The muni backdrop looks benign, but be mindful of potential credit risks.

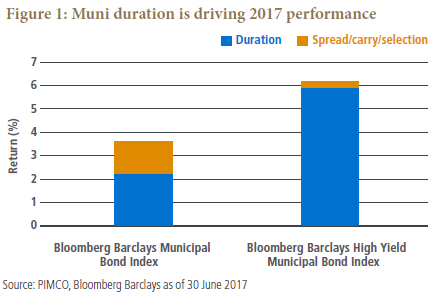

The skies seem clear over the municipal market: Tax reform concerns have abated (for now), mutual fund flows have been positive and supply remains manageable. The tax-exempt market1 has shown solid performance since our May 2017 Munis in Focus, with the Bloomberg Barclays Municipal Bond Index returning 3.57% year-to-date through the end of June and the Bloomberg Barclays High Yield Municipal Bond Index returning 6.13%. That said, we’re seeing some early signs of potential credit flare-ups, with an unusually tough state budget season marked by weak tax collections, federal policy uncertainty and the failure of a number of states to sign budgets before entering the new fiscal year. With potential turbulence looming, we believe active management and credit selection will be key to unlocking opportunities and avoiding credit pitfalls amid any resulting volatility or credit deterioration.

Muni performance: Duration takes the reins

Much of the macro uncertainty and tax reform concern that limited muni performance earlier in the year have now subsided, with improving technicals moving to the forefront to support results. Muni duration, in particular, has been a key driver of returns (see Figure 1), with high yield muni credit spreads remaining somewhat wider since the election.

Fund flows rise as supply tightens

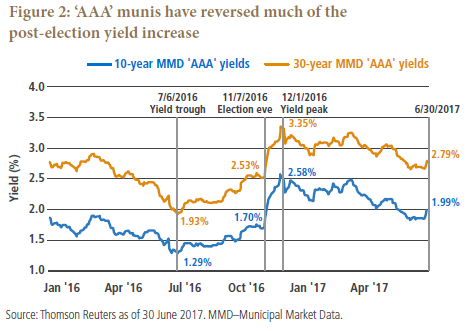

Open-end municipal bond funds have seen $6.8 billion of inflows this year through the end of June, which compares with the $20 billion in outflows in the six weeks following the presidential election. This influx of investable cash has come at a time when primary market supply has decreased, with just $196 billion in new issuance in the first half of 2017, 13% lower than in the same period last year. Moreover, the supply of muni debt stock outstanding has contracted by $23 billion through June 2017 (according to Bloomberg), as maturing debt has outpaced the issuance of new money supply. With a boost from the positive technical backdrop, ‘AAA’ rated munis have reversed roughly 70% of their post-election yield increase (see Figure 2).

High yield tax-exempt bonds still look attractive

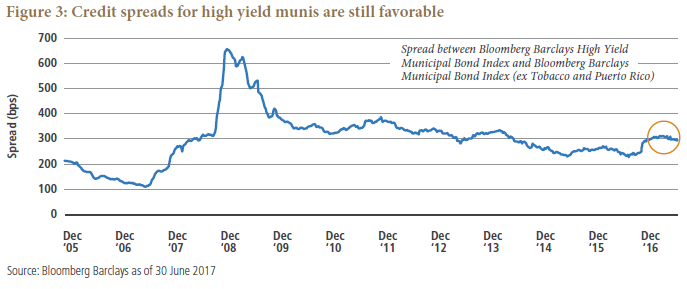

Spreads on traditional high yield (HY) muni bonds (excluding Puerto Rico and Master Settlement Agreement (MSA) tobacco) versus the Bloomberg Barclays Municipal Bond Index remain roughly 50 basis points (bps) wider than they were before the presidential election (see Figure 3).

