AI infrastructure spending is driving record equity market raisings and has lifted expectations for long-term GDP growth in the US. But what will happen to growth when the AI capex surge has peaked? Today’s elevated long-bond yields suggest that the market expects AI-related productivity gains to support faster growth over the longer term. But will they? To us, the likely extent of such gains is unclear.

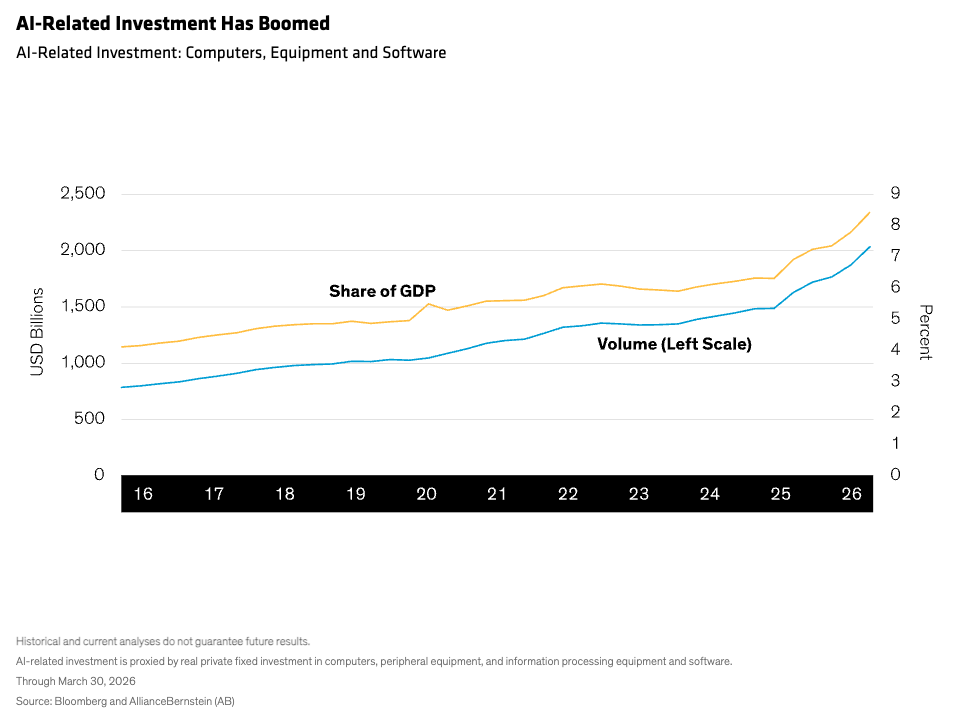

Though still in its early stages, the AI revolution has already made a significant contribution to economic growth through capital expenditure (capex) related to the build-out of AI infrastructure. In the US, it’s boomed in dollar terms and as a share of GDP (Display).

The volume of capex is expected to remain high for some years, but there are signs that its growth rate may have peaked. This has implications for AI’s contribution to GDP growth

