We live in what Brett Arends claimed as “The Dumbest Stock Market In History,” but I believe it is potentially the most dangerous era. That phrase is not hyperbole as it reflects structural distortion, extreme valuations, and an investor base intoxicated by momentum and narrative. The MarketWatch piece puts it bluntly: “At one level, there is no doubt that this is the dumbest market in history, because at this point it is completely dominated by ‘passive’ index investing.” That dominance means we are now in the most dangerous era where market mechanics, not fundamentals, rule.

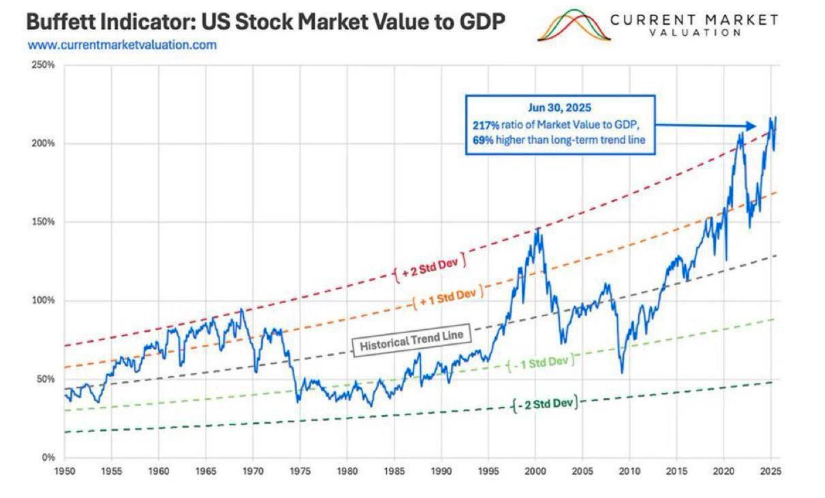

Consider the valuation extremes. The S&P 500 trades at 26 times trailing earnings, and the CAPE ratio hovers near 40x, levels seen only in the height of historic bubbles. The total stock market’s capitalization now exceeds 217% of U.S. GDP, a ratio Warren Buffett once identified as a warning flag. In the MarketWatch narrative: “The market, by this measure, is near the all-time peak reached during the epic bubble around the turn of the millennium.” Those numbers don’t lie.

But as we know, valuations mean very little in the short term during the fevered pitch of an investing mania. However, in the long term, valuations indicate future outcomes. Given the current levels, does it potentially make this era even more dangerous than 2000 or 2007? Maybe, yes. That is because the underlying structure has changed. We now have a market where capital flow is automated, valuation discipline is eroded, and active managers are fading. The passive tsunami has erased Ben Graham’s “margin of safety” while the narratives (AI, debasement, central banks as saviors, etc.) dominate. All that’s left is momentum and sentiment, and when momentum flourishes in a weakened system, it is a powder keg.

In the most dangerous era, crashes will not start with macro shocks but with structural unraveling.

The Impact of Passive Investing on Markets and Valuations

We have previously written about the issues with passive investing.

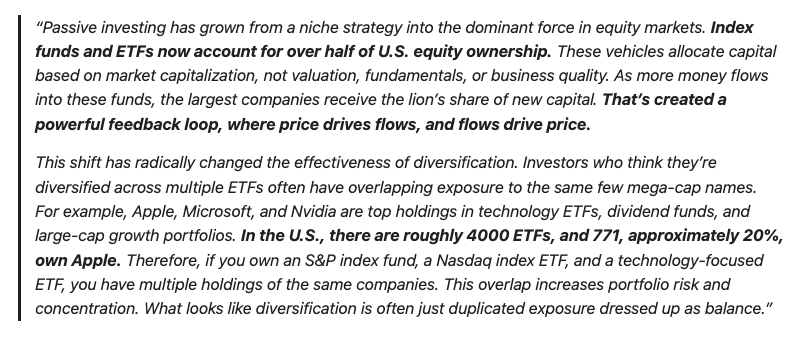

However, in a market dominated by passive funds, the other byproduct is the erosion of any valuation discipline, which is, in my opinion, one of the most central features of this most dangerous era. Passive strategies don’t pick winners; they replicate an index. As Morningstar recently articulated, “Passive investing is fueling the rise of mega‑rirms, which could affect your portfolio in unexpected ways.” Because of this structural shift, the most prominent firms receive outsized capital flow regardless of fundamentals.