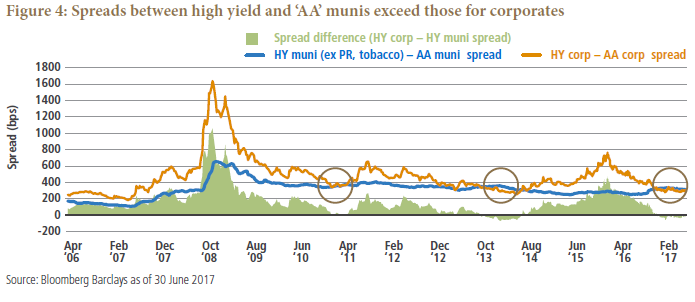

High yield muni spreads also continue to look attractive relative to HY corporate spreads: For only the third time in the past decade, the spread of HY to ‘AA’ munis actually exceeds the spread of HY to ‘AA’ corporates (see Figure 4). It’s worth noting that in the 12 months immediately following the prior two instances – in 2011 (after the 60 Minutes report predicting hundreds of billions of muni defaults and MSA tobacco downgrades) and 2014 (following the Fed “taper tantrum,” Detroit’s bankruptcy filing and the initial drawdown of Puerto Rico debt) – HY munis outperformed HY corporates by 7.64% and 13.64%, respectively.

One note of caution, however: The FDA’s recent announcement that it plans to limit and regulate the amount of allowable nicotine in cigarettes in the future could create headwinds for the MSA tobacco market (as cash flows on these bonds are directly related to the level of cigarette consumption). Any selling pressure in this sector could negatively affect price performance of HY muni funds and may lead to outflows in the space, so this development is worth monitoring closely.

Muni backdrop looks favorable, but heed emerging risks at this stage in the cycle

Though our current view of the muni market is generally sanguine, we recognize that the U.S. has now entered its ninth year of expansion – and despite the adage that expansions do not die of old age, PIMCO sets the risk of a global recession sometime in the next five years at around 70%. Accordingly, we think investors must remain vigilant about screening credit and repositioning portfolios ahead of potential credit challenges.

The troubled budget process puts muni investors on alert

Outcomes from the most recent budget season, which concluded for most states on 30 June, underscore the need for caution: 10 states entered the new fiscal year without a signed budget, and 23 states made midyear budget cuts in fiscal 2017, the most since 2010 (according to the National Association of State Budget Officers). Moreover, general fund expenditures in fiscal 2018 are expected to increase just 1% in nominal terms, an anemic rise compared with the historical average of 4.2% for the past 25 years.

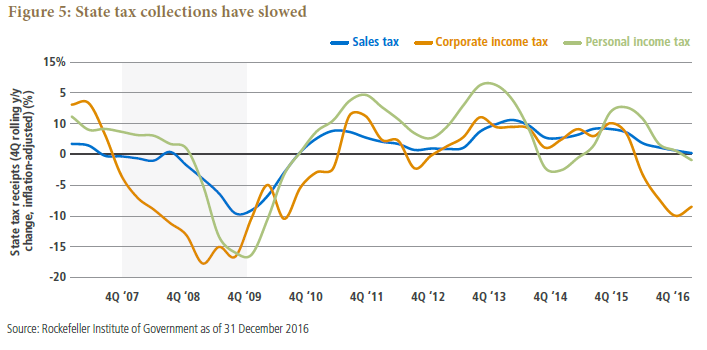

We believe a confluence of factors contributed to these outcomes, including the oft-cited higher pension costs, slowing tax collections (see Figure 5) and continued economic weakness across energy-producing states. And an additional source has added to the budget difficulties: Since the beginning of the year, federal policy uncertainty and political polarization have emerged as a credit threat to many cities and state capitols.

Political risk is perhaps more acute today than at any time in U.S. municipal history, and political polarization and attendant legislative gridlock are extending beyond the federal level to affect state governments. We expect that as the municipal market faces these realities – along with the macro trends of slower economic growth, weaker revenues and higher cost structures – the frequency of credit downgrades and bouts of credit spread widening may increase for issuers that are unable to adjust. For investors, proactive assessment of risk will be critical.

Are investors mispricing risk?

