In the Warsh Fed's new era of two-way risk, bonds offer something rare: potential downside risk mitigation that investors get paid to hold.

In a world of high starting yields and rupturing economic alliances, investors who actively diversify across regions, sectors, and currencies can be better positioned to pursue durable returns.

Markets have long struggled to price geopolitical risk. Part of the issue is that each flare-up tends to be viewed as a one-off volatility jolt to be weathered and then faded once there is resolution.

Barely a month into 2026, markets have already weathered multiple bouts of rolling, event‑driven volatility. Geopolitical surprises and policy pivots have triggered sharp price moves from the U.S. to Japan to Europe, from sovereign bonds to currencies to mortgages.

Mortgage bond reinvestment could be the Federal Reserve’s most effective and immediate tool to unlock the housing market – without even touching interest rates.

Investors enjoyed broad gains across major asset classes in the first half of this year, but they endured considerable market swings to earn those returns.

Rapid U.S. policy changes pose challenges for investors accustomed to a global financial system anchored in U.S. markets and assets.

Lofty U.S. stock valuations call for a renewed focus on risk assessment and portfolio diversification.

Amid concerns about the impact of rising deficits on U.S. Treasuries, it helps to differentiate bond investments by maturity, credit rating, and global relative value.

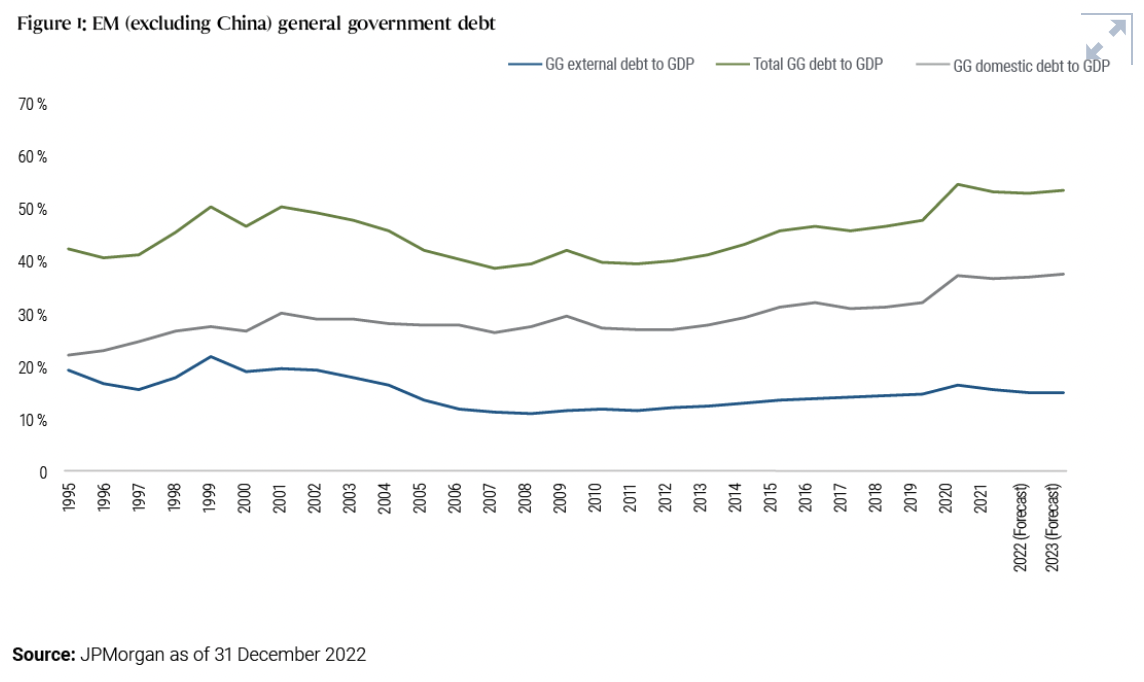

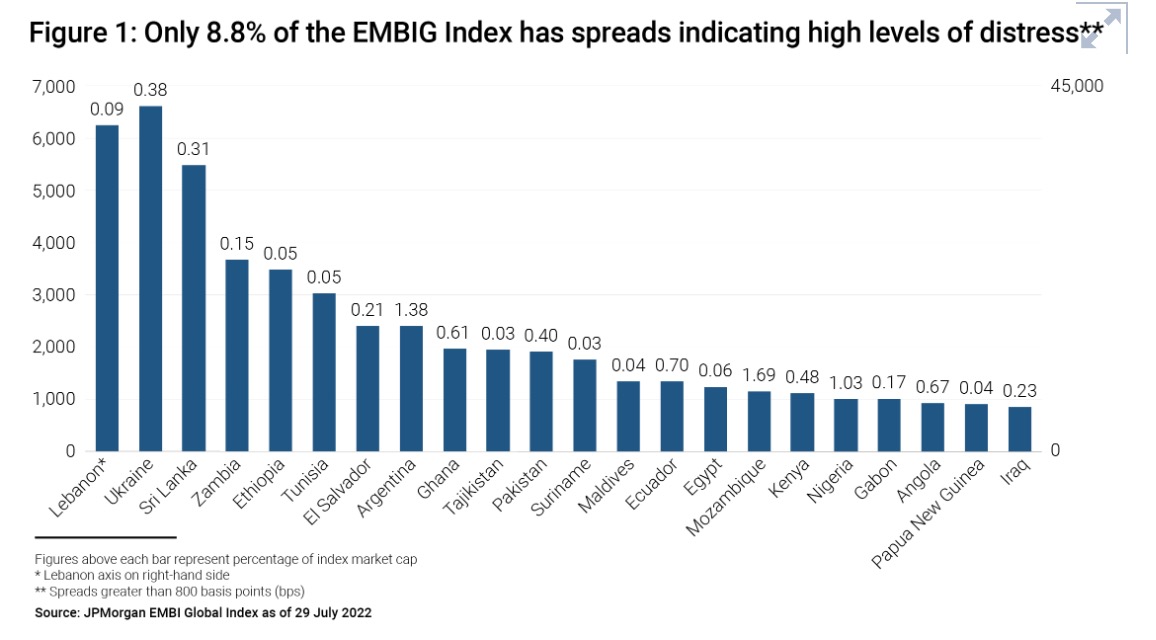

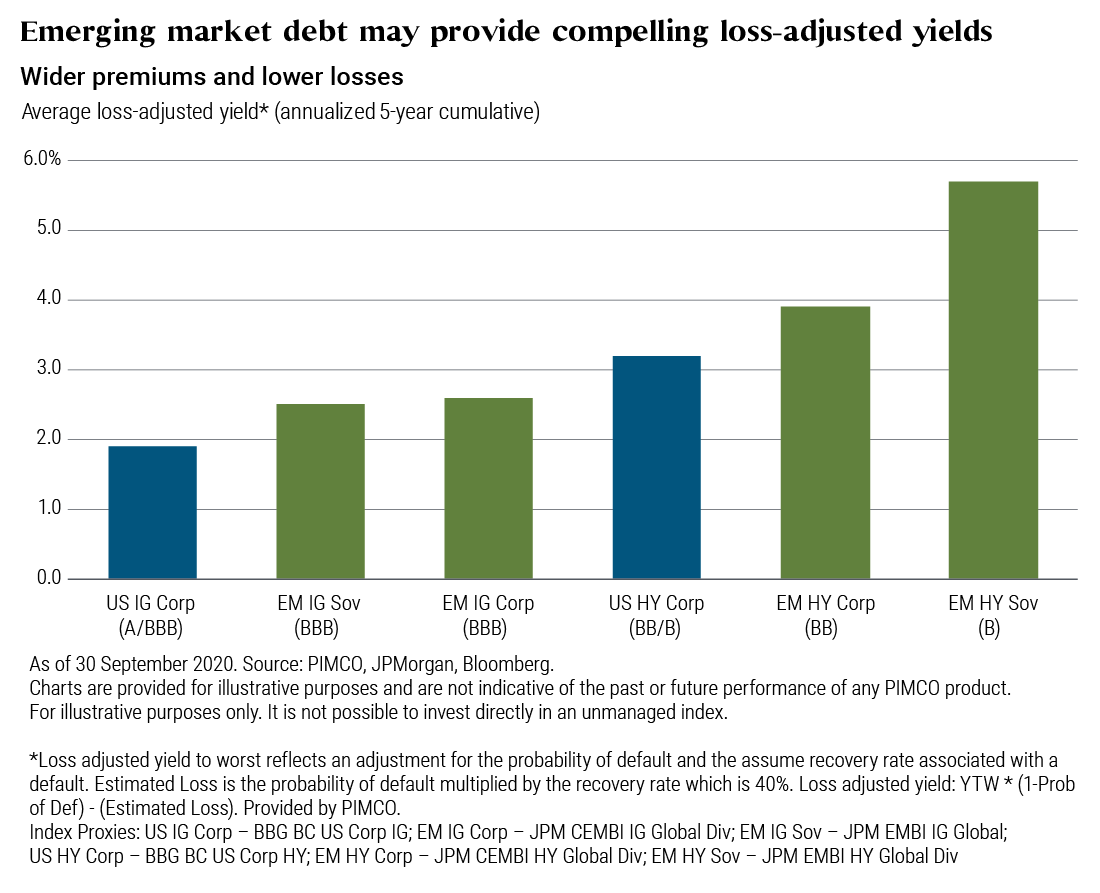

Many investors today use EM debt for the wrong reasons, manage it imprudently, or overlook the best parts.

