Key Takeaways

- Treasury yields fell sharply following a softer August jobs report, with the U.S. 2-year treasury now fully pricing in three Fed rate cuts.

- While the Fed is likely to cut rates in September, the decision-making process going forward is still highly data-dependent.

- With the UST 10-year yield near 4%, a sustained rally toward 2024’s lows appears unlikely unless recession risks escalate further.

It’s no understatement to say this could have been the most anticipated jobs report in quite some time. While it was not necessarily a referendum on whether the Fed would cut rates in a week or so, it was being viewed as perhaps the final input for Powell & Co. The overall report did confirm labor market activity is cooling, but it also seemed to confirm NY Fed Prez Williams’ description of a “no hire, no fire” jobs setting.

In terms of the upcoming Federal Open Market Committee (FOMC) meeting, in my opinion, the tenor of the August employment report confirms a 25-basis-point (bp) rate cut at the September FOMC meeting. Is a 50-bp rate cut completely ruled out? Not necessarily, but Powell & Co. have given no guidance on that front up to now. In fact, a negative payroll print would have made for a better argument for a 50-bp point cut. As for the remainder of 2025, an additional rate cut, or maybe two, is certainly now on the table, but once again, the Fed’s decision-making process will remain data-dependent with policy tilted more toward the employment aspect of its dual mandate.

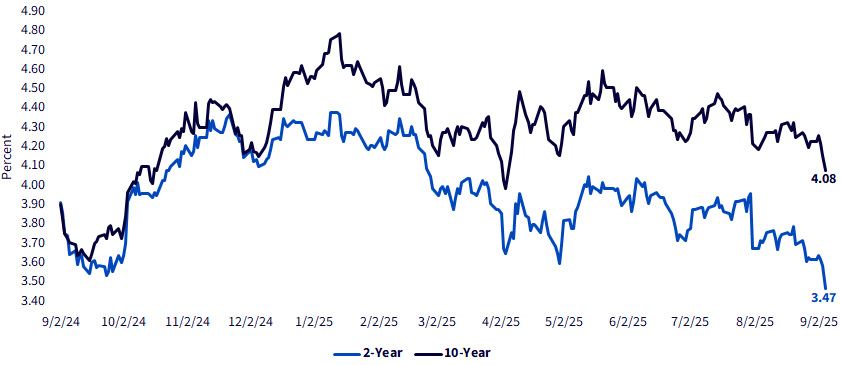

Figure 1: U.S. Treasury Yields

Source: Bloomberg, as of 9/5/25.

So, where can Treasury (UST) yields go in this environment? Treasuries rallied going into the jobs report, and the data provided the platform for this rally to continue post-release. As a result, the UST 10-yr yield fell to 4.08% while the 2-yr rate came in under the 3.50% threshold, as of this writing.

At these levels, the UST 2-yr yield is fully priced for three rate cuts and actually fell below the low watermark of 3.54% that was registered following the Fed’s 50-bp rate cut at the September 2024 FOMC meeting. However, the 10-yr yield has not experienced the same type of déjà vu. Indeed, at this time last year, the UST 10-yr yield fell to almost 3.60%, based on the increasing recession odds at that time. We’re not there at this point in terms of recession expectations.

That is an important consideration when trying to determine the upcoming movement in the 10-year yield. While rallies and sell-offs can overshoot in either direction, unless upcoming economic data shifts the outlook for a potential recession, it would appear as if the UST 10-yr rally could run out of gas. In other words, getting back to the 3.60% level would more than likely not occur.

Bottom Line

The key takeaway going forward is that Treasury yields don’t necessarily move in the same direction or with the same magnitude. With the UST 10-yr yield flirting with the 4% threshold, there is little margin for error if the economy can avoid an outright downturn.

A message from Advisor Perspectives and VettaFi: Are you backed by institutional quality bond funds? Click here to learn more.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.