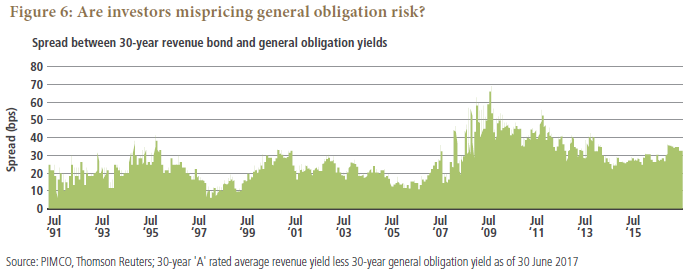

We’ve observed various recent instances of what we view as mispriced credit risk in the general obligation (GO) segment of the municipal market. GO debt typically trades rich relative to similarly rated essential service revenue bonds (see Figure 6), based in part on a perception that a pledge of the “full faith and credit” or taxing authority of the issuer could support a GO claim without limitation. However, not all GOs are created equal, nor are debtors, and many investors may overestimate GO credit quality and misprice the risk.

The unfolding of recent fiscal crises (in Detroit and Puerto Rico, for example) has demonstrated that multiple claims often compete for limited resources, and when this occurs, the positioning of creditors in the payment waterfall may diverge from expectations. For instance, GO bondholders may find their priority subordinate to bonds for essential services (which may be subjectively defined) and other perceived priority claims of officials and politicians (e.g., pensions).

Credit pitfalls and credit opportunities: knowing the difference

While investors may be quick to draw comparisons between deteriorating credits and those with real solvency and liquidity concerns (such as Puerto Rico and Detroit), municipal defaults and bankruptcies remain relatively rare, and selling without first evaluating and dissecting the potential credit risk may crystalize losses. Successfully differentiating between a hopeless fiscal crisis and one that offers the debtor a way out can be a significant driver of alpha generation and is among the primary goals of our municipal credit research.

Case study: budget woes in the “Land of Lincoln”

Illinois’ budget woes exemplify the importance of differentiating credit risk from true default risk, and illustrate both the challenge and the potential opportunity of forecasting political risk in times of fiscal stress.

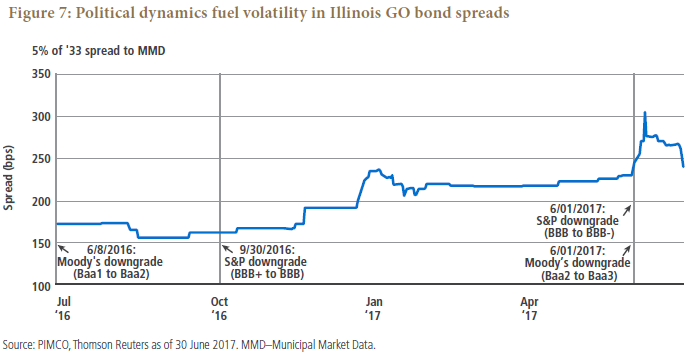

Illinois is highly indebted, with over $130 billion of unfunded pension liabilities. The state has also struggled to strike a budget compromise between the Republican governor and its Democratic general assembly in each of the past three fiscal years, resulting in a series of limited stop-gap spending bills that allowed unpaid bills to climb to more than $15 billion. Moody’s and S&P both downgraded the state in June to one notch above non-investment-grade, which contributed to widening of spreads for the state’s GO securities. The state failed to pass a budget during its regular legislative session (ended 30 June), but in early July Illinois’ House and Senate passed a budget bill and an income tax hike and were able to successfully override Governor Bruce Rauner’s vetoes.

Illinois’ significant structural challenges and political polarization contributed to volatility in bond prices and spreads (see Figure 7). Between 31 May and the end of June, spreads between Illinois 10-year GO bonds and the ‘AAA’ curve widened by 86 bps to a recent high of roughly 305 bps, due in part to the threat of a rating downgrade to junk status. After the budget and tax hike passed, spreads tightened by 106 bps to 225 bps. Spreads also widened by more than 50 bps between September 2016 and May 2017 without any downgrades or changes in outlook by the rating agencies. The agencies’ actions at the conclusion of this period lagged the credit spread widening and illustrate the need for diligent monitoring of credit risk.

