Lately, I have been getting many questions about investing in private equity. Such is common during raging bull markets, as individuals seek higher rates of return than the market generates.

Wall Street analysts continue significantly lowering the earnings bar as we enter the Q2 reporting period. Even as analysts lower that earnings bar, stocks have rallied sharply over the last few months.

Financial advisors get a bad rap. Some deserve it; most don’t. The problem for the entire investment advisory and portfolio management community stems from the “career risk” they inevitably face.

Goldman Sachs recently upped its price target to S&P 6300 for the end of this year, along with Evercore ISI upping its year-end target to 6000. Such is not surprising given the strong run in the markets this year.

Over the last decade, there has been an ongoing fundamental debate about markets and valuations. The bulls have long rationalized that low rates and increased liquidity justify overpaying for the underlying fundamentals.

The latest consumer survey data from the New York Federal Reserve had interesting data.

Recently, James Grant, editor of the Interest Rate Observer, was asked about his outlook for interest rates. He sees interest rates moving in a cyclical pattern, potentially rising for another multi-decade period.

More than a few individuals were active in the markets in 1999-2000, but many participants today were not. I remember looking at charts and writing about the craziness in markets as the fears of “Y2K” and the boom of “internet” filled media headlines.

It is always interesting when commodity prices rise. The market produces various narratives to suggest why prices will keep growing indefinitely. Such applies to all commodities, from oil to orange juice or cocoa beans. For example, Michael Hartnett of BofA recently noted.

In 2022, we discussed the market’s deviations from long-term growth trends. That discussion centered on Jeremy Grantham’s commentary about market bubbles.

The future of electricity demand for everything from electric cars to Bitcoin mining to artificial intelligence may also be the cure for our debt concerns.

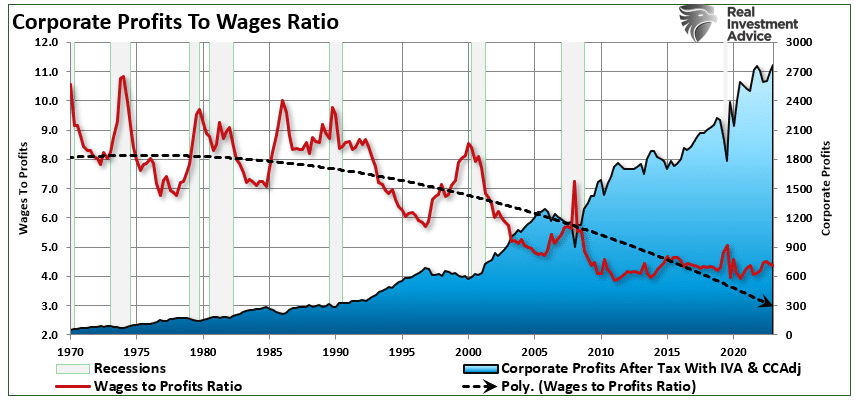

Corporate greed is not causing inflation, despite the claims of many on the political left who failed to understand the very basics of economic supply and demand.

As we discussed recently, Wall Street economists increasingly believe the risk of recession has fallen sharply.

During ripping bull markets, investors often start benchmarking. That is comparing their portfolio’s performance against a major index—most often, the S&P 500 index. While that activity is heavily encouraged by Wall Street and the media, funded by Wall Street, is benchmarking the right for you?

Every year, investors anxiously await the release of Warren Buffett’s annual letter to see what the “Oracle of Omaha” says about the markets, the economy, and where he is placing his money.

While there is much debate over whether another bear market is imminent, weekly moving average crossovers suggest a different outcome for now. There are many current concerns, from geopolitical risk to still inverted yield curves, slowing economic growth, high interest rates, and inflation. Yet, despite those concerns, markets are flirting with all-time highs.

When it comes to the financial markets, investors have a litany of investment vehicles to choose from. The choices are nearly unlimited, from brokered certificates of deposit to complex derivative instruments.

The latest FOMC meeting caused a stock rally as Jerome Powell turned more “dovish” than expected. While Powell did note that progress on inflation has been lackluster, the announcement of the reversal of “Quantitative Tightening” (QT) excited the bulls.