Capex Growth Is the Key Trend to Watch

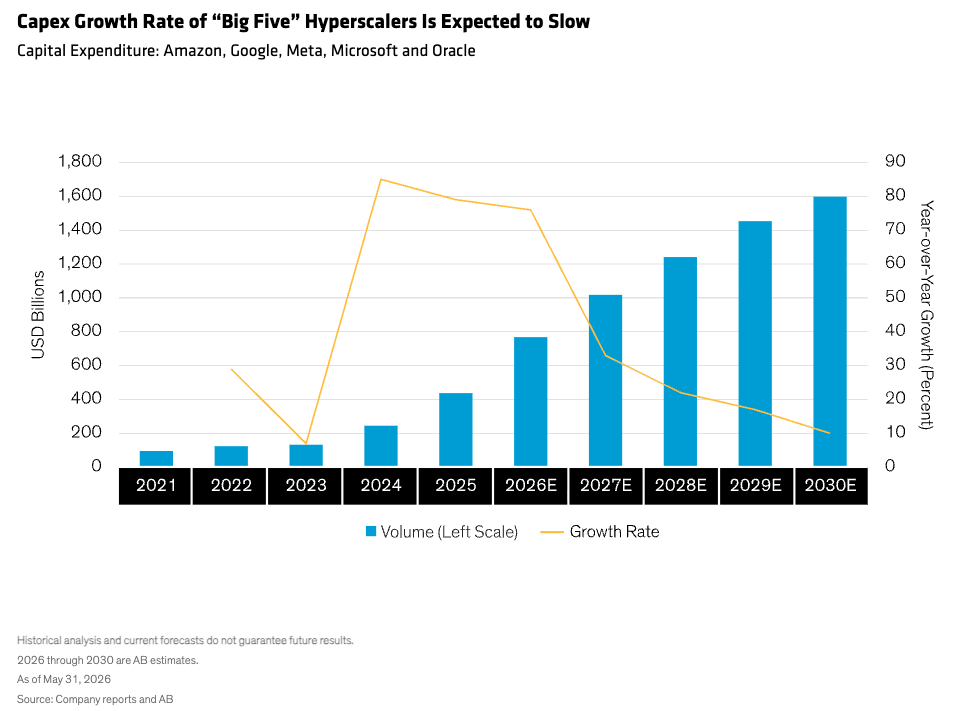

The five big hyperscalers—Amazon, Google, Meta, Microsoft and Oracle—account for much of the capex and provide a pointer for the industry-wide trend (Display).

Their combined investment has exploded from less than $100 billion in 2021 to an estimated $768 billion in 2026 and is projected to reach nearly $1.6 trillion in 2030. Downside risks to these figures include the physical constraints of finding land, power, labor and water to supply the data centers. Rising input costs across a range of AI-related hardware—such as graphic processing units, central processing units and dynamic random-access memory—threaten the return on AI investments and the cycle’s sustainability.

And there are potential funding challenges. So far, the hyperscalers have financed growth mainly internally. They will likely continue to generate huge cash flows, but the liquidity may not be enough, beyond 2027, to fund the volume of capex required.

That said, physical constraints are expected to slow and prolong the boom rather than stop it, and the hyperscalers will likely fund capex increasingly from debt and equity markets. There are upside risks to the figures too: AI companies tend to underestimate how much they will spend (capex plans were revised upwards by 131% between May 2025 and May 2026) and one leading tech CEO has said that spending could be as high as $4 trillion in 2030.

But in our view the key trend to watch, in terms of implications for long-term GDP growth, is the growth rate of AI capex. This has fallen from a peak of 85% in 2024 to an estimated 76% in 2026 and is expected to continue to fall through 2030.

No Answers Yet on AI Productivity Boost

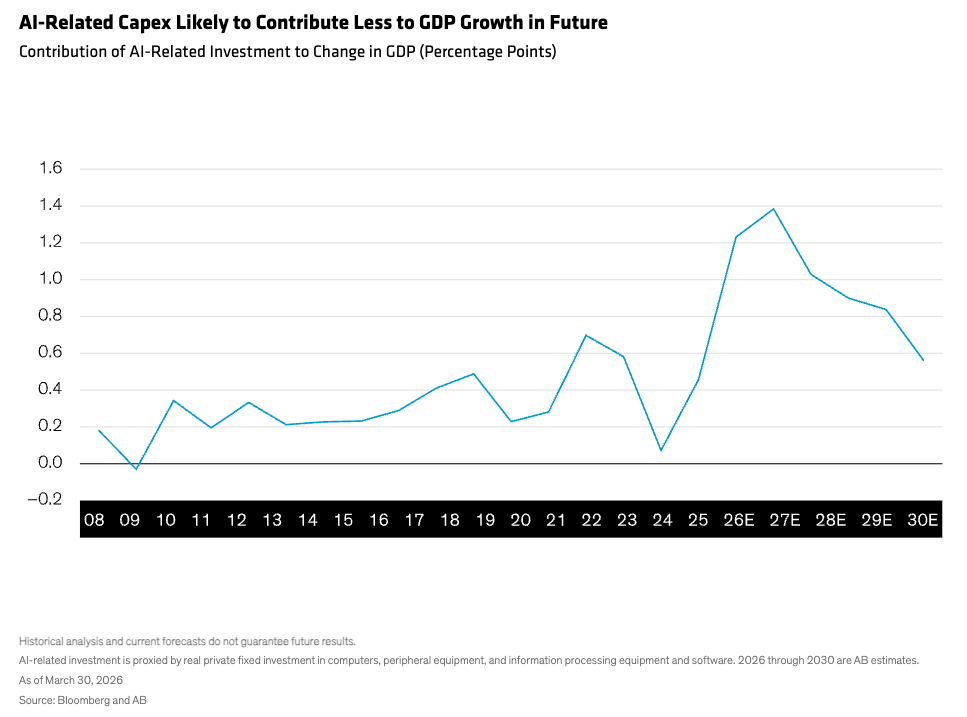

As the AI capex growth rate falls, its contribution to the change of GDP will also fall. If we assume it accounts for 1.5 percentage points of growth in 2026, that share, based on the forecasts above, will roughly halve between 2026 and 2030 (Display).