While the budget impasse in Illinois created a number of challenges, our portfolio positioning continued to reflect our view that these issues did not materially increase the state’s probability of default. Despite high balance sheet leverage emanating from one of the lowest-funded pension systems in the nation, Illinois has been funding its pension contributions better in recent years (over 80% of the required contribution since 2013), keeping funding levels relatively flat. In addition, fundamental macro conditions in the “Land of Lincoln” remain relatively sound, if not without challenges. The state’s economy remains well diversified, and income taxes – despite a 32% headline increase – are still reasonable for the region and are not outsized as a percent of gross state product relative to nationwide averages.

Knowing the difference between an impending default and a manageable – if painful – credit hurdle can be the difference between incurring a loss and generating alpha.

Investment takeaways

While we remain generally constructive on the municipal market, a strong technical backdrop does not guarantee performance. We remain underweight GO credit that we view as inappropriately priced and are taking heed of early signs of coming turbulence.

We maintain a structural portfolio bias in favor of essential service revenue bonds, which tend to trade at higher yields than comparably rated GO bonds, and often come with less political risk and may offer better downside risk protection in the form of treatment under the federal bankruptcy code. And while many muni managers state a preference for essential service revenue bonds over GOs, among the 10 largest investment grade muni open-ended funds and ETFs (by assets under management), the median allocation to GOs is 23.15% (according to Bloomberg as of 30 June 2017, most recent published holdings). This is marginally lower than the Bloomberg Barclays IG Municipal index allocation of 25% GO bonds, which indicates that investors are only modestly underweight GOs relative to revenue bonds.

While Puerto Rico and Illinois have grabbed recent credit headlines in the muni market, we’re seeing fiscal challenges to varying degrees elsewhere as well. New Jersey and Connecticut, for instance, both face high balance sheet leverage from unfunded retirement obligations; moreover, Connecticut’s Capitol, the City of Hartford, recently hired financial advisors and may be on the brink of bankruptcy. Investors must determine whether credit stress for these and other entities presents an opportunity (as with Illinois) or a credit pitfall (as with Puerto Rico and Detroit).

As part of our investment process, we continually monitor the municipal universe for credit risk in all its forms (downgrades, spread widening and default risk). By establishing a framework to understand the forms of credit risk in an investment and then setting valuation parameters to guide buy and sell decisions, we aim to help investors identify attractive opportunities and avoid potential losses.

1 The term “tax-exempt” market refers to income from municipal bonds, which is exempt from federal tax. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax.

Past performance is not a guarantee or a reliable indicator of future results.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

The Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long term tax-exempt bond market. To be included in the Index, bonds must be rated investment-grade (Baa3/BBB- or higher) by at least two of the following ratings agencies: Moody’s, S&P and Fitch. If only two of the three agencies rate the security, the lower rating is used to determine index eligibility. If only one of the three agencies rates a security, the rating must be investment-grade. They must have an outstanding par value of at least $7 million and must be issued as part of a transaction of at least $75 million. The bonds must be fixed rate, have a dated-date after December 31, 1990, and must be at least one year from their maturity date. Remarketed issues, taxable municipal bonds, bonds with floating rates, and derivatives, are excluded from the benchmark. The Barclays High Yield Municipal Bond Index is a rules-based, market-value-weighted index that measures the non-investment grade and non-rated U.S. tax-exempt bond market. To be included in the Index, bonds must be rated non-investment-grade (Ba1/BB+/BB+ or below) using the middle rating of the following rating agencies: Moody’s, S&P and Fitch. If only two of the three agencies rate the security, the lower rating is used to determine Index eligibility. If only one of the three agencies rates a security, that rating is used. Non-rated issues are also eligible. Bonds must have an outstanding par value of at least $3 million and must be issued as part of a transaction of at least $20 million. The bonds must be fixed-rate, have a dated-date after January 1, 1991, and must be at least one year from their maturity date. Defaulted securities, remarketed issues, taxable municipal bonds, bonds with floating rates, partially pre-refunded bonds where no new securities are issued, illiquid securities that lack reliable pricing, and private placements are excluded from the benchmark. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

© 2017, PIMCO

CMR2017-0721-280377

© PIMCO

Read more commentaries by PIMCO