Markets: Bullish vs Bearish Case

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsJust recently, Scott Rubner of Citadel Securities wrote an excellent piece discussing the bull versus the bear case for the markets. You look at the markets today and see a tension between expectation and reality. On one hand, equities—especially tech and growth—are pushing to fresh highs. Optimism about rate cuts, AI and productivity gains, global monetary easing, and solid corporate earnings has created a tailwind. On the other hand, concerns are growing: valuations are high, inflation remains only partly subdued, growth outside a few sectors is slowing, and investor positioning is nearing extremes. The debate is no longer academic. It’s central to how you allocate capital from here.

To understand where the market might go, you need to weigh both the bull case and bear case in light of what is actually priced and what risks remain unacknowledged. As noted, Scott argues that systematic flows and positioning may be nearer tipping points than many think. The data support the bull momentum case, but many components are already baked into current prices.

Some numbers to anchor where we are:

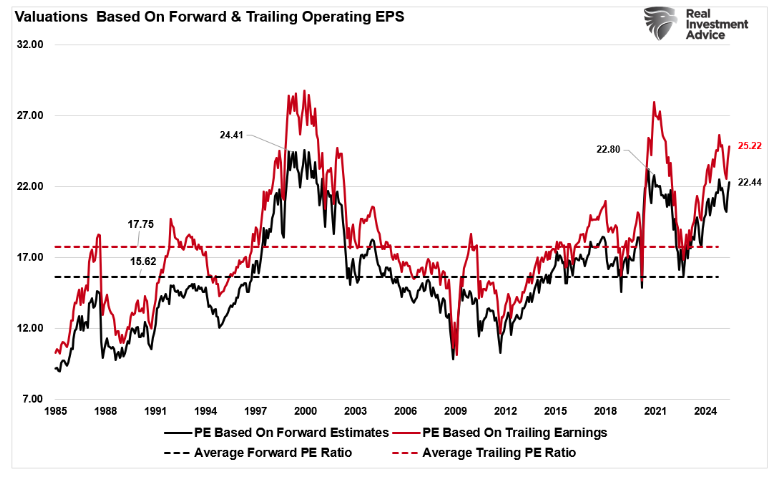

- The forward P/E of the S&P 500 is around 22‑23x. That’s near the top percentile from a long‑term historical view. UBS observes it’s among the top 5% readings since 1985.

- PMI (purchasing managers index) data still shows growth, especially in the manufacturing and tech sectors. However, there are signs of softness creeping into services.

- Earnings reports remain strong in major large caps (especially tech and AI‑exposed firms), but mid‑ and small‑caps have underperformed, with many earnings estimates getting revised downward.

So here’s the general overview:

- The bull case leans heavily on rate cuts, earnings growth (especially in AI/tech), global liquidity, and strong flow dynamics. If those hold or improve, there is room for upside.

- The bear case leans on overvaluation, deteriorating breadth (many stocks not keeping up), rising risks of macro softness (inflation rebounds, weak labor, global shocks), and the possibility that momentum—especially flow‐driven momentum—reverses sharply.

This moment is critical because many bullish assumptions are already reflected in current prices. That means the margin for error is shrinking, and any misstep, such as an inflation tick‐up, Fed caution, or earnings disappointments, could tip the balance toward a decline.

The Bull Case: Why Optimism Has Real Force

If you believe the market’s upside remains, here are the arguments that give weight to that side.

One of the strongest pillars for the bull case is the expectation that the Federal Reserve will continue to cut rates in the coming months. The Fed’s recent statements and market moves suggest the Fed sees enough slack or risk in the economy to consider easing further. Lower rates reduce discount rates for future earnings, helping to justify currently elevated valuations. They also allow firms with leverage or capital spending needs to borrow more cheaply. Lower rates help encourage activity for consumers and housing. If the Fed transitions smoothly without triggering inflation flare‑ups or financial instability, that opens a favorable window for equities.

