Q3 2025 Earnings Preview: Earnings Season Begins with High Hopes and Key Tests for Banks

Key Takeaways:

-

Earnings season gets underway this week, with reports from major banks providing the first look at corporate performance

-

The technology sector is expected to be the standout performer with over 20% projected earnings growth, driven by the ongoing "AI arms race"

-

Sectors that rely on lower-end consumer spending are expected to see earnings decline as shoppers become more "value-conscious

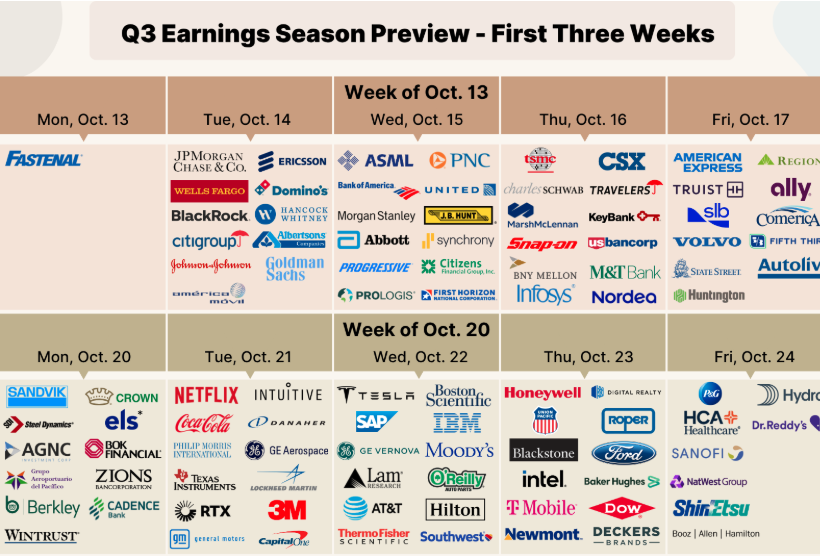

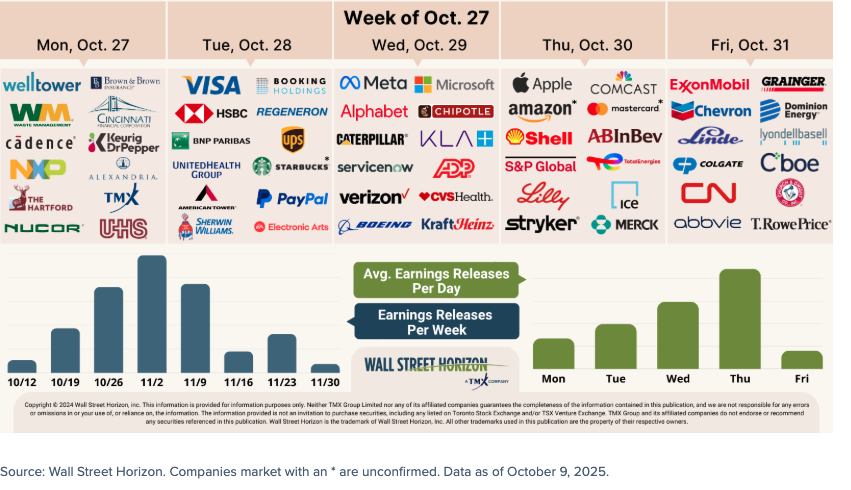

Earnings season kicks into high gear this week, with the big banks unofficially firing the starting gun on Tuesday. As the season begins, major U.S. indices are at record levels, even amidst a government shutdown, creating a dynamic environment with no shortage of significant events.