Balanced risks to inflation and employment indicate it’s time for the Fed to normalize interest rates, enhancing a positive backdrop for bonds.

In this PIMCO Perspectives, we explore the dispersion playing out across monetary policy and financial markets.

In this PIMCO Perspectives, we examine how the return of elevated bond yields comes at an opportune time to consider shifting out of cash.

This PIMCO Perspectives assesses how the term premium’s 40-year downturn could start to reverse.

After withstanding a multitude of global challenges last year, emerging markets look poised for improvement as inflation recedes and the path of monetary policy comes into view.

Inflation is receding and real interest rates are climbing in EM after a year of tightening monetary policy.

Emerging market valuations appear attractive, but country-specific risks can be critical to monitor amid global inflation and rising interest rates.

The varied responses of individual countries to global inflationary pressures have contributed to elevated real-rate differentials between developed and emerging markets.

Natural herd immunity in predominantly young emerging markets populations looks set to offset slower vaccine rollouts, setting the stage for a resurgence in economic growth.

A confluence of dynamics are set to accelerate global capital flows to emerging markets amid attractive valuations.

Debt of many emerging market countries can offer robust yields and enhance portfolio diversification, provided the asset manager has the resources and sophistication to avoid potential pitfalls.

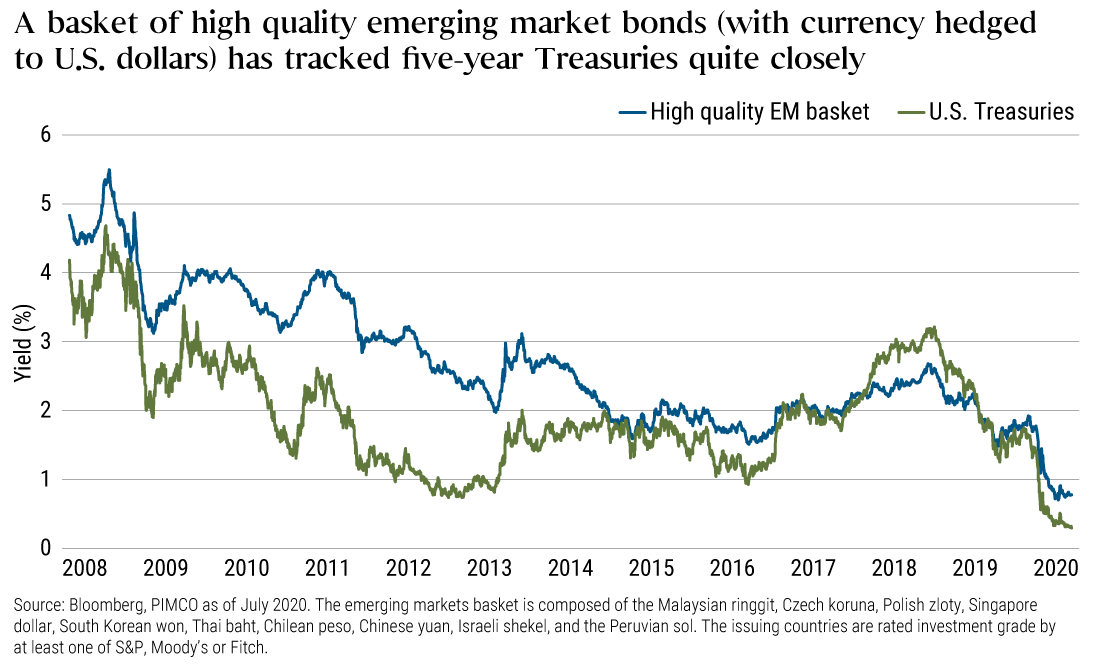

A basket of emerging market bonds may offer the same appeal investors have long sought from U.S. Treasuries.

While we are constructive on the prospects for emerging markets in the year ahead, we think the real potential lies in individual country and thematic opportunities.

Like shock therapy, Argentina’s new lending agreement with the IMF delivers immediate benefits: increased funding and front-loaded disbursements to meet the country’s budget through next year. It also comes with serious side effects, including a likely deep recession in Argentina and the risk of political resistance leading up to the country’s elections in 2019.

During the second most significant repricing in U.S. Treasury bond yields since 2013, emerging market debt has so far significantly outperformed equity, oil and U.S. Treasury beta.

Earlier this year, Argentina, the Czech Republic and Uruguay joined the bellwether benchmark for the asset class, JPMorgan GBI-EM Global Diversified, taking the total to 18 countries. China, Egypt and another three countries may enter the index next year. The inclusions will make the EM local debt asset class much larger, deeper and more liquid.

Many investors are concerned about the risks to growth and the potential for higher inflation in Peru following two recent shocks.