FaST (Few Sentence Takeaway): Markets were supposed to stumble under the weight of tariffs, tight monetary policy and weakening consumer sentiment, but earnings say otherwise. With Q2 results, the July FOMC and shifting trade dynamics all converging, we're finally starting to find out what truly matters: guidance, not just headlines.

It was supposed to be a difficult quarter. Tariffs, tighter financial conditions and a wary consumer were expected to weigh heavily on corporate earnings. Yet, that pessimism is being steadily walked back.

Companies are managing the tariff transition with surprising finesse. Stage one: withdraw or slash guidance is largely behind us. Stage two: reinstating or raising that guidance is well underway. Stage three: price increases and margin defense is just getting started.

P&G Tariff Guidance Revision

So category growth, question mark in the short term. Midterm, we expect it to return to 3% to 4% growth rate. The levers for us are the same levers that we talk about in our integrated strategy. I think the tariff impacts that are visible to us right now at a gross level are in the range of $1 billion to $1.5 billion. So it's not immaterial. For us to offset those in the short term, we have to consider productivity, which we will double down on, and we have a very strong productivity plan over the next 3 years that I feel very bullish about.1

But then …

The Company estimates a headwind of around $200 million after-tax from unfavorable commodity costs and a net headwind of roughly $250 million after-tax from modestly higher net interest expense and its core effective tax rate. In addition, the Company's outlook includes around $1 billion dollars before-tax, or approximately $800 million after-tax, in higher costs from tariffs. The Company said it expects a tailwind from foreign exchange rates of approximately $300 million dollars after-tax. Combined, the net of these impacts equates to a headwind of $0.39 per share for fiscal 2026, or a six percent drag on core EPS growth.2

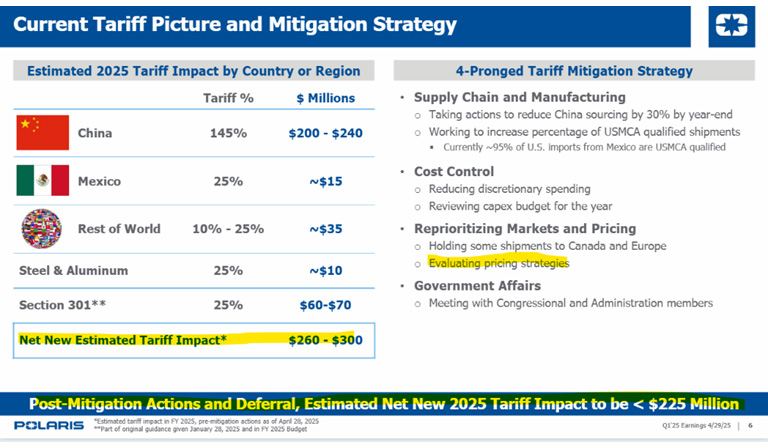

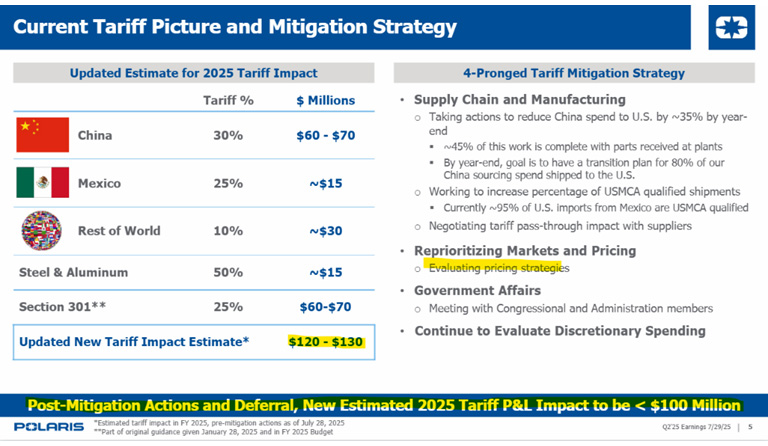

Procter & Gamble didn't post a blowout quarter, but they significantly revised their expected tariff hit—from a $1 billion–$1.5 billion range down to approximately $1 billion. That's not insignificant mitigation, but it is clarity. The same goes for Polaris Industries and Stanley Black & Decker, both of which recalibrated their estimates as tariff negotiations evolved. Not every supply chain is favorable, and not every company has navigated it equally well, but margin preservation is becoming a real and replicable story.

Source: Polaris Industries investor presentation, 4/29/25 (emphasis added).

And then …

Source: Polaris Industries investor presentation, 7/29/25 (emphasis added).

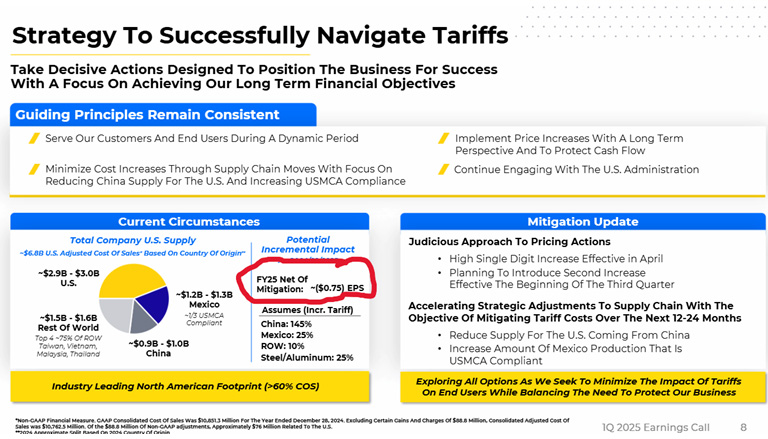

Source: Stanley Black & Decker investor presentation, 4/29/25 (emphasis added).

