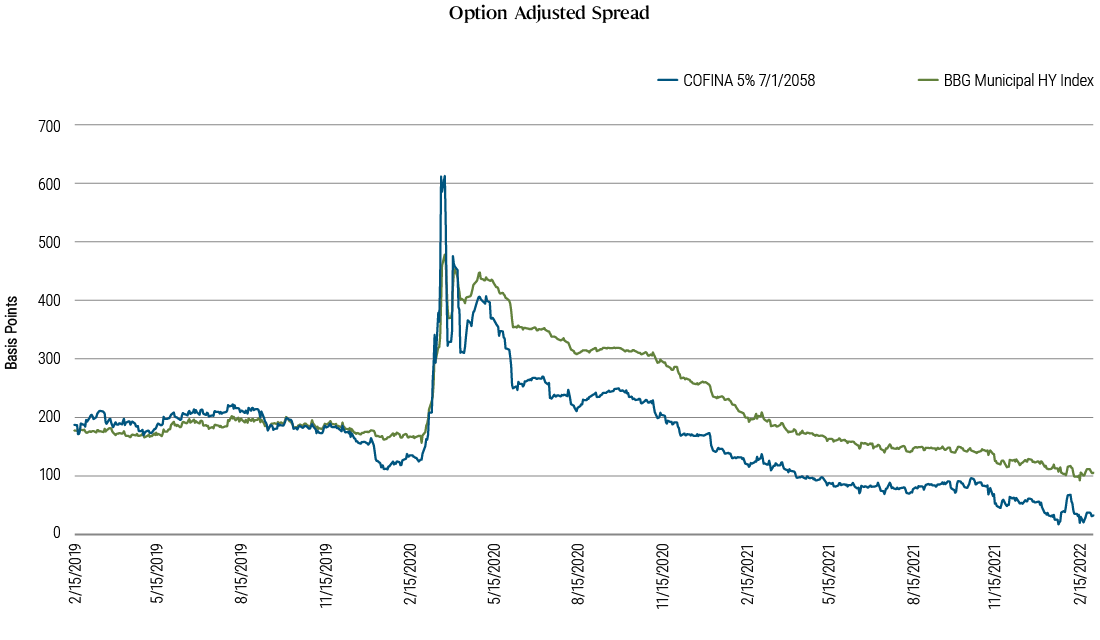

Liquidity could remain challenged, but valuations may be attractive for long-term investors.

Municipal bond investors worried by the 1st U.S. Circuit Court of Appeals’ affirmation of a lower court’s decision regarding the Puerto Rico Highway Transportation Authority should rest a bit easier: The ramifications will likely be limited.

We expect policy will continue to drive municipal bond markets in 2018, if more constructively than in 2017. Municipal investors may remember 2017 as the year of unrealized policy fear. While the threat of tax reform and its potential to reduce the value of the muni exemption for retail investors loomed large, ultimately it had little impact on individual municipal bonds.

Outcomes from the most recent state budget season, which concluded for most U.S. states on 30 June, underscore the need for caution among municipal bond investors.

The muni backdrop looks benign, but be mindful of potential credit risks.

An active approach to the complex, fragmented municipal bond market may help investors avoid several common drawbacks of passive strategies.

In many ways the filings may mark “the end of the beginning” (as Churchill once said) of this chapter for Puerto Rico.