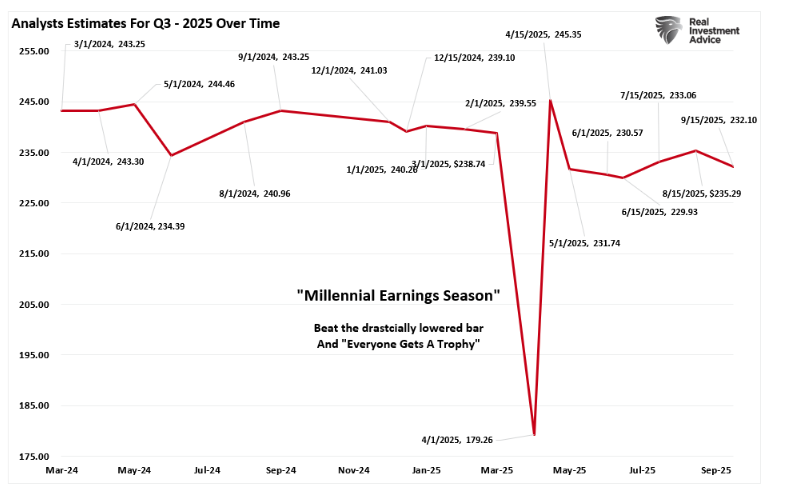

Secondly, you don’t get a market rally without earnings, even if investors want to believe momentum can carry it. So far, large‑cap tech and AI‑adopters are showing strong revenue growth, margin expansion, and forward guidance that suggests continued investment demand. Oracle’s recent surge, powered by AI contracts, is one example. For investors, third-quarter earnings estimates have been lowered, and with “Millennial Earnings Season” starting in October, we should see a decently high beat rate and optimistic forward guidance. Those reports should help put a floor under markets and ease current valuation concerns, particularly in the AI and technology sectors.

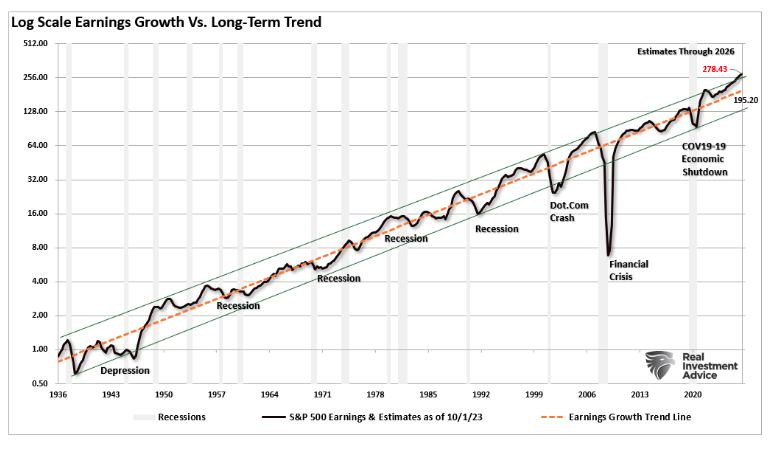

However, earnings optimism into 2026 is extremely exuberant currently, and we should expect to see these estimates come down over the next few quarters. The current deviation from the long-term earnings growth trend is now the largest on record.

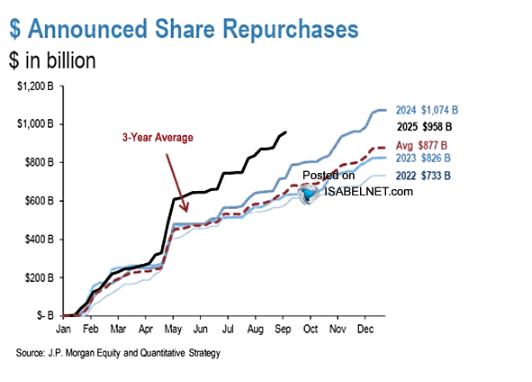

Third, corporate share buybacks return in the latter part of October as earnings season begins to conclude. Since the turn of the century, corporate share buybacks have accounted for nearly 100% of all net equity purchases. In other words, if it weren’t for share buybacks, the market would trade about 40% lower than it currently is. With share buybacks expected to exceed $1 trillion in 2025, and currently running at a record pace, the bullish case for the markets remains strong.

