Key Takeaways

-

All eyes turn to the Magnificent 7 this week as Alphabet, Meta, Microsoft, Amazon and Apple all report Q1 2026 results.

-

The S&P 500® is projected to deliver its sixth consecutive quarter of double-digit earnings growth at 15.1%, fueled largely by a powerhouse 46% expansion in the Information Technology sector.

-

Potential earnings surprises this week: Chipotle, Vulcan Materials, Xylem and more

Q1 2026 earnings season shifted into high gear last week, led by UnitedHealth Group’s (UNH) strong beat and raise on Tuesday, which calmed fears over rising medical costs.1 The airline sector was mixed as United Airlines (UAL) posted a massive EPS beat on premium cabin strength2, while Southwest (LUV) struggled with valuation3, and Boeing (BA) surprised to the upside with narrower losses4.

After the bell on Wednesday, Tesla (TSLA) delivered a rollercoaster performance; the stock initially surged on a revenue beat of $22.39 billion and improved margins, but those gains evaporated during the conference call as CEO Elon Musk detailed massive capital spending plans for AI and robotics that spooked investors.5 Meanwhile, IBM saw its stock dive over 7% as a narrow earnings miss and slowing consulting growth overshadowed strong software performance and high free cash flow.6

Intel (INTC) ended the week on a high note when it reported results Thursday after the bell. Revenue for the tech giant increased 7% YoY, driven by an impressive 22% surge in its Data Center and AI segment that easily cleared market expectations.7 Boosted by this momentum and a robust outlook for the next quarter, the stock soared on Friday, trading up roughly 22% and reaching new all-time intraday highs.

On the economic front, Tuesday’s Retail Sales data for March provided a "good news is bad news" moment for the Federal Reserve. Total sales jumped 1.7%, significantly exceeding estimates, though much of that was driven by a 15.5% spike in gasoline spending amid the ongoing Iran conflict. While the top-line number was strong, core retail sales (ex autos, gasoline, building materials and food services) grew a more modest 0.7% after increasing 0.6% in February.8 On Friday, The University of Michigan’s final consumer sentiment index reading for April dropped 3.5 index points to 49.8, making it comparable to the trough seen in July 2022, as households grapple with inflation fears and the economic fallout from the conflict with Iran.9

Read more: Stocks Shook Off the March Dip: Now Q1 Earnings and April Data Take Center Stage

Q1 2026 Scorecard: Growth Perseveres

We are now roughly 28% through S&P 500 reports for the Q1 2026 earnings season, and the early results as tracked by FactSet10 suggest a "glass half full" scenario:

-

Positive Surprises: 84% of S&P 500 companies have beaten EPS estimates and 81% have beaten on revenues, both metrics are above the 1, 5 and 10-year averages.

-

Earnings Growth: The blended growth rate stands at 15.1%, putting the index on track for its 11th consecutive quarter of year-over-year growth, and the sixth consecutive quarter of double digit growth

-

Sector Leaders & Laggards: While Tech and Materials are leading the charge on earnings growth for Q1, Energy, Health Care and Communication Services are all expected to post YoY declines