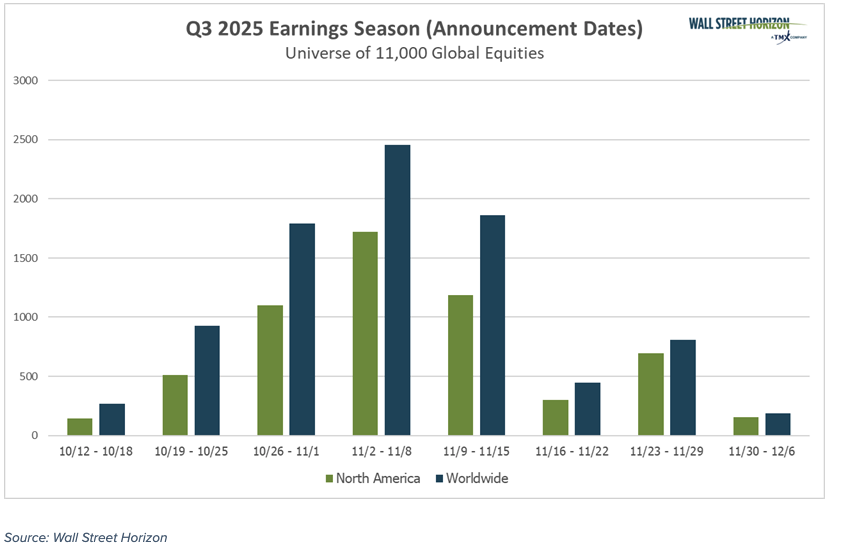

Sell-side analysts and investors alike are optimistic heading into the reports. For the first time since late 2021, Wall Street analysts have actually raised their earnings estimates heading into the reporting period, a rare vote of confidence in corporate America. The consensus is for an impressive 8% year-over-year earnings growth for the S&P 500®, a figure that would mark the ninth straight quarter of expansion. Revenue growth is expected at 6.3%.1

But don't let the headline number fool you. Under the surface, a "have and have-not" economy is becoming more entrenched. While the AI darlings and financial giants are poised for a strong showing, other sectors are starting to feel the pinch of a more discerning consumer and persistent inflation.

Key Themes for Q3 2025 Earnings Season

Big Banks Poised for Another Strong Showing

Financials are expected to be one of the leading sectors this season, as the environment for banks has gotten better, but there are still headwinds. JPMorgan Chase, Citigroup and Wells Fargo get the party started on Tuesday and here’s what we’re looking for updates in three key areas:

1. Dealmaking - both M&A and IPO markets have cautiously been thawing in 2025.

-

-

M&A Reawakens: While deal volume remains below historical highs, the value of transactions surged in Q3. According to our data at Wall Street Horizon, Q3 saw 111 M&A announcements. This is in-line with the first two quarters of the year, and a marked improvement from the M&A dearth of 2023, but still well-below the record quarters seen in 2022. The value of those deals on the other-hand neared a Q3 record. Dealogic data shows global M&A volumes hit $1.26 trillion, up 40% year-over-year, making it the second-best third quarter on record by value.2 Companies are hunting for scale, and a record number of mega-deals (over $10 billion) have been announced this year.

-

The IPO Window Creaks Open: The market for initial public offerings is no longer frozen shut. Blockbuster IPOs in the tech and fintech sectors, such as those for CoreWeave and Circle Internet, have demonstrated strong investor appetite. According to our data, there were 150 IPO announcements in Q3, the best quarter since Q4 2021. Expect banks to highlight this renewed momentum, signaling a healthier outlook for capital markets.

-

2. Lending - the tailwind from high interest rates which has boosted profits for the last couple of years is starting to show its downside.

-

-

Net Interest Income (NII) Under Pressure: NII—the difference between what banks earn on loans and pay on deposits—is expected to see modest growth or even begin to flatten. While the Federal Reserve's rate cut in September offered some relief, banks are now facing intense competition for deposits. Customers are moving their cash to higher-yielding accounts, forcing banks to pay more for funding.

-

Loan Growth: Demand for new loans has been sluggish for a while now as high borrowing costs have deterred both consumers and businesses. However, banks started to signal some optimism in this area as loan growth was better-than-expected in Q2.3 Listen for commentary from Bank of America and Wells Fargo on mortgage and auto loan demand, which are key indicators of consumer health.

- Credit Quality in Focus: While credit remains generally stable, any uptick in delinquencies or provisions for credit losses will be heavily scrutinized. The focus will be on commercial real estate, as well as potential stress among lower-to-middle income consumer borrowers.

-

3. Trading - Likely a bright spot once again this quarter due to volatility. Market volatility, driven by shifting expectations around Fed policy, inflation, and geopolitical uncertainty, creates opportunities for Wall Street trading desks.

-

-

Fixed Income, Currencies, and Commodities (FICC): Uncertainty around the future path of interest rates and asynchronous monetary policy from global central banks likely drove significant client activity in interest rate and currency products. This is a core strength for firms like JPMorgan and Citigroup.

-

Equities: Equity markets were resilient in Q3, with strong ETF inflows and a renewed "buy the dip" mentality from investors. The anticipation and eventual arrival of the September Fed rate cut sparked a rally in small-cap stocks, driving volume and creating profitable conditions for equities trading divisions.

-