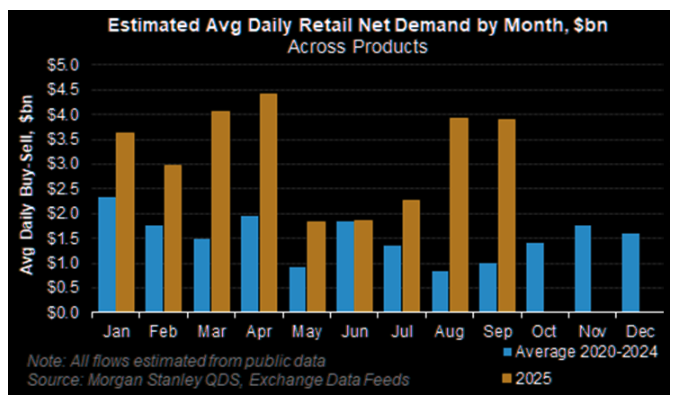

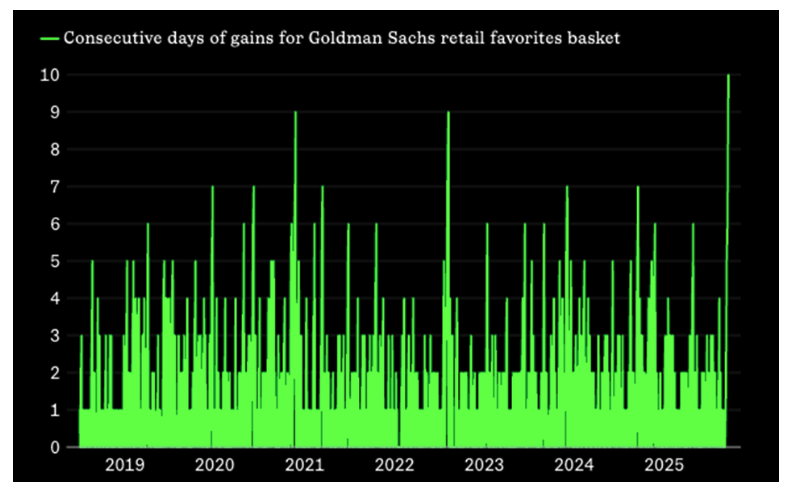

Finally, retail investors are flooding the markets. Flows into technology and growth sectors remain large, with money chasing the strongest performers. ETF and mutual fund flows show capital chasing technology, AI, and innovation‑oriented sectors, and retail participation, according to Morgan Stanley has run at a record pace in 2025 versus the average monthly rate over the previous five years.

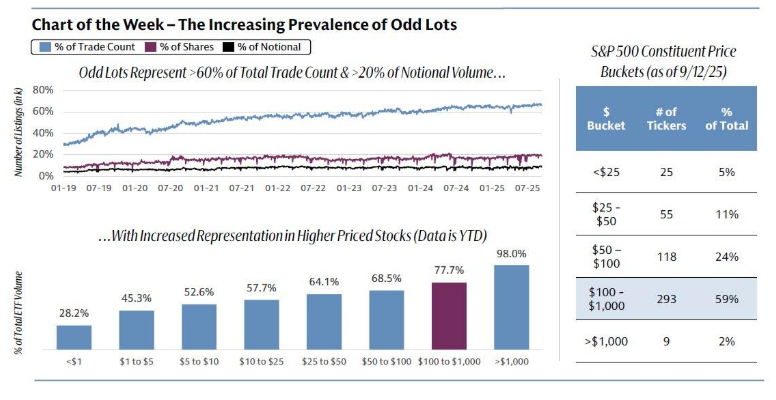

However, that data is confirmed by Goldman Sachs, which showed that odd lot transactions, or transactions with fewer than 100 shares of stock and a proxy for retail trading, just hit 66% of all US equity trades in Q3. That is up from only 31% in January 2019, representing more than 20% of notional volume and 8% of total executed shares!

Technically, the picture supports bulls enough to prevent retreat soon. Yes, broad market indices are above key moving averages, but market momentum remains positive. There are glimpses of improved breadth; some smaller and mid‑cap stocks are participating, particularly with the Fed now easing. While surveys also show fund managers believe stocks are overvalued, many remain overweight equities, which suggests they expect macro or earnings tailwinds to offset valuation risk.

The Bullish Scenario

Putting those together, what could a complete bull scenario look like?

- The Fed executes 2‑3 rate cuts in late 2025 / early 2026.

- Inflation continues toward targets, perhaps sticky in service sectors but less so in goods, energy, and commodities; productivity gains from AI help offset cost pressures.

- Global trade frictions ease or stabilize. No fresh shocks from tariffs, energy, or geopolitical risk.

- Earnings across sectors rebound or at least stabilize outside tech. Mid‑caps catch up. Consumer demand holds up better than feared.

- Liquidity stays abundant; economic growth remains positive, albeit modest.

If this happens, it is not unreasonable to expect that the S&P 500 could reach or surpass 7,000 by year‑end 2025 as the start of the seasonally strong period of the year begins.