And then …

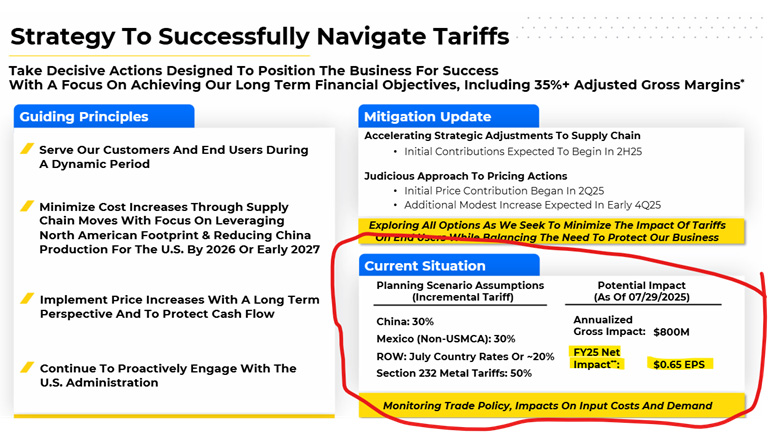

Source: Stanley Black and Decker investor presentation, 7/29/25 (emphasis added).

This is no longer a story of damage control—it's becoming a blueprint for resilience. And one of the most underappreciated signals this quarter is just how many companies are using tariff visibility to guide margins higher, not lower.

It's not just about tariffs, either. Earnings from P&G, Colgate and Kimberly-Clark are giving us a clearer sense of how corporates are responding to cost pressures. Royal Caribbean and Hershey are revealing pricing power. Meta and Microsoft are outlining capex strategies and the pace of AI monetization. Amazon, of course, is speaking to all of the above.

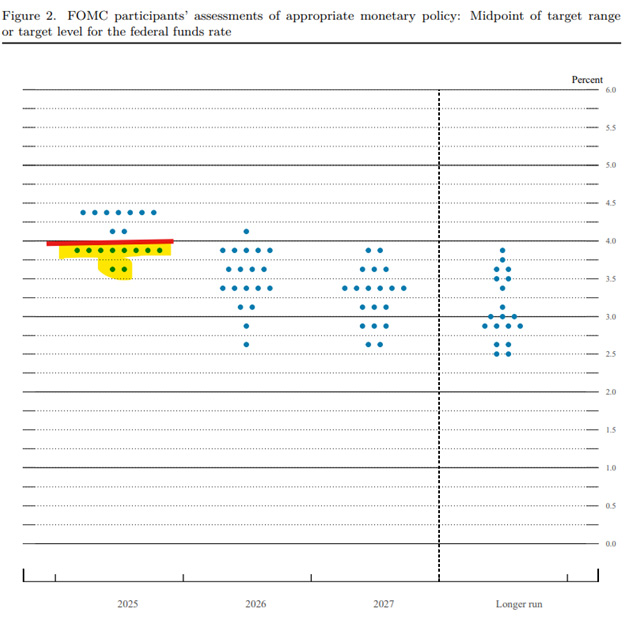

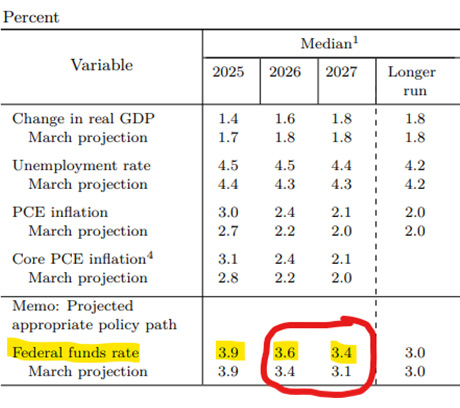

The Federal Reserve adds another layer. This quarter's FOMC decision was expected to be uneventful, no rate cuts, minimal surprises. But like corporate earnings, it's the guidance that matters. In June, the FOMC penciled in a more hawkish stance in the out years. That now gives them room to surprise dovishly without deviating too far from previous positions. The voices most eager to cut are already signaling their views. Dissent is likely, and so is a shift in tone.

FOMC Summary of Economic Projections (SEP)—June 2025

Source: FOMC SEP, as of June 2025 (emphasis added).

and

Source: FOMC SEP, as of June 2025 (emphasis added).

If dovish language emerges, paired with better-than-feared earnings, markets may begin to price in the end of the elevated interest rate environment—just ahead of Jackson Hole.

That's what this month is really about: finding out.

Is the consumer resilient? Are companies adapting profitably to tariffs? Is the Fed preparing to pivot? If the answer to all three is "yes," it could be a month to remember. If not, well—still a month to remember.

1 Source: P&G earnings call, 4/24/25 (emphasis added).

2 Source: P&G earnings call, 7/29/25 (emphasis added).

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.