Key Takeaways

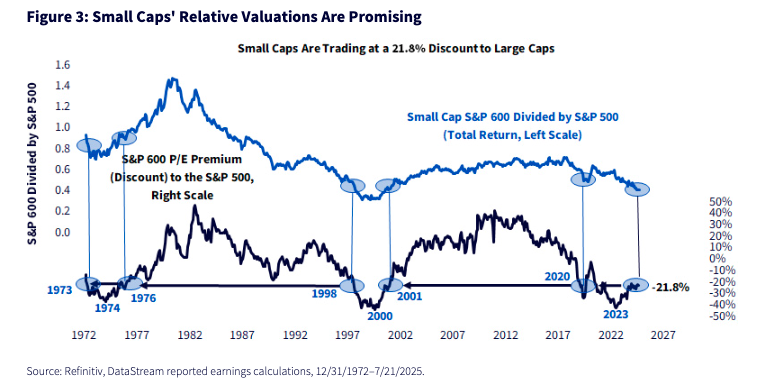

- Despite lagging the broader market, U.S. small caps now trade at a 21.8% valuation discount to large caps, levels last seen before major relative rallies in the 1970s and early 2000s.

- With rate cuts, Jay Powell could set up a reversal that swings fortunes in favor of small caps.

- Investors should consider focusing less on dollar predictions and more on small caps’ sensitivity to falling rates.

The house of pain continues with small caps, at least on a relative basis. Year-to-date, the S&P 600 index has posted a 3.0% gain, so it's not like money is being burned. But still, even the Bloomberg Aggregate Bond index is up 4.9% YTD and the S&P 500 is up 10.9%.1

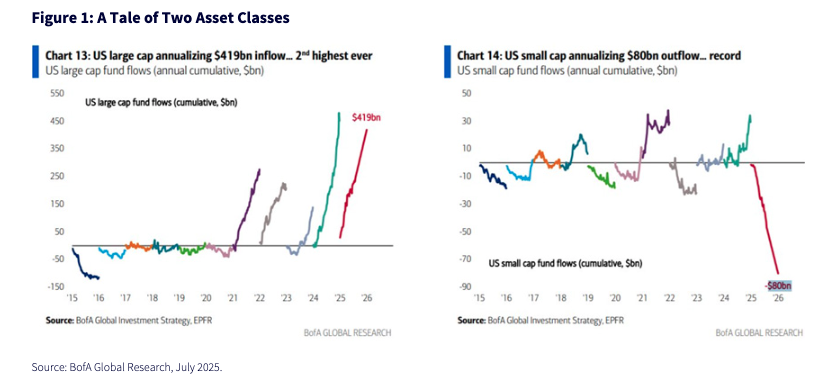

BofA's fund flow data tells a thousand words.

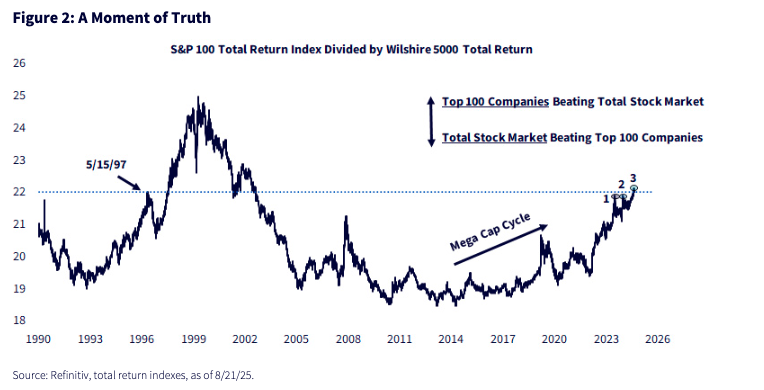

We're at a moment of truth with large versus small, too. When I plot the S&P 100 relative to the big, broad Wilshire 5000 index, it is making its third attempt at resistance levels that date to the 1990s. If recent action holds, this would mark an important breakout for large caps.

Because of small caps' multi-year struggle, the group is trading at a 21.8% discount to large caps on reported earnings (figure 3). It doesn't mean a small-cap resurgence will start tomorrow, but I do find solace in these valuation gaps resembling the situation that manifested in both the mid-1970s and the turn of the century.

Small caps are cheap, at least relatively, but there is a potential 2026 headwind that we should address.

The S&P 600 index of small caps has an easy hurdle this calendar year, in that the Street is penciling in earnings growth of just 2.7% to the S&P 500's 7.4%, according to Yardeni Research. But for next year, the Street has S&P 600 earnings jumping another 18.8% (the S&P 500 is expected to see earnings growth of 13.9%). Those will probably both be revised down, as usual, but it's still an easier hurdle for large caps than small caps.

As for the Dollar

It's one of the most common questions we get on large versus small. I wish I had some strong view here, but I don't. The problem with the dollar is you must get two things correct to make money:

- First, you have to forecast where the dollar is going, which is as good as heads versus tails

- Then, you must accurately identify what will happen to small and large caps if you get the dollar right

It's easier said than done, as I think figure 4 makes clear. Even if you accurately predict the dollar, good luck making heads or tails out of large and small because of it.

I have given the "dollar vs. cap size" concept a ton of thought over the years.

The common refrain goes something like this: "If the dollar rises, that is going to be bad for big U.S. multinationals, because their costs will be in expensive dollars and their customers will pay them in weak euros and weak yen. Therefore, if I'm bullish the dollar, I should go for small caps."

If it were only that simple. Dollar up, give me small caps. Everyone knows that. But it isn't necessarily true.

How about if "dollar up" is happening because some hedge fund is blowing up or a banking institution is dying in real time? In those markets, people are doing wild things like getting diamonds into Swiss safe deposit boxes, emptying ATMs and so on. In that world, where the grab for dollars is on, you probably aren't going to be happy with small caps.

Moral of the story: like small caps because you like small caps, not because of any U.S. dollar forecast that is on your mind.

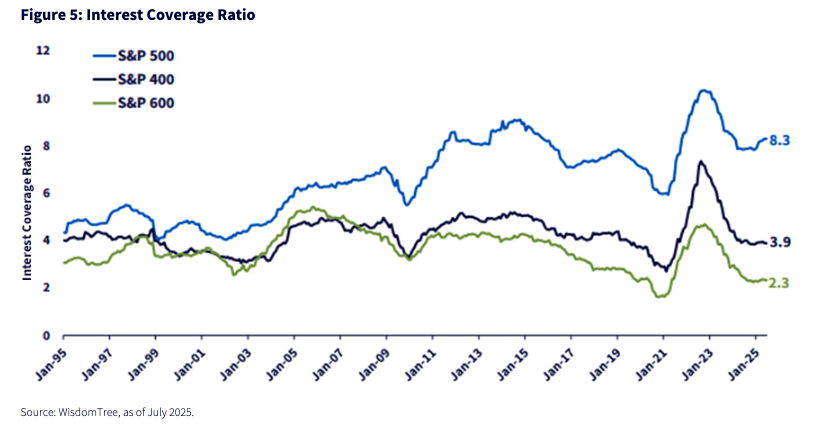

Now…that doesn't mean you can't engage in some old-fashioned Fed Kremlinology. That work could help small caps because of a narrative that figure 5 lays out. It shows a concept that is intuitive: as a collective, large caps tend to stand on sturdier balance sheet ground than small caps. Interest coverage (earnings before interest and taxes divided by interest expense) is a notably different scene as you move across the cap spectrum.

1 Performance figures from WisdomTree's PATH software, as of 8/27/25.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.