That’s the bullish scenario, but it is not guaranteed. It does mean that the risk is balanced and potentially skewed slightly to the upside unless an unforeseen event derails the momentum.

The Bear Case: Risks That Could Undo the Bullish Drift

While the bull case has strong underpinnings, several threats could unravel it. If these materialize, losses could be steep and swift, and therefore, even if you are uber bullish, it could be worth considering.

First, as noted, valuations are already elevated. Forward P/E for the S&P 500 sits at 22.5x earnings with trailing earnings at 25x. UBS notes that such readings are among the top 5% since 1985.

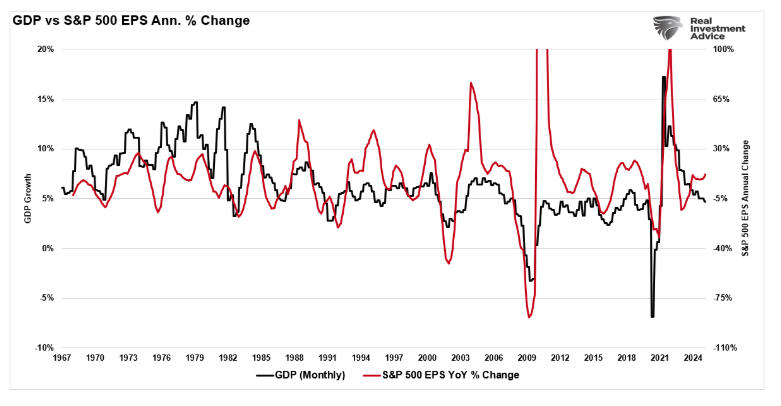

High valuations mean expectations are high and reflect investor sentiment. However, if earnings disappoint, then forward valuations (expectations) must be recalculated, and currently, the margin for error is slim at best. Notably, given that earnings are derived from actual economic activity, the current gap between the annual change in earnings and GDP is notable. The long historical correlation between the two suggests that a higher degree of risk to investors may be present more than realized.

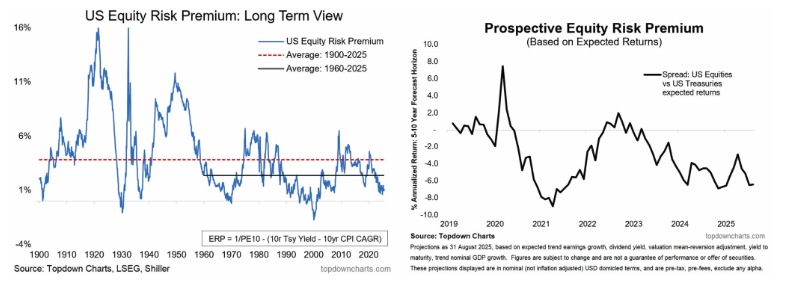

Also, the equity risk premium is compressed: the extra yield investors demand for owning stocks over “safe” assets is thin. Bonds and risk‐free rates are relatively more attractive than in some past cycles. As noted by Callum Thomas recently:

“The prospective equity risk premium (based on expected returns) is negative, and the ERP indicator from the Shiller data continues to track around 20-year lows. All the warning signs are there, and we need to be paying closer attention to opportunities in bonds and risks in stocks, with the next logical step for asset allocators being a switch to underweight stocks and overweight bonds.“

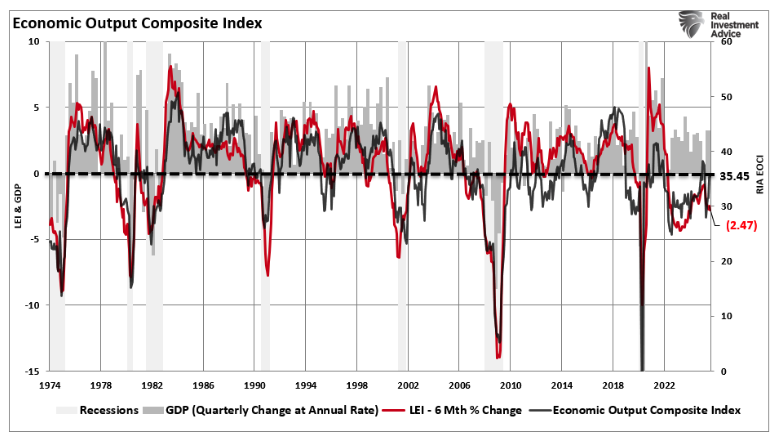

Growth is uneven. While the economic composite index upticked over the last three months, following the front-running of tariffs, the data remains broadly weak. Furthermore, consumer confidence is mixed; discretionary spending is under pressure from inflation, stagnant real wages, and rising debt burdens, suggesting that the most important driver of the markets, earnings, could be at risk.

