The U.S. dollar has experienced a notable decline in value this year relative to a broad basket of foreign currencies. This depreciation has meaningfully affected the investment returns of U.S. based investors holdings in international stocks and bonds. As the dollar weakens (or strengthens) against foreign currencies, the returns on foreign investments increases (or decreases) when translated back into U.S. dollars.

The U.S. dollar has experienced a notable decline in value this year relative to a broad basket of foreign currencies. This depreciation has meaningfully affected the investment returns of U.S. based investors holdings in international stocks and bonds. As the dollar weakens (or strengthens) against foreign currencies, the returns on foreign investments increases (or decreases) when translated back into U.S. dollars.

For example, when a U.S. investor buys a stock listed in Europe, they assume not only equity risk but also currency risk, specifically the EUR/USD exchange rate. If the euro depreciates by 10% against the dollar while the European stock gains 10% in local currency terms, the investor would see a flat return in dollar terms. In this way, currency fluctuations can either amplify or erode investment results.

Over shorter periods, exchange rate movements can significantly impact portfolio performance. This is well illustrated by the performance gap between a currency-hedged foreign Index and its unhedged counterpart year-to-date (see exhibit 1). The difference between the two reflects how much impact currency swings can have in the short term.

There are three primary drivers of U.S. dollar exchange rate movements:

- Interest Rate Differentials: When U.S. bonds, such as Treasuries, offer higher yields than their foreign counterparts, global investors are often drawn to U.S. dollar denominated assets to capture the yield advantage, which pushes the dollar higher.

- Safe-Haven Demand: In times of global market stress, the U.S. dollar is often viewed as a safe haven. Global investors buy more dollars, which drives up its value during periods of elevated volatility.

- Reserve Currency Status: The U.S. dollar is the dominant global reserve currency and widely used in trade along with as a holding for central banks. This structural demand supports the dollar’s strength over time.

Despite these drivers, timing currency movements is extremely challenging. We have implemented a currency hedge strategy only once, and for a limited time, because the risks of mistiming can outweigh the benefits in our opinion.

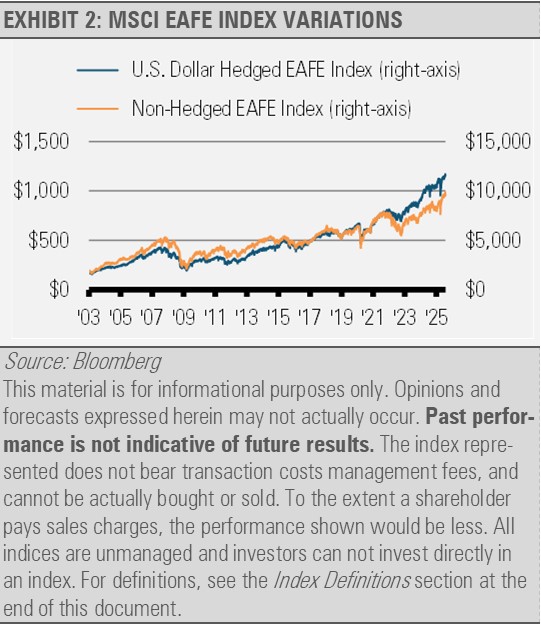

Our cautious approach stems from the observation that, over the long term, currency fluctuations have had a minimal impact on investment returns. As shown in the chart below, hedging currency risk tends to have little impact on long-term performance. However, some studies suggest that long-term strategic currency hedging can modestly reduce portfolio volatility.

Understanding currency impact is essential when comparing global investments. For instance, roughly half of the recent outperformance of international equities relative to U.S. large-cap stocks this year can be attributed to the weakened U.S. dollar. As the dollar has strengthened in recent weeks, this performance gap has narrowed, though it remains meaningful.

Ultimately, while currency moves can affect returns in the short run, their long-term influence is limited. Therefore, we advise investors to avoid overreacting to currency swings and instead focus on enduring investment strategies that have historically delivered more consistent results over time.

Originally published at Stringer Asset Management

For more news, information, and strategy, visit the ETF Strategist Content Hub.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Index Definitions:

MSCI EAFE US Dollar Hedged Net Index – This Index is designed to represent a close approximation of the return that can be achieved by hedging the currency exposures of the Index in the one-month forward market at each end of month.

MSCI EAFE Net Total Return USD Index – This Index covers developed market countries in Europe, Australasia, Israel, and the Far East. Indices with net dividends reinvested use the same dividend minus-tax-credit calculations, but subtract withholding taxes retained at the source for foreigners who do not benefit from a double taxation treaty.

Read more commentaries by Stringer Asset Management