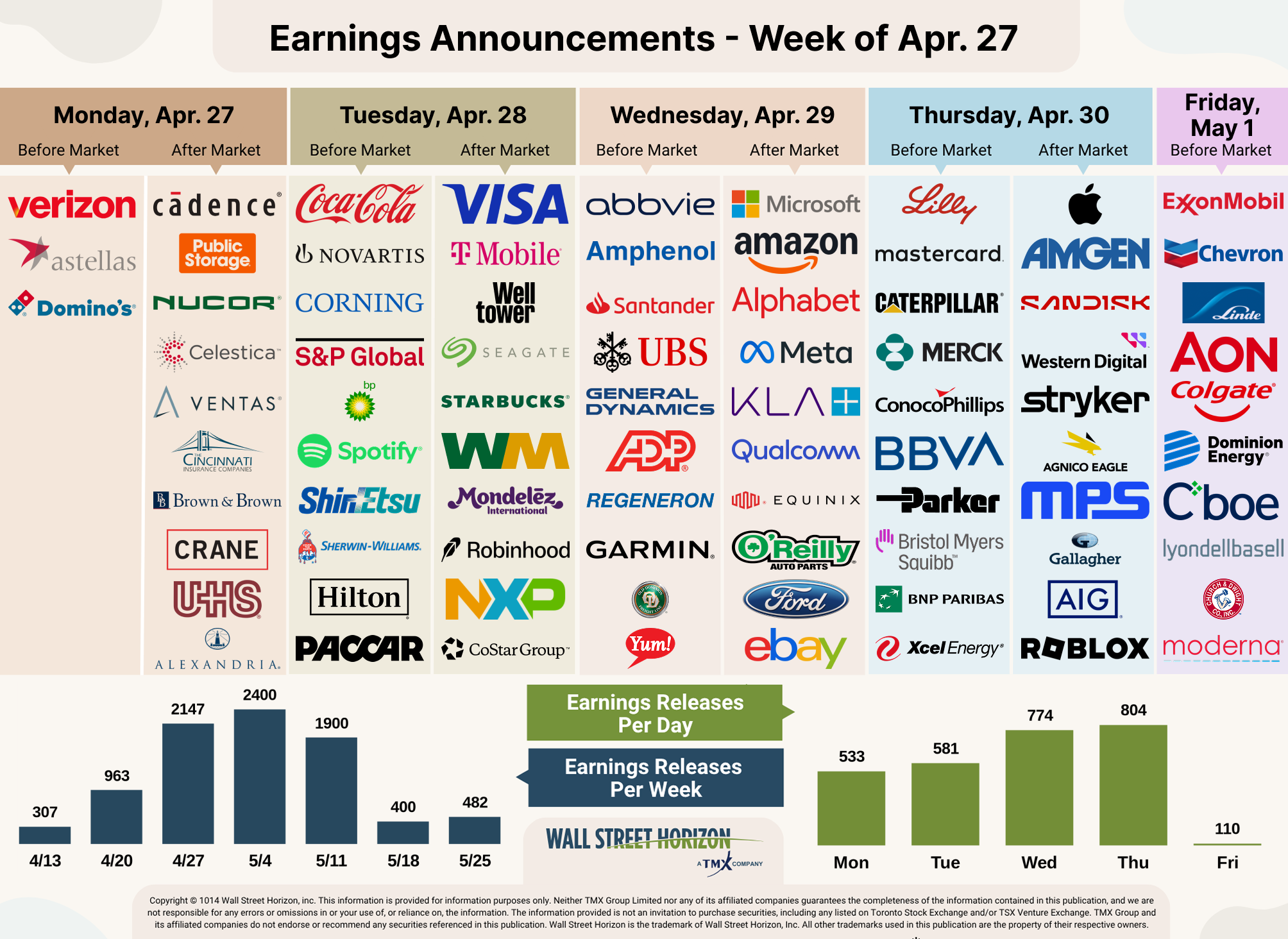

On Deck this Week: Magnificent Seven

This week is the undisputed heavyweight week of the Q1 2026 earnings season, as the Magnificent Seven and major blue-chip Dow components take center stage. Investors will be laser-focused on Wednesday, April 29, when a massive quartet, Microsoft, Alphabet, Meta and Amazon, all report. The primary litmus test for these tech giants will be AI monetization: specifically, whether Microsoft’s 365 Copilot and Google’s Gemini-integrated Cloud are generating enough revenue to justify the billions in capital expenditure they have spent on data centers. For Amazon the market is looking for AWS growth to exceed 20% to prove it isn't losing market share in the AI infrastructure race. On Thursday we get results from Apple. Investors will be looking for stability following the monumental announcement that Tim Cook will step down as CEO on September 1, 2026, to be succeeded by hardware chief John Ternus.

Source: Wall Street Horizon

Outlier Earnings Dates This Week

Academic research shows that when a company confirms a quarterly earnings date that is later than when they have historically reported, it’s typically a sign that the company will share bad news on their upcoming call, while moving a release date earlier suggests the opposite.11

This week we get results from a number of large companies on major indexes that have pushed their Q1 2026 earnings dates outside of their historical norms. Six companies within the S&P 500 confirmed outlier earnings dates for this week. Three of those companies, Allegion (ALLE), Chipotle Mexican Grill (CMG) and Old Dominion Freight Line (ODFL), are later than usual and therefore have negative DateBreaks Factors*. Xylem (XYL), Vulcan Materials (VMC) and Verisk Analytics (VRSK) all have a positive DateBreaks Factors for this week.

* Wall Street Horizon DateBreaks Factor: statistical measurement of how an earnings date (confirmed or revised) compares to the reporting company's 5-year trend for the same quarter. Negative means the earnings date is confirmed to be later than historical average while Positive is earlier.

Q1 2026 Earnings Wave

The peak weeks of the Q1 earnings season are expected to fall between April 27 - May 15, with each week expected to see over 2,500 reports. Currently, May 7 is predicted to be the most active day with 1,168 companies anticipated to report. Thus far, 70% of companies have confirmed their earnings date (out of our universe of 11,000+ global names). The remaining dates are estimated based on historical reporting data.

Source: Wall Street Horizon

The Bottom Line

As the Q1 2026 earnings season enters its most frantic stretch, the market stands at a critical crossroads between resilient corporate fundamentals and macro-driven anxiety. While the high percentage of early beats suggests that American business remains surprisingly nimble, the coming days will determine if that momentum can withstand the Mag 7’s massive spending requirements. Investors must now weigh record-breaking double-digit growth against a higher-for-longer interest rate environment fueled by stubborn retail inflation and a wary consumer. Whether the upcoming deluge of results confirms a sustainable AI-driven rally or exposes a widening gap between tech giants and the broader economy, the next two weeks will undoubtedly set the definitive tone for the 2026 market narrative.

1 UnitedHealth Group Reports Q1 2026 Results, April 21, 2026, https://www.unitedhealthgroup.com

2 United Airlines Reports Q1 2026 Results, April 21, 2026, https://www.united.com

3 Southwest Airlines Reports Q1 2026 Results, April 22, 2026, https://www.southwestairlinesinvestorrelations.com

4 Boeing Reports Q1 2026 Results, April 22, 2026, https://s2.q4cdn.com/661678649/files/doc_financials/2026/q1/Press-Release.pdf

5 Tesla Reports Q1 2026 Results, April 22, 2026, https://assets-ir.tesla.com

6 IBM Reports Q1 2026 Results, April 22, 2026, https://www.ibm.com

7 Intel Reports Q1 2026 Results, April 23, 2026, https://d1io3yog0oux5.cloudfront.net

8 March Retail Sales, US Census Bureau, April 21, 2026, https://www.census.gov

9 University of Michigan April Consumer Sentiment, Surveys of Consumers, April 24, 2026, https://www.sca.isr.umich.edu/

10 FactSet Earnings Insight, John Butters, April 24, 2026, https://advantage.factset.com

11 Time Will Tell: Information in the Timing of Scheduled Earnings News, Journal of Financial and Quantitative Analysis, Eric C. So, Travis L. Johnson, Dec, 2018, https://papers.ssrn.com

Copyright © 2026 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon's prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. This publication shall not constitute an offer to sell or the solicitation of an offer to buy, nor may there be any sale of any securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Wall Street Horizon

Read more commentaries by Wall Street Horizon