Furthermore, earnings for mid‑cap and small‑cap firms have already shown cracks, as these firms are more sensitive to tighter financial conditions, supply chain disruptions, and weaker demand. A scenario where only a narrow set of large tech winners carry the market remains a risk, and creates a vulnerability to sector rotations and valuations contracting.

Lastly, external macro risks remain from trade policy, geopolitical flare-ups, fiscal policy uncertainty, global supply chain disruptions, and possible disruptions from China or other major economies. These are harder to forecast but matter and often trigger market corrections or risk‐off rotations.

Since investors have piled into equity markets, with flow data showing significant new money in tech and growth, sentiment and momentum indicators are extended. Put/Call and volatility measures show complacency, and systematic flows (ETFs, quant, passive) exacerbate drawdowns when they reverse. Scott Rubner’s Citadel commentary suggests that hedges are becoming more prudent.

If flows reverse or liquidity (monetary or fiscal) dries up, the downside risks grow nonlinearly. Margin debt, leverage, and crowded trades make the market more fragile.

Potential Triggers

What could trip the market into a more bearish path?

- Inflation unexpectedly rises again.

- Fed becomes more conservative or signals rate cuts later than expected.

- Earnings disappoint, especially outside tech. Revenue misses or margins shrink.

- Global disruptions, energy shocks, trade wars, supply chain failures, geopolitical conflict.

- Sentiment breaks, which could be due to one or more of the above, or just a shift in perception, leading to rapid outflows.

If any of those triggers occur, richly priced markets are vulnerable. The bear case is not necessarily a dramatic crash but a correction, a loss of multiple percentage points, possibly more if multiple risks coincide.

Conclusion: Tactics for Navigating Regardless of Outcome

Given both the strength of the bull case and the real risks in the bear case, your strategy must accommodate both. You should plan for multiple scenarios, hedge where appropriate, and avoid over‑commitment to one narrative. Below are actionable tactics to navigate what comes next.

- Maintain Portfolio Flexibility: Do not fully lean in or wholly lean out. Keep some dry powder (cash or cash equivalents) to take advantage of dips.

- Focus on Quality and Balance Exposure. Favor companies with strong balance sheets, pricing power, and secular tailwinds (e.g., AI, hardware infrastructure, industrials with tech adoption). Avoid overpaying for growth where earnings are speculative or cash flows are distant. Reduce exposure in crowded trades that are dependent on multiple assumptions.

- Monitor Macro Data Closely: Watch inflation components closely (wages, services, energy). Watch the Fed’s communication for signals of delay or caution. Monitor PMI readings, consumer sentiment, and credit spreads. Weakening in these may indicate that the bear case is gaining strength. Also monitor global data and geoeconomic risk.

- Manage Risk with Hedging and Position Size. Use hedges, such as options, inverse ETFs, or long volatility, to guard against outsized losses in case of negative surprises. Keep positions in speculative or high‑valuation names reasonably sized.

- Do not let winners become too large without reassessing fundamentals and risk. Rebalancing portfolios regularly can prevent concentration risks.

- Rotate allocations as needed: If rate cuts continue, cyclical sectors (industrials, financials, materials) could rise. However, defensive sectors (utilities, consumer staples, healthcare) may outperform if inflation or Fed risk prevails.

- Keep Expectations in Check. If the bull case plays out, returns from here may not be as spectacular as prior years. With valuations already high, gains may be more modest and volatile. If the bear case wins, drawdowns may be sharp. Planning your return expectations conservatively helps you avoid emotional mistakes.

- Use Volatility as an Ally: Volatility is not just risk but opportunity. When fear spikes, there are mispricings. When euphoria dominates, risk becomes underestimated. Rebalance in those moments.

In short, the market sits at a crossroads. The bulls have compelling arguments from rate cuts, AI tailwinds, and liquidity, but many are already reflected in current prices. The bears have significant threats, including overvaluation, inflation risk, and growth slips, but many only trigger under adverse surprises. Your task is not to pick who “wins,” but to position so your assets survive (and ideally prosper) whatever comes.

Discipline, balance, and alertness matter now more than conviction alone.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All