One core mechanism is flow concentration. As assets flow into index funds, passive managers buy stocks in proportion to their weight in the index, which means mega‑cap names disproportionately benefit from inflows. Morningstar noted that passive investing fuels “distortions in price formation, market concentration, and volatility.” Academic research backs that phenomenon. In the paper Passive Investing and the Rise of Mega‑Firms by Jiang, Vayanos, and Zheng, the authors demonstrate that flows into passive funds “disproportionately raise the stock prices of the economy’s largest firms” and especially those “in high demand by noise traders.” The result is that the aggregate market might rise even if the flows come purely from reallocation from active to passive strategies.

Because passive flows inject capital mechanically, they increase idiosyncratic volatility in large firms. That increased volatility discourages arbitrage from active investors who might otherwise correct mispricings, allowing distortions to persist. The paper found that the largest firms in the S&P 500 experience the most significant returns, and volatility increases following passive inflows.

Morningstar’s warning is timely: the surge in passive investing “doesn’t just mirror the market — it shapes it.” What once was a price‑taking approach is now a price‑setting force. This also leads to several distortions that pose a significant risk to investors.

- The pollution of valuation signals. When mega firms get capital for size rather than merit, valuation ratios become less meaningful. A large and popular firm in the index keeps attracting capital, regardless of profit margins, growth prospects, or leverage. The feedback loop is self‑reinforcing: size begets inflows, which beget price increases and more size.

-

The casualty of liquidity. Passive dominance gives a veneer of liquidity, especially in bull regimes. But in stress, passive funds become sellers. Forced redemptions trigger mechanical selling of underlying equities. That selling pressure concentrates on the very names already inflated by passive flows. In the most dangerous era, structural fragility serves as an accelerant to corrections.

-

Concentration and herding risk. Many portfolios assume diversification simply by owning index funds. However, proper diversification vanishes when an index is heavily weighted in a few mega names. Morningstar’s analysis underscores that distortion. And the academics back it: the rise of mega‑firms driven by passive flows concentrates systemic risk in a few names.

In short, passive investing underwrites a market where the most prominent firms dominate by default, not by merit. That behavior undermines valuation integrity, amplifies volatility, and builds in fragility. In the most dangerous era, these distortions are not theoretical risks. They are the architecture underlying today’s market.

Speculative manias are not a modern invention. They recur with different assets, new technologies, and updated language. What remains constant is the core mechanism: the promise of easy wealth, mass participation, and innovation that seems too powerful to fail. Today’s environment mirrors the 1920s, not by coincidence, but by design. This is a feature of the most dangerous era, where Wall Street markets access as progress but often hides asymmetric risk.

In the 1920s, investment trusts were sold to everyday investors as a safe way to share in Wall Street’s boom. In truth, they were layered with leverage and internal cross-holdings that no one could untangle. When the market turned, they collapsed. The modern version is private equity funds inside 401(k) plans, crypto ETFs with built-in leverage, and semi-liquid vehicles promising stable returns from inherently illiquid assets. As the New York Times Magazine recently noted, these vehicles are pitched to ordinary investors as “opportunities once reserved for the elite.” Still, they obscure risk behind slick packaging and limited redemption rights.

Michael Saylor’s Strategy (formerly MicroStrategy) became a Bitcoin proxy through billions of debt-financed crypto purchases. Robinhood now sells “private company tokens” tied to firms like SpaceX and OpenAI, products that mimic equity without the regulatory safeguards. In both cases, retail investors are invited to invest in high-risk, thinly regulated assets with little transparency. The logic echoes 1929: financial instruments are being repurposed to offer the appearance of access and stability, while concealing leverage and fragility.

