Taiwan-based insurers are gearing up for a big overhaul in their regulatory framework. The transition to the Taiwan Insurance Capital Standard (TW-ICS) is slated for January 2026, though some provisions will have a lengthy phase-in period. Over time, the impact on capital-based relative value could lead some insurers to consider transforming their asset allocations.

The shift will happen along with the adoption of a new accounting regime, International Financial Reporting Standard 17 (IFRS 17). TW-ICS is intended to align Taiwan’s regulatory framework with international standards, including Solvency II in Europe as well as Japan and Korea, who have already implemented their version of the ICS. In doing so, the Financial Supervisory Commission hopes to bolster the strength of Taiwan’s insurance sector.

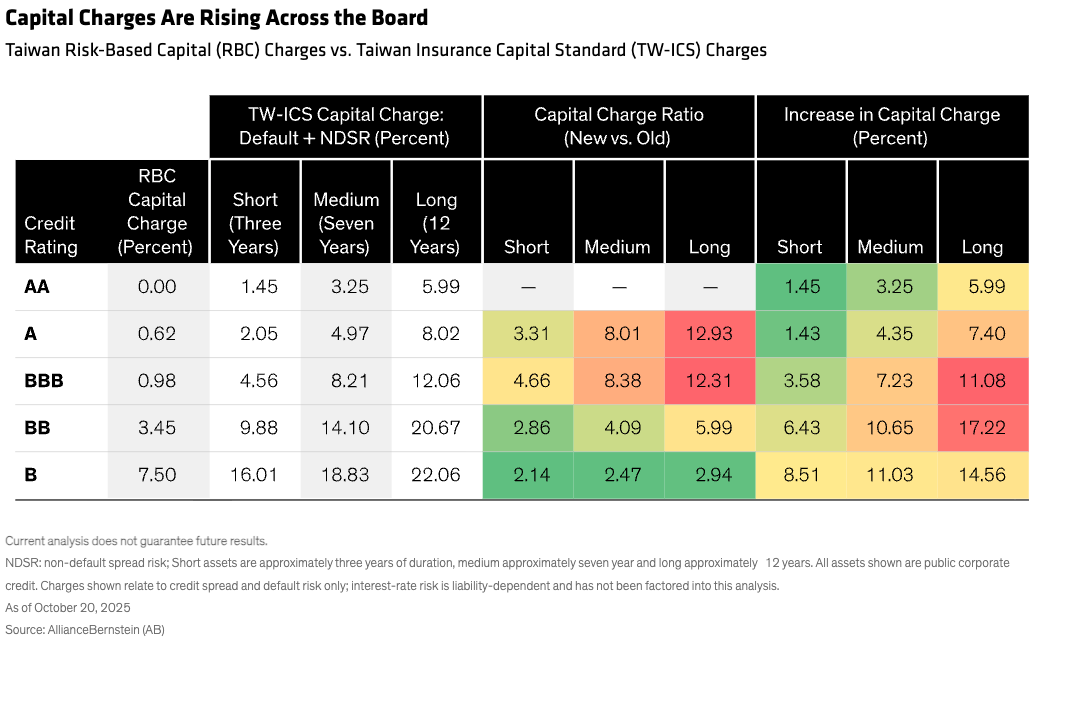

New Calculation for Risk-Based Capital Charges

Under TW-ICS, balance sheets will be treated on a fair-value basis, with both assets and liabilities marked to market where possible. The rules will also usher in a new, more complex, methodology for calculating required capital on different investments. The current calculation is based on rating alone; under TW-ICS, it will also account for the investment’s spread duration, or sensitivity to changes in spreads, and maturity.

For credit risk, there will no longer be a single credit-risk factor. The new rules call for insurers to provide separate factors for default risk and the risk from credit spreads widening in the absence of default, called non-default spread risk, or NDSR. The TW-ICS will sharply increase capital charges (Display), though the interest-rate and NDSR factors will phase in over 15 years to avoid cliff effects.

Assessing the Impact on a Relative Value “Heat Map”

With a few calculations and data points, we can translate the new capital charges into a revised relative value heat map. Default risk can be sourced from a regulatory table, and will vary based on factors including credit rating, type of asset and term to maturity. The NDSR for assets can be calculated with the following function:

Spread Duration x Min (Max (75% x Asset Spread, 40), 150)

There is a similar formula for calculating the NDSR on the liabilities in a spread-down stress; here, we focus solely on the impact to the asset side of the balance sheet.

Longer-duration assets will generally require more capital reserves because the spread-duration component is now considered part of the overall capital charge—unlike before. Naturally, lower-rated assets will face a higher incremental charge, but the relative impact is larger on higher-quality assets. For example, in the long-duration category in the previous display, B-rated bonds will face a charge 2.94 times higher; for A-rated bonds, the charge will be 12.93 times higher. This is partly explained by the effective cap of 150 basis points in spread stress applied to calculate the NDSR.

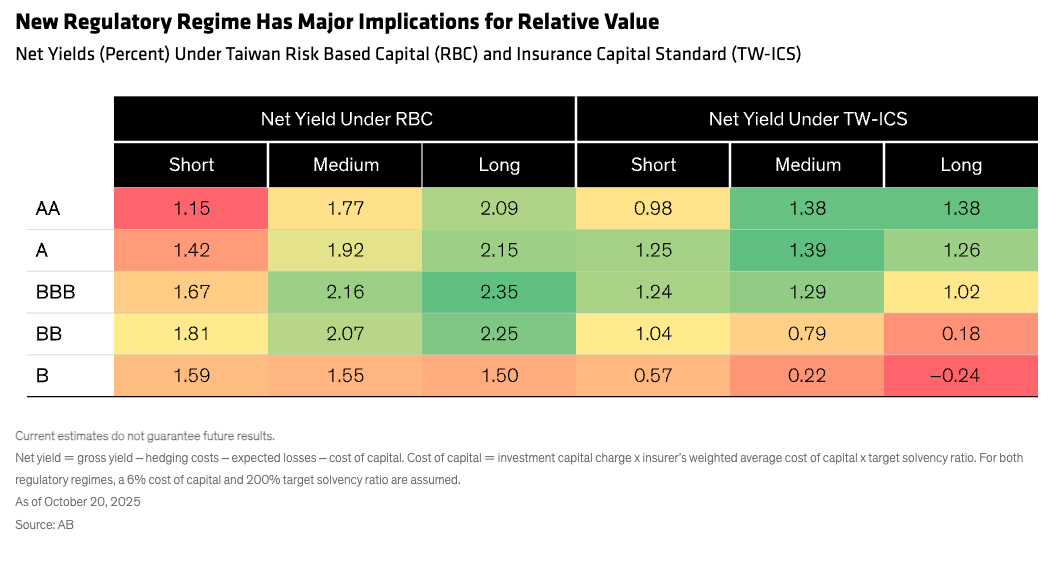

Collectively, these changes will reshape the relative value heat map, as can be seen by comparing net yields under the two regimes (Display).

What TW-ICS Could Mean for Insurance Portfolios

With the sizable boost in capital requirements, it would be only natural to expect Taiwanese insurers to bring down portfolio risk, looking to move up in quality to reduce the weight of capital charges. We can also see insurers shifting from the BBB/BB region to AA/A to take advantage of relative value, particularly at longer maturities. The path, however, may be different for well-capitalized firms or those with a lower cost of capital. Relative-value assessments at different durations should consider interest-rate sensitivity relative to the liability profile.

Under the new framework, foreign-exchange exposures will be more visible, a key development for Taiwan-dollar-based insurers who often invest in unhedged US dollar assets. We have seen issues arise this year as a result of US dollar/Taiwan dollar currency volatility; insurers might react by mitigating risk and matching foreign-exchange exposures between assets and liabilities more closely, especially where the balance sheet under new regulations is more sensitive to this volatility.

To shore up balance sheets in light of the more strenuous capital requirements, we could see insurers making more use of other capital-management activities, such as implementing hedging programs and boosting access to the debt market. We might also see more activities to optimize balance sheets, with a focus on raising equity: capital injections, joint ventures, reinsurance and sidecar deals to free up capital and surplus. Under ICS, asset-liability management will become even more integral to managing interest-rate risk, and investment strategies will need to evolve, growing more complex to adequately manage capital positions and overall balance sheets.

Because the new framework will be implemented gradually, firms will have time to access debt markets to raise required capital. We’ve seen increasing sophistication in Europe’s approach to asset-liability management, in large part due to regulatory changes introduced in 2016. This may flow through to Taiwan’s market, which could be informed by previous efforts made under Solvency II.

The bottom line for Taiwan’s insurers? ICS is coming in 2026, and even though some provisions will phase in over an extended period, the new rules will alter the relative value playing field and other fundamental aspects of portfolio construction.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein