Many investors are concerned about the risks to growth and the potential for higher inflation in Peru following two recent shocks: severe floods stemming from the coastal El Niño and allegations of corruption related to the Brazilian construction conglomerate Odebrecht. Both raise hurdles for the government’s infrastructure push, which is at the heart of President Pedro Pablo Kuczynski’s plan to revive domestic demand and promote growth (see chart below).

In the short term, we think GDP growth should drop closer to the 3% range from the consensus forecast of 3.5%–4.0% six months ago. Yet, even as headwinds increase, we continue to believe that the government’s overall strategy will lead to a new period of dynamism in the Peruvian economy over the medium term. Solid planning, sound fundamentals and improving terms of trade should help significantly, and Peru continues to have many levers at its disposal to achieve its policy objectives.

Peru’s solid economic agenda and ample tools

Under a special 90-day legislative window granted by parliament last year, President Kuczynski’s government enacted 112 reform decrees that provide a solid framework to support its economic agenda. They include measures to facilitate infrastructure projects and a revised fiscal law that will allow the government to pursue slower consolidation and still be bound by a 30%-of-GDP public debt limit.

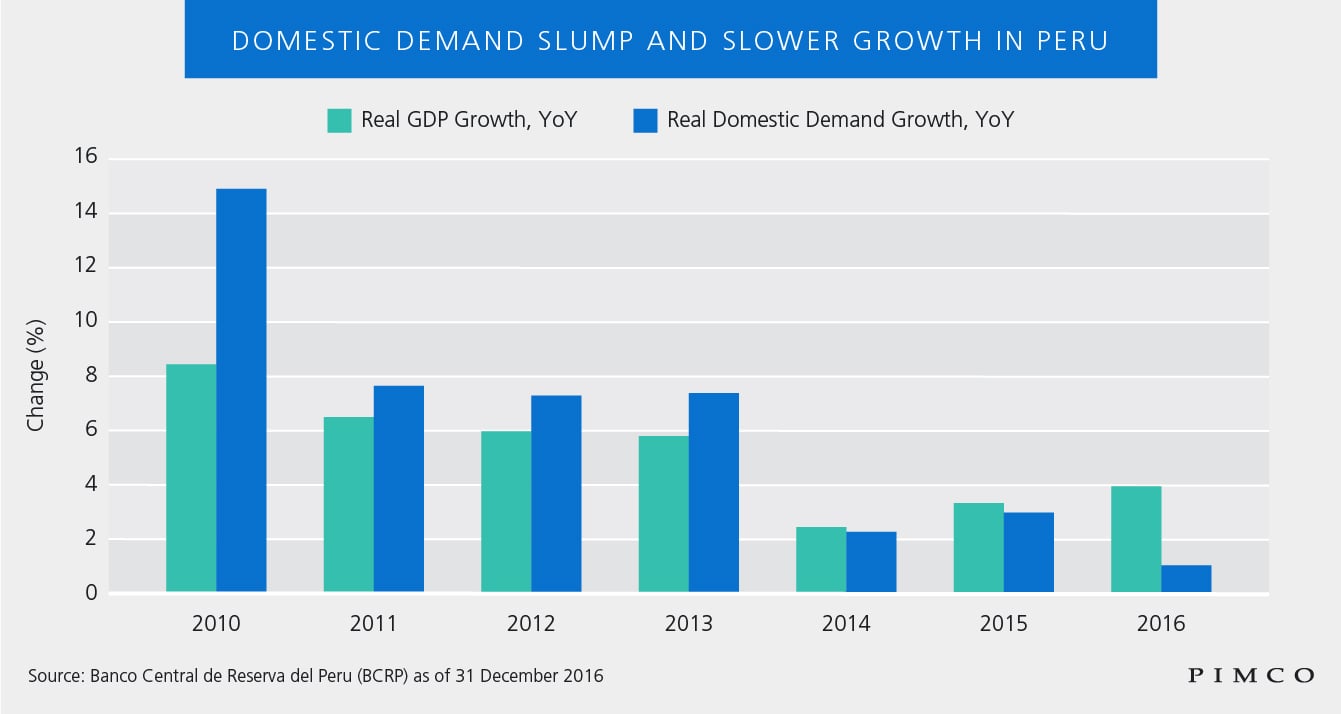

In 2017, the execution of public works and an additional fiscal thrust will provide important support to the economy. The government recently launched a fiscal stimulus of close to 1% of GDP. Reconstruction efforts following the torrential rains will likely require additional resources (possibly leading to a wider deficit), and government investment will also be an important supplement to non-mining private investment, which is expected to grow for the first time in four years. Growth in private consumption should follow, albeit with a lag given the softness in the job market.

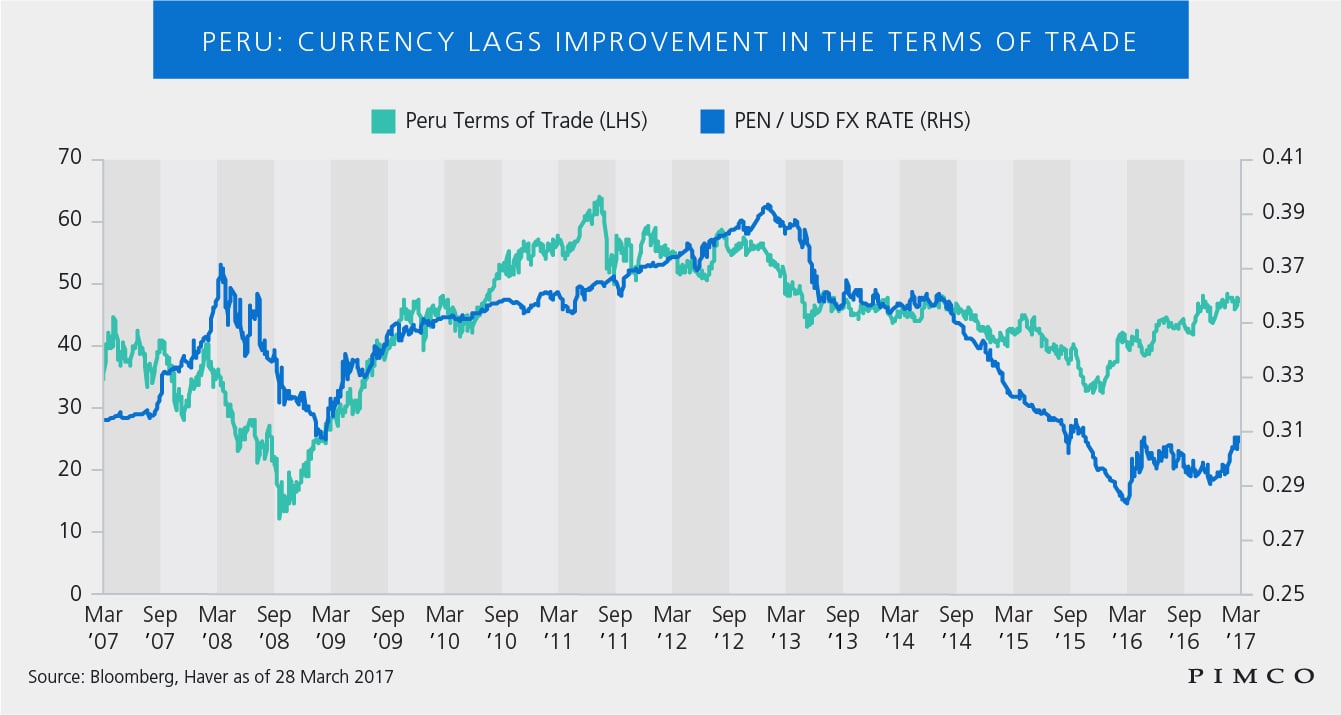

Exports should contribute positively to growth this year as the trade balance reverts to a surplus. The improving terms of trade is an important tailwind to domestic fundamentals and will likely lead to a smaller current account deficit of about 2.6% of GDP in 2017, more than fully financed by foreign direct investment.