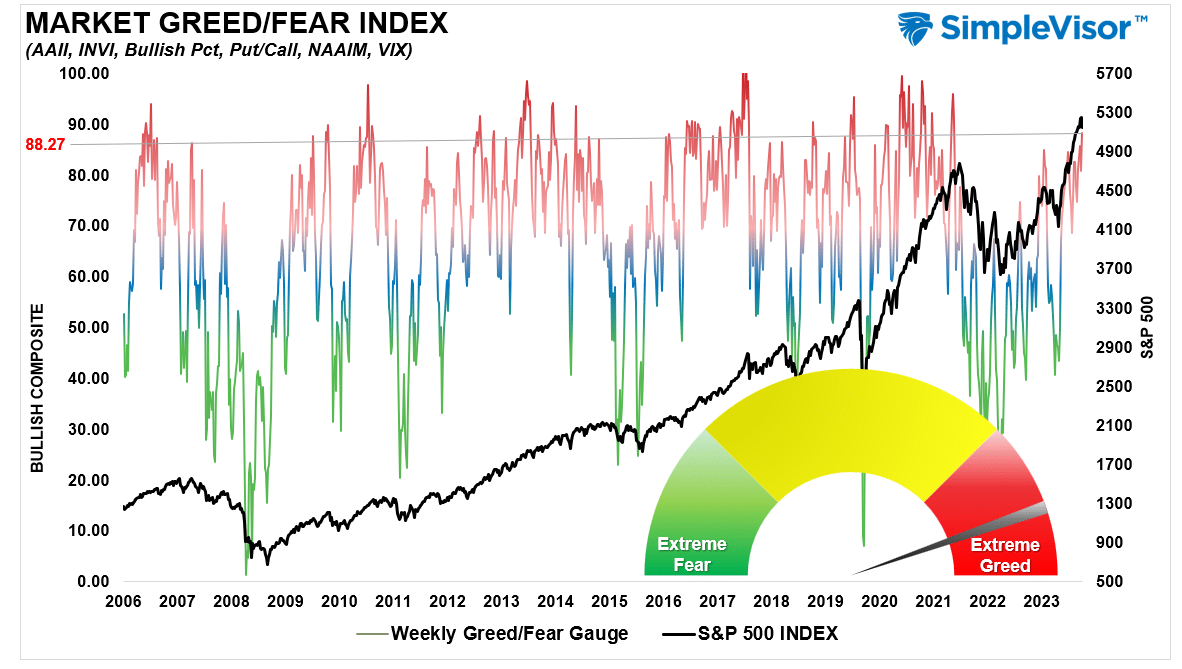

Over the last two weeks, the bullish sentiment index has reversed from extreme greed to fear. The composite net bullish sentiment index, comprised of professional and retail investors, fell from 38.15 to 9.9 in two weeks.

Behavioral traits and cognitive biases are anathemas to portfolio management as they impair our ability to remain emotionally disconnected from our money. As history all too clearly shows, investors always do the “opposite” of what they should when it comes to investing their own money.

Is this just a correction after a strong bullish advance from November, or is the bull market ending?

The latest National Federation of Independent Business (NFIB) survey was an economic warning that departed widely from more robust governmental reports.

Economic “reflation” is becoming the next bullish narrative as equity valuation increases continue to outpace earnings gains, at least according to Gold Sachs and Tony Pasquariello.

While immigration has positively impacted economic growth and disinflation, this story has a dark side.

In the most recent report from FINRA, margin debt levels have surged as bullish investors leverage their bets in the equity market. The increase in leverage is not surprising, as it represents increased risk-taking by investors in the stock market.

Your mother likely imparted valuable investing lessons you may not have known. With Mother’s Day approaching and bullish market exuberance present, such is an excellent time to revisit the investing lessons she taught me.

During running bull markets, much commentary is written on why this time is different and why investors should not worry about market corrections.

Technical measures and valuations all suggest the market is expensive, overbought, and exuberant. However, none of it seems to matter as investors pile into equities to chase risk assets higher. A recent BofA report shows that the increase in risk appetite has been the largest since March 2021.

One of the most interesting conundrums is the surging wealth gap in America. Despite two of the largest bull markets in history since 1980, most Americans struggle with making ends meet and are unprepared for retirement. Such a reality starkly differs from the belief that rising asset prices benefit the masses.

It is long past the time that we face the fact that “Social Security” is facing a retirement crisis. In June 2022, we touched on this issue, discussing the stark realities confronting Social Security.

With the last half of March upon us, the blackout of stock buybacks threatens to reduce one of the liquidity sources supporting the bullish run this year.

Household equity allocations are again sharply rising, as the “Fear Of Missing Out” or “F.O.M.O.” fuels a near panic mentality to chase markets higher.

Over the last few years, digital currencies and gold have become decent barometers of speculative investor appetite.

Presidential elections and market corrections have a long history of companionship. Given the rampant rhetoric between the right and left, such is not surprising. Such is particularly the case over the last two Presidential elections, where polarizing candidates trumped policies.

Valuation metrics have little to do with what the market will do over the next few days or months. However, they are essential to future outcomes and shouldn’t be dismissed during the surge in bullish sentiment.

After over two years, retail investors, also known as the “dumb money,” are almost back to breakeven.

I revisited that original post a couple of weeks ago as the market approached its 5000 psychological milestone. Since then, the entire market has surged higher following last week’s earnings report from Nvidia (NVDA).

Recently, retail investors have started chasing small-cap stocks in hopes of both a rate-cutting cycle by the Federal Reserve and avoiding a recession.

Don’t fear all-time highs in the market. Such is a natural response for investors who are concerned about market risk. However, rather than fearing market exuberance, we must understand what drives it.

Regarding the surprisingly strong employment data, Fed Chair Powell said the quiet part out loud. The media hopes you didn’t hear it as we head into a contentious election in November.

While the bulls remain entirely in control of the market narrative, divergences and other technical warnings suggest becoming more cautious may be prudent.

The cost of housing remains a hot-button topic with both Millennials and Gen-Z. Plenty of articles and commentaries address the concern of supply and affordability, with the younger generations getting hit the hardest.

Of course, the market peaked in January 2022, just four months later, at 4796.56. Fast forward 2-full years of returning investors to breakeven, and the market is again approaching that magical round number of 5000.

I received an email this past week concerning George Soros’ “Theory Of Reflexivity.” It’s an interesting question, and I have previously written about the “Theory of Reflexivity.” Notably, this theory begins to resurface whenever markets become exuberant.

As the financial markets grind higher, retirement savers have consciously decided to add more to equity risk. Such was the result of a recent Bloomberg survey.

As money market account balances soar, the mainstream media again proclaims, “There is $6 trillion of cash on the sidelines just waiting to come into the market.”

As the stock market hit all-time highs this past week, there remains an interesting disconnect from the more dour economic concerns of the average American. A recent survey by Axios, a left-leaning website that supports the current Administration, addressed this issue.

As we get ready to review the Q4 earnings report, stocks have rallied sharply over the last two months

Economic growth continues to defy expectations of a slowdown and recession due to continued increases in deficit spending.

A stunning post from VisualCapitalist showed a poll of 8550 investors and 2700 advisors and the gap between the two of future portfolio return expectations. The poll was global; however, I will focus on this post’s domestic portfolio return expectations.