This is the shortfall that AI-related productivity must cover for AI’s contribution to GDP growth to remain constant. But whether that’s possible remains to be seen. While US productivity has improved in the last few years, research by the Federal Reserve Bank of San Francisco suggests that the gains have been mostly labor-related rather than economy-wide and remain short of the enormous technology-driven gains of the 1990s.

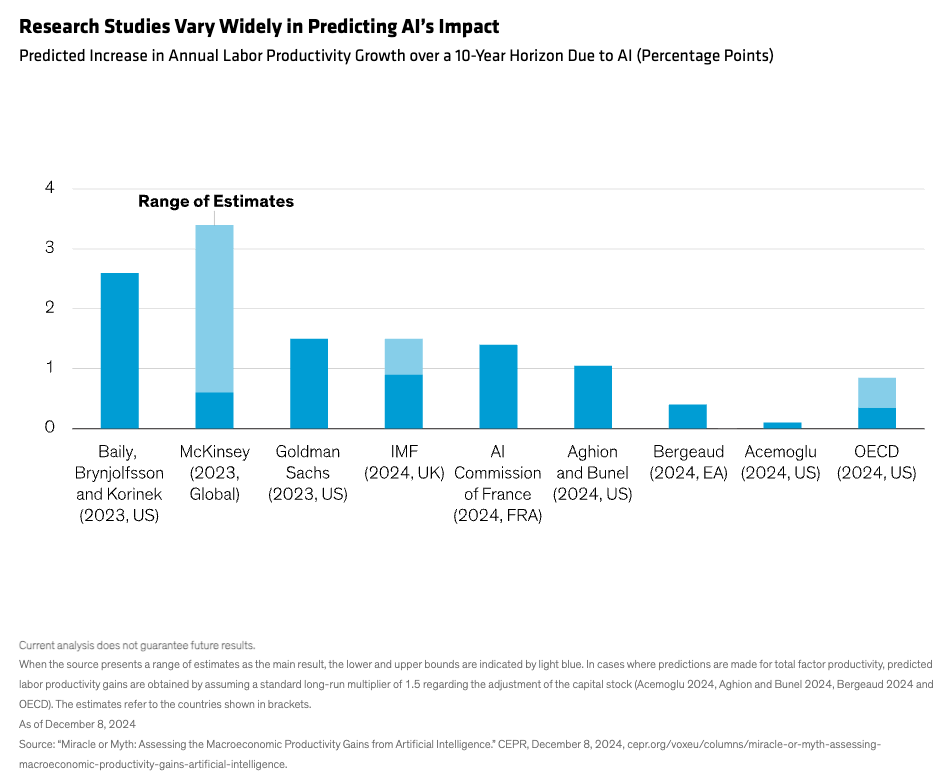

Also, beyond 2030, as the headwinds from declining AI capex growth fade, the economy will continue to face downward forces such as climate change, geopolitical risks and so on. Will AI-related productivity compensate? Indeed, what impact will AI have on growth generally? Researchers differ markedly in their estimates (Display).

The estimates average around 1%, but the range, from 0% to 3.5%, is too wide to be conclusive. In short, the contribution of AI-related productivity to long-term growth remains an open question. The risk for investors is that, if productivity gains prove insufficient, the market may unwind its recent re-pricing of growth and rate expectations.

Investors Should Have a Dual Focus

Investors, in our view, should apply a dual focus to the AI revolution, weighing short-term developments against long-term uncertainties. In the short term, AI’s impact on capital markets looks set to grow, especially as more companies fund themselves externally.

AI companies are becoming significant borrowers in global credit markets. Participants include not just hyperscalers but suppliers too, some of which issue bonds collateralized by, for example, critical IT hardware or hyperscalers’ signed data-center leases. Such financings increase leverage across the supply chain.

In equity markets, Google’s parent, Alphabet, and Elon Musk’s SpaceX have raised $85 billion and $75 billion respectively, mainly for AI initiatives. As long as the equity and debt markets remain open to fund massive AI capital investments, the AI capex cycle will continue. But if investors collectively decide the demand is too much, the cycle could abruptly turn.

Investors should note that, among smaller and more speculative stocks, the falling rate of AI capex growth may lead to squeezed multiples and lower valuations, in our analysis.

Given the scale and speed of the AI revolution, we expect the volume of capex to stay high in the short-to-medium term, but the outlook is not without risk. Beyond that horizon, we think investors should continue to monitor AI’s potential to improve productivity. Expectations might change.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

More Leveraged and Inverse Funds Topics >