Former Federal Open Market Committee Chairman Alan Greenspan famously observed that forecasting foreign exchange was like flipping a coin. Last year proved him right. What happened, and what lessons can it teach us about the dollar in 2026?

Like most forecasters, we came into 2025 believing that the economic impact of tariffs would support the US dollar. And yet, in the first few months of last year, the dollar slid by roughly 10%. Then, just when the market adjusted to the likelihood of further dollar weakness, the currency instead stabilized and even regained some ground.

One reason that predicting an exchange rate is complicated is that there are both structural and cyclical variables at play. Structural variables tend to play out over a very long time, while cyclical variables tend to work faster. We believe that there are good structural reasons for the dollar to weaken and that those variables were the primary reason the dollar slid in early 2025. But cyclical variables that pointed—and continue to point—in the other direction boosted the dollar as the year progressed.

We expect more of the same in 2026: a push and pull between the long term and the short term leaves us expecting more volatility than directionality. We expect the dollar will bounce around, but we don’t have high conviction that it will durably move in one direction or the other.

Crosscurrents Keeping the Dollar in Check

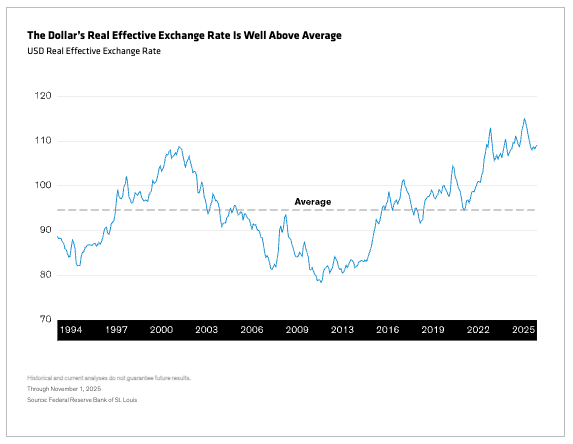

From a structural perspective, there are two primary factors that require consideration. The first is valuation. The dollar’s real effective exchange rate, which measures its purchasing power relative to other currencies, is well above its long-term average (Display). This rate tends to mean revert over long periods, suggesting that we should expect the dollar to weaken.

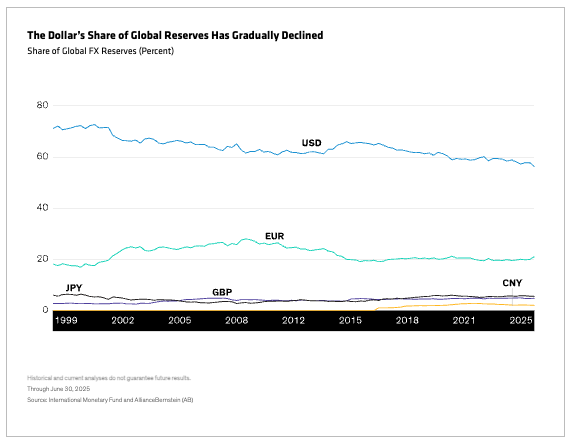

The second structural force—and the mechanism for valuation-driven weakening—is reserve diversification. Central banks and sovereign wealth funds around the world hold a disproportionate share of their assets—nearly 60%—in dollars (Display). That share has gradually declined over time.

Still, given the US’s less reliable, less predictable and less rules-based role in the global political economy, we believe that global reserve managers have an even stronger incentive than they had previously to diversify their holdings. Indeed, the data suggest that outflows accelerated somewhat last year in the wake of the magnitude and breadth of the tariffs announced in April.

Those same tariffs that gave our trading partners incentive to move out of dollars, however, also provided economic support for the currency as the year progressed. Tariffs did reduce the trade deficit by making foreign goods less competitive in the US market, and reducing a trade deficit generally supports a currency.

Tariffs made a fiscal impact too, generating record levels of customs revenue—more than $200 billion in 2025. While that represents only 0.5% to 1.0% of total GDP, it did make a contribution to the federal budget. And, while the deficit remains very large by historical standards, it does not appear to have increased in 2025. That, too, should be supportive of the dollar.

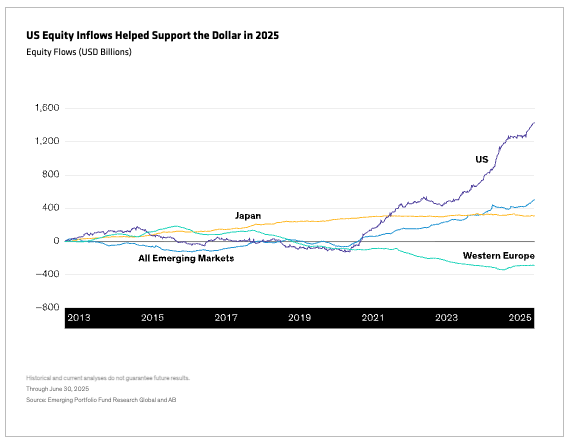

Finally, increasing investor attention to artificial intelligence (AI) also boosted the dollar as 2025 progressed. Inflows into US equity markets, which became increasingly concentrated in AI-related names, provided support for the currency as well (Display).

These factors fought to a draw in the second half of 2025; after its early slide, the dollar treaded water for the remainder of the year. And given that the same factors remain in play today, we expect more of the same in 2026.

Swing Factors That Could End the Stalemate

That outlook could change if certain swing factors materialize.

The first and most important potential shock to the system would be a loss of central-bank independence. Central banks without independence have a long and inglorious history of generating persistent inflation, which would erode the value of long-term dollar holdings and force reserve managers into other currencies.

If the Supreme Court decides pending cases in favor of the Trump Administration and the Fed becomes subject to political oversight, or if the next Fed Chair is not perceived to be independent, we believe that reserve managers will significantly accelerate their diversification away from the dollar.

On the other side of the coin, if AI boosts productivity in the near term, that could lead to an economic acceleration that would generate more inflows and push the dollar’s value back up. At this stage of the year, we can’t predict whether either of those possibilities will materialize, and thus we expect the dollar to fluctuate rather than to trend.

As ever, though, forecasting foreign exchange is a dangerous game, and we will watch closely as the year progresses to see which factors prevail or if the stalemate that defined the end of 2025 in currency markets persists through 2026.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein