FaST (Few Sentence Takeaway): There is (another) framework for a deal with China. That is a positive for risk markets. There is increasing evidence of waning tariff effects on company earnings and outlooks. That is a positive for risk markets. The interaction of the two is by far the most intriguing.

Let's begin with the tariffs. Tariffs get every headline, but their effects on revenues/earnings appear to be abating. Liberation Day was six months ago. Companies did not wait to "gather additional facts" about the trajectory of tariff policy. They began to mitigate the risk to their businesses and defend their margins. Earnings season is in full swing, but a couple of examples stand out.

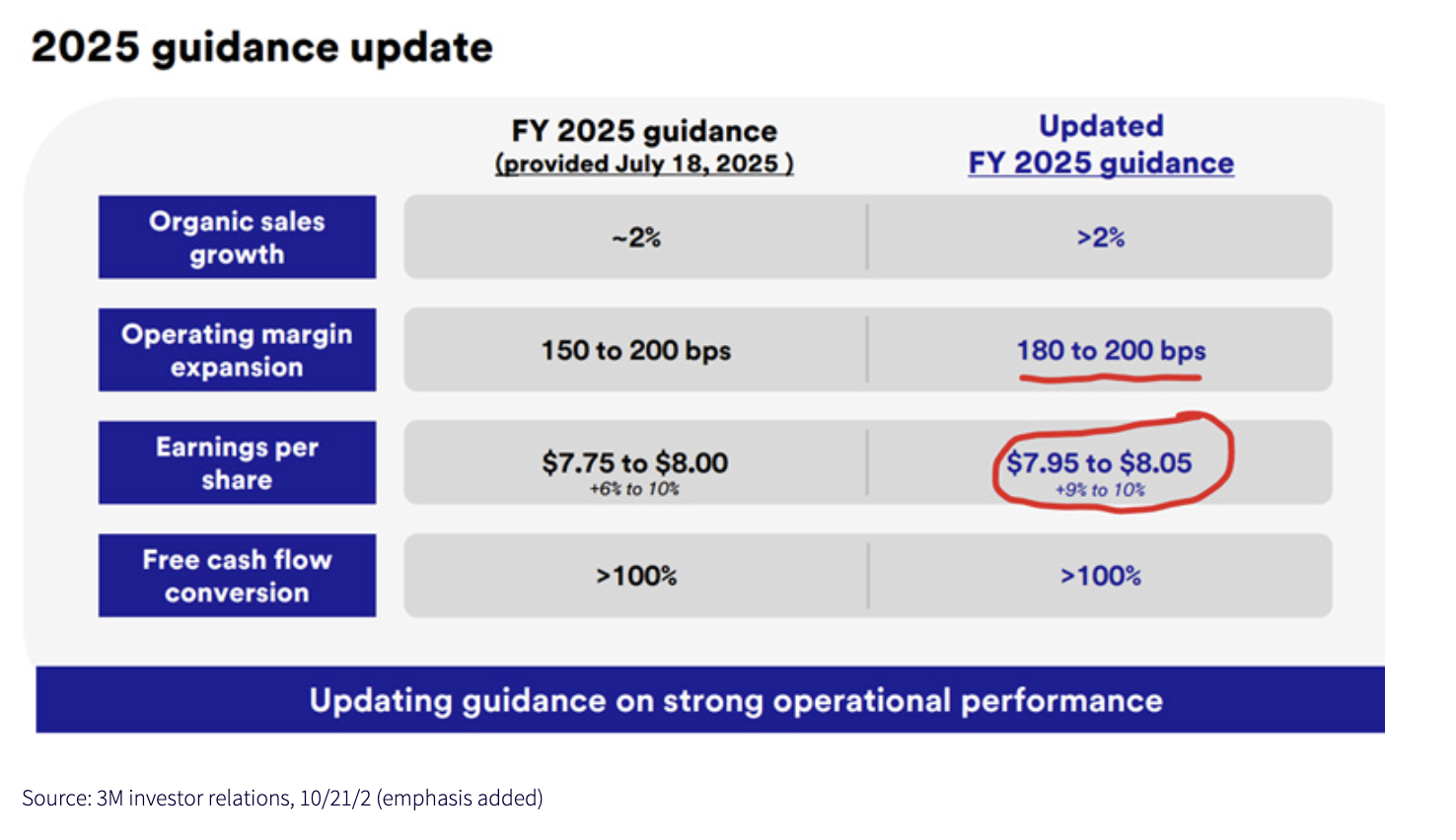

but then

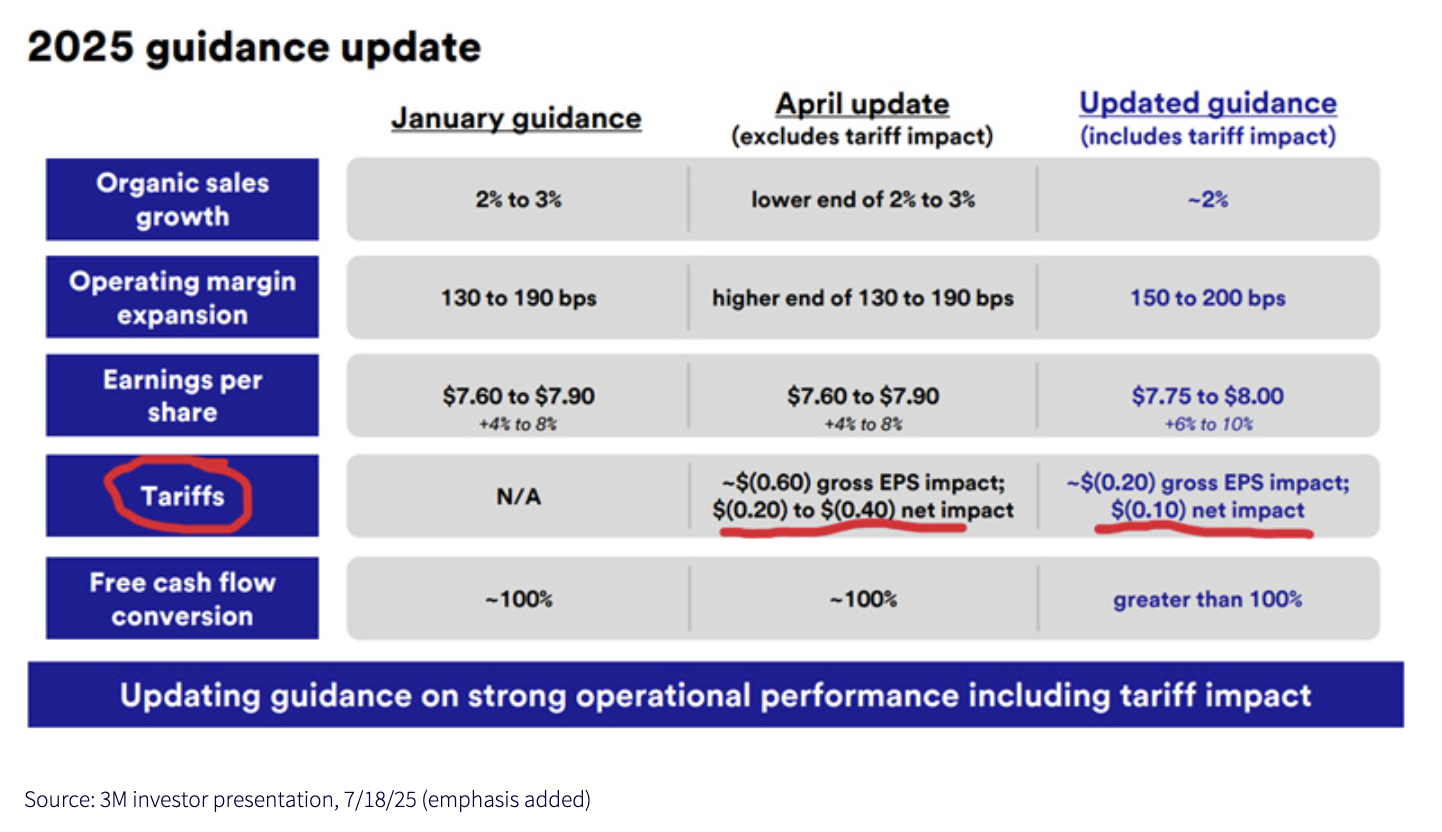

There is something conspicuous missing between the two slides. In the wake of Liberation Day, the tariff hit was set to be around 4% to 3M's bottom line. Fast forward a single quarter: 3M did not even include a line for the effect of tariffs and increased their guidance above the pre-tariff level. That is not a "one-off" example either.

Not everyone has ceased talking about tariffs. But tariffs are far from the dominant talking point in earnings releases. Simply put, there is far less sensitivity to tariffs in company reports than six months ago.

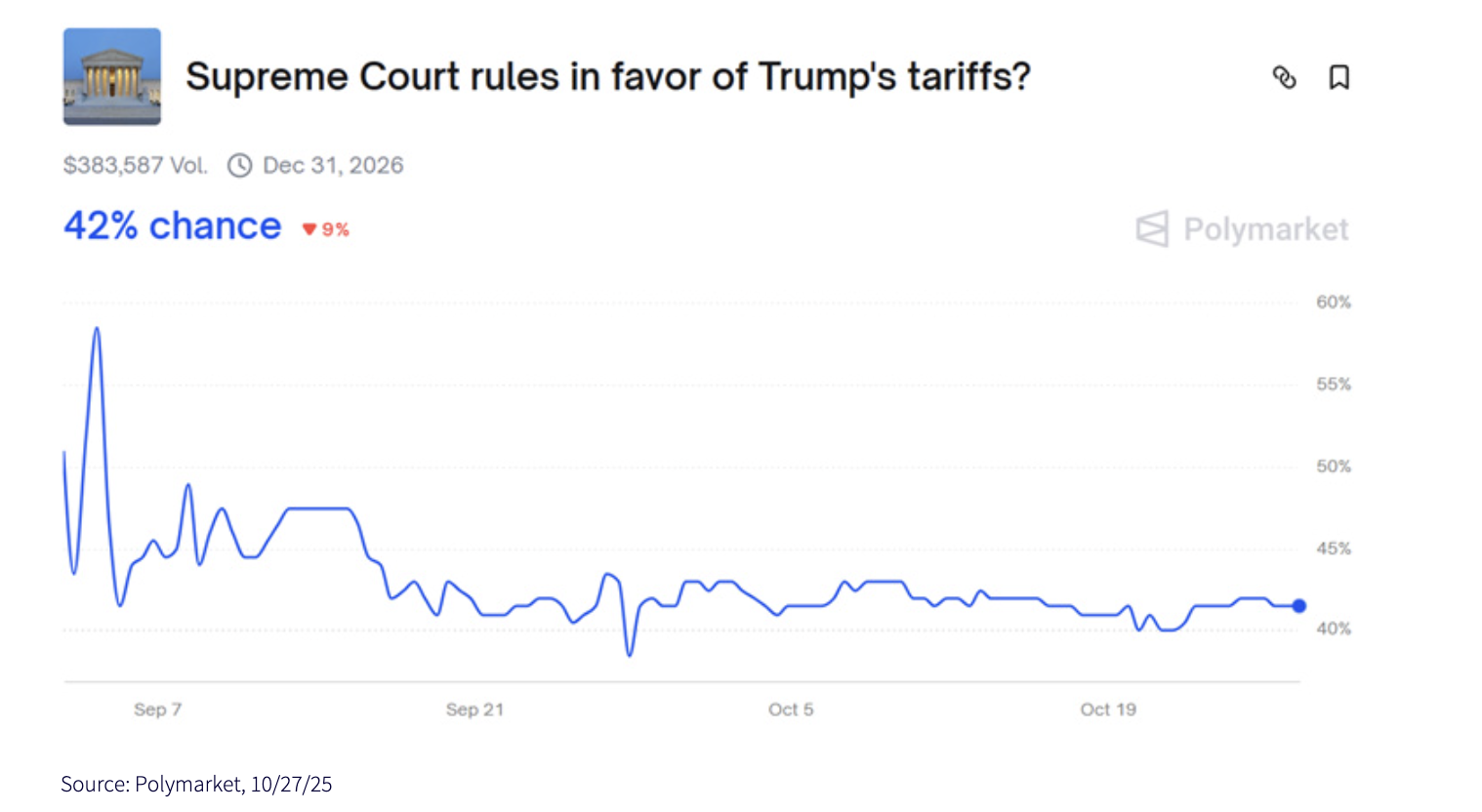

Not to mention, there is also an upcoming Supreme Court challenge (November 5) to the legality of the current IEEPA tariffs. This covers the vast majority of the tariffs currently in place. If ruled illegitimate, the tariffs will be rolled back. Also, the tariff revenue collected would be repaid. What are the odds of that happening?

Not trivial. In fact, slightly better than 50/50. That would be yet another catalyst for many of the 490.1 When you combine the mitigation of tariffs (see 3M above) with the potential for a corporate stimulus check tariff repayment, there are reasons to look at the 490 for opportunities. Of course, tariffs would come back (section 232 or 301, or both, are candidates). But they would already be mitigated.

When it comes to the U.S.-China trade framework, the meeting between Presidents Trump and Xi this past Thursday is going to be important to consider. A few bullets on pieces of the announcement that mattered more.

- Rhetoric on "No Tariffs for Minerals": (U.S. reduces tariffs/leaves at current levels, China keeps rare earths flowing)

- A "TikTok Dance": (A deal around TikTok likely includes some relaxing of U.S. semi restrictions, though not the highest-end chips)

- "Soybeans for Solace": (A deal for China to return to the U.S. soybean market into the U.S. midterms)

Importantly, the deals are likely structured to last through the midterms—alleviating pressures on some of the more sensitive economic areas of the U.S. economy. Any deal will be far from comprehensive, but it will eliminate a risk overhang to the U.S. economy/risk markets.

Risks are coming off the table and/or have already been dealt with by corporates. Maybe, just maybe, the 490 are about to strike back in a meaningful way.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Alejandro Saltiel, Andrew Okrongly, Behnood Noei, Bradley Krom, Brendan Loftus, Brian Manby, Christopher Gannatti, David Graichen, Hyun Ku Kang, Jeff Weniger, Jeremy Schwartz, Jonathan Steinberg, Joseph Grogan, Joseph Tenaglia, Kara Dombroski, Kevin Flanagan, Lauren Pfendt, Liqian Ren, Lonnie Jacobs, Matt Wagner, Rick Harper, Ryan Krystopowicz, and Vanya Sharma are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.