What makes this dangerous is the illusion of liquidity and price stability. Private equity firms now mark assets with little market validation, known informally as “mark-to-make-believe.” Redemption limits, like the 5 percent cap in funds such as Blackstone’s BREIT, prevent investors from exiting but do little to prevent panic. When prices stop rising, the promise of access becomes a trap. In the most dangerous era, history isn’t rhyming, it’s repeating with new wrappers and fewer brakes.

What This Means for You, the Irony of the Crowd, and Final Thoughts

If you accept that we are in the most dangerous era, your approach must shift. The market no longer rewards bullish optimism. It punishes complacency.

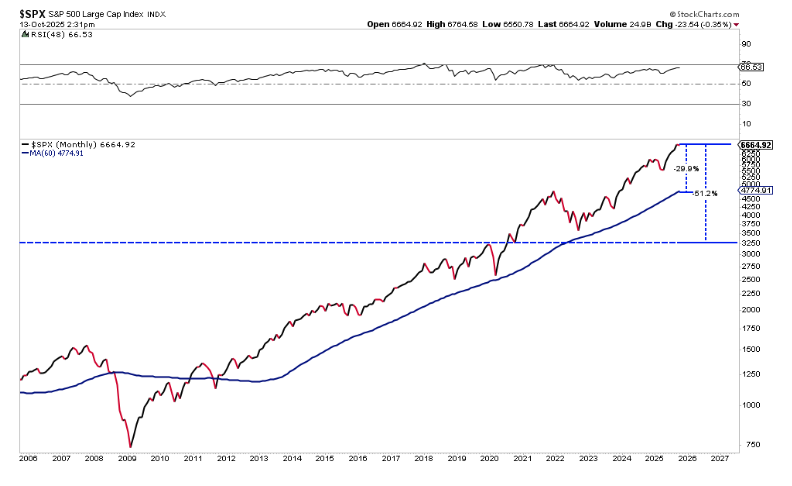

Begin with risk. While it may seem like it can’t happen, assume a 30% to 50% drawdown. In the S&P 500, a 30% retracement would only reset the market to the current bullish trend line from 2009. A 50% retracement would only reset markets to the beginning of 2020.

In Gold, a 30 to 50% correction would be well within historical norms of corrections that followed more extreme overbought conditions driven by speculative fervor.

While I am not suggesting that such corrections WILL occur, I am suggesting that stress testing your portfolio is crucial. Can your allocation survive that? Or rather, could you emotionally survive such a decline? Do you know which positions will lead during a crash, versus which will lag?

Critically, you must resist the crowd. Passive investing was sold as democratization, but it has become the crowd. As MarketWatch notes: “Indexers buy stocks without any regard to valuation … index funds chase the crowd … index funds are the crowd.” When you and everyone else hold the same names, fragility amplifies.

Furthermore, hold liquidity. Cash isn’t dead money; if we are in the most dangerous era, it is insurance and gives you optionality. Cash lets you act when others panic, a flexibility you will want when forced selling begins.

Also, favor active and disciplined strategies. Value investing, risk control, and a margin of safety will matter again when volatility returns. When the crowd abandons fundamentals, fundamentals regain power, and valuations matter even more when the “market fantasy” eventually revisits reality.

Finally, stay sober on narratives. AI, biotech, space, these are compelling stories, but when they drive valuation without cash flow, they become speculative traps. Markets don’t reward stories forever; eventually, the demand for profitability will matter.

The irony of the crowd is brutal: we designed passive strategies to remove emotion. Instead, we institutionalized herd behavior. Now the passive masses amplify bubbles instead of dampening them. That is the truth of the most dangerous era.

This moment is historic, not just for its heights but also for its fragility. The longer it lasts, the harder the unwinding. However, a crisis creates opportunities for disciplined, skeptical, and prepared investors. If you refuse to follow the crowd, you may live to profit from the dislocation.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice