Key Takeaways

- Treasury floating rate notes (FRNs) have provided a rare pocket of stability in 2025’s volatile rate environment, offering ultra-short duration exposure without the sawtooth yield swings seen across the fixed coupon curve.

- While credit-oriented ultra-short strategies like JPST and JAAA may offer higher yields, their performance suffered during recent risk-off episodes, highlighting the hidden risks of credit exposure even in short-duration vehicles.

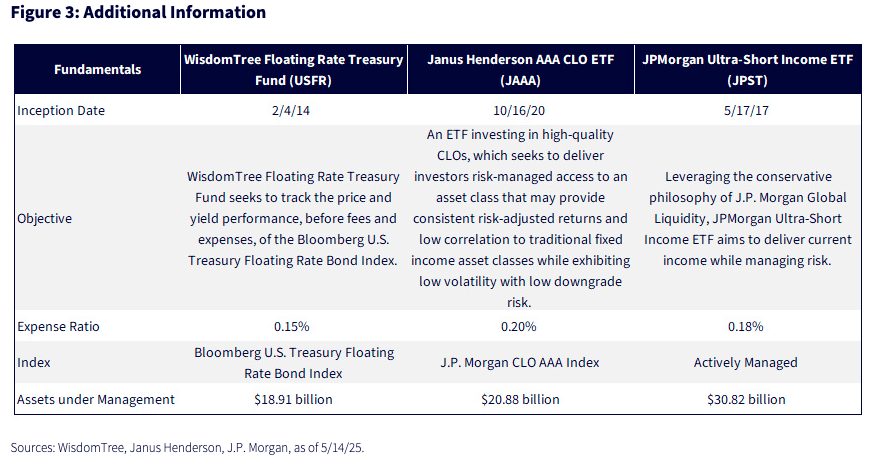

- The WisdomTree Floating Rate Treasury Fund (USFR) seeks to offer investors a low-volatility, credit-free alternative for managing interest rate risk while maintaining ultra-short duration positioning.

Our overarching theme for U.S. fixed income has been, and will continue to be, based on the premise that interest rates will stay at more historically “normal” levels, but that, within this backdrop, investors will face heightened volatility. Without a doubt, looking at the U.S. Treasury (UST) market’s behavior through the first four months of the year, this landscape has been underscored. As a result, fixed income investors will need to make some potentially challenging investment decisions, where at first glance, a solution may seem like a suitable one, but when uncertainty enters the mix, an unexpected result could occur.

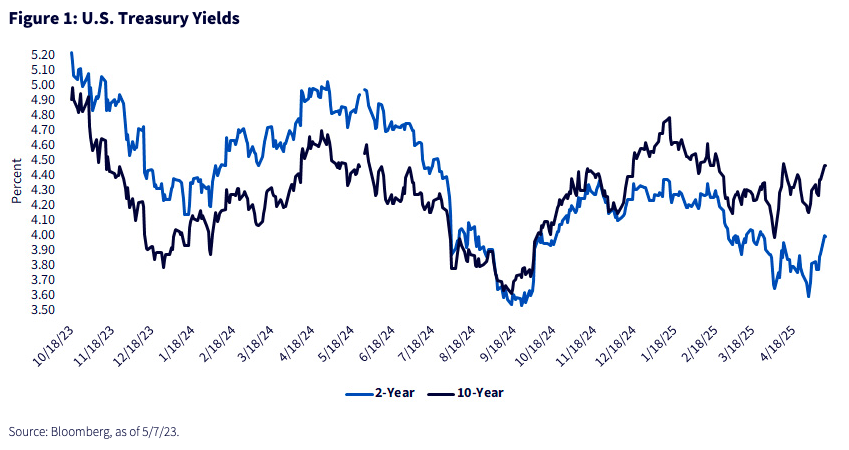

Let’s first take a look at some of that volatility I just mentioned. Since reaching their near-term peak readings around mid-October 2023, Treasury fixed coupon yields have experienced a roller-coaster ride, to say the least. In addition, even within these broader ups and downs, yield levels have shown visible sawtooth patterns as well.

It is also important to note that no sector of the Treasury fixed coupon curve was spared. As the graph illustrates, both shorter- and longer-dated maturities experienced the same results. As you can see, this short- and long-run volatility has continued right up until this writing here in 2025.

The only sector of Treasuries that has not been subject to this volatility is floating rate notes (FRNs). UST FRNs are reset with the weekly 3-month t-bill auction, plus a spread, and as a result, are anchored by the Fed Funds Rate and not impacted by speculative trading activity. Thus, tariff uncertainty and recession and/or inflation fears are not part of the daily trading mechanism that the fixed coupon maturities are confronted with.

The Credit Factor

Oftentimes, when bond investors are looking to use ultra-short duration as a hedge against volatility, they consider using structures that, unlike UST FRNs, are not 100% Treasuries, but rather are concentrated with either corporate credit or collateralized loan obligations (CLOs). Interestingly, these types of vehicles entail both a rate and credit component as a result.

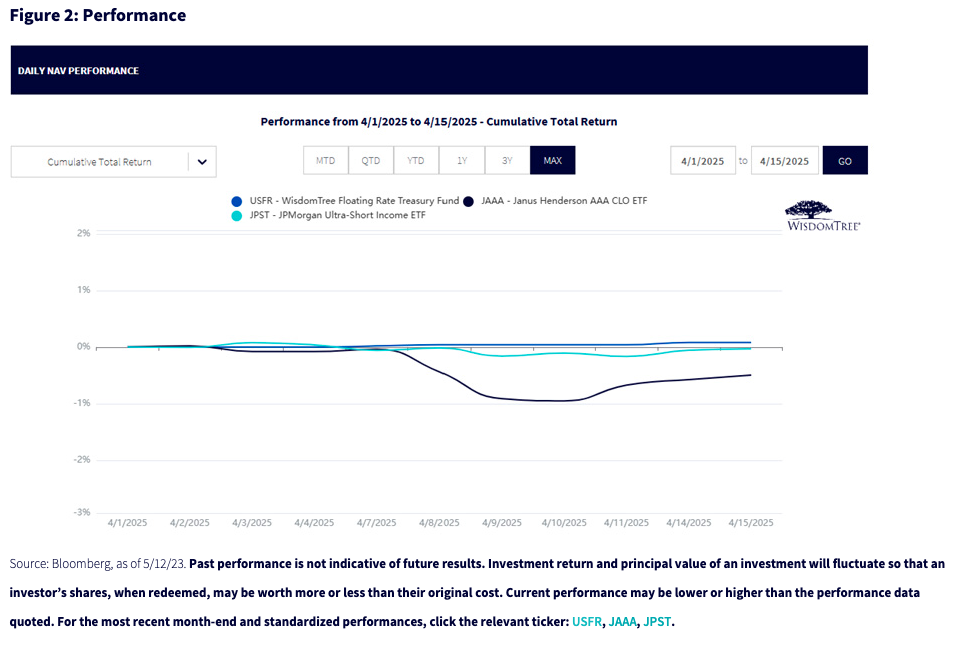

While ultra-short credit and/or CLO instruments can offer somewhat higher yields than Treasury FRNs, there is a reason: potential credit risk. Relatively recently, markets have witnessed a period where the credit component can overtake the duration aspect of a fund, specifically during a risk-off episode. Obviously, I’m referring to the post-Liberation Day sell-off where two of the largest and most well-known funds in the ultra-short credit and CLOs bucket, JPMorgan Ultra-Short Income ETF (JPST) and Janus Henderson AAA CLO ETF (JAAA), experienced negative returns, but the WisdomTree Floating Rate Treasury Fund (USFR) did not.

Conclusion

While this period of negative activity may have been somewhat short-lived, investors who put their funds in the ultra-short duration bucket are not expecting to see potential statement risk. Treasury FRNs are direct obligations of the U.S. government and do not carry that type of credit risk. USFR is a means to invest in the ultra-short duration bucket with exposures only to Treasury FRNs.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Important Risks Related to this Article

USFR: There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

JAAA: The biggest risk is that the Fund’s returns and yields will vary, and you could lose money.

JPST: Investments in asset-backed, mortgage-related and mortgage-backed securities are subject to certain risks including prepayment and call risks, resulting in an unexpected capital loss and/or a decrease in the amount of dividends and yield. During periods of difficult credit markets, significant changes in interest rates or deteriorating economic conditions, such securities may decline in value, face valuation difficulties, become more volatile and/or become illiquid.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.