Recent market volatility has shaken the faith of some investors. However, our analysis shows that historically, staying invested through volatile periods has provided superior returns when compared to selling when volatility rises and reinvesting later. Some of the greatest upside returns have happened shortly after volatility spikes, and investors who have pulled out have missed out on important opportunities for portfolio gains.

In October 2014, we posted an historical examination of the S&P 500 index following sharp rises in the CBOE VIX that measures investors’ expectations of volatility. The results showed average gains for the S&P 500 in the periods following spikes in the VIX. These gains would obviously be missed opportunities for investors who sell their positions when the VIX surges.

Given recent volatility, we updated and expanded this study to include the time since 2014, to see if the new history confirms the previous findings. Examination of the new results sheds some light on the price paid, through recent history, for selling positions when volatility is elevated, and specifically, when it spikes for the first time after an interval of low volatility. Our new results confirm that the VIX, while indeed predicting periods of increased volatility, does not predict overall losses in the S&P 500; as before, the realized returns during the volatile period have slightly greater upside overall than downside and result in gains once compounded.

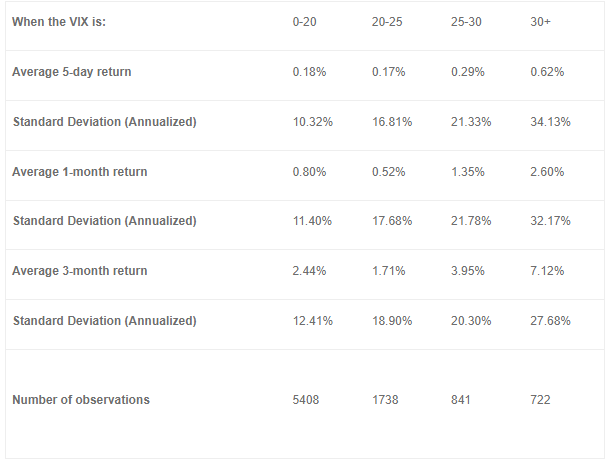

To start, we present an exploratory summary of forward returns in general, across the entire dataset, for different ranges of the VIX, including both first-time spikes and continuing elevated VIX, in other words all times when the VIX attains the specified ranges. The 1-week, 1-month, and 3-month forward returns (5 market days, 21 days, and 63 days) and their annualized standard deviations are shown in Table 1.

Table 1: S&P 500 returns following observed values of the CBOE VIX, Jan 2nd 1990 - Aug 5th, 2024

Table 1 validates the VIX as a signal of imminent volatility. Increased values of the VIX uniformly correspond to increased volatility in the following period, for the time interval spanning 1990-today (Aug 5th, 2024). For the category of greatest volatility, when the VIX is above 30, the observed volatility is highest in the five days immediately afterward and decreases as the time window is expanded.

Moreover, this table shows uniformly greater average returns as VIX increases to the 25-30 and 30+ ranges, although average returns are smallest in the VIX 20-25 range. The returns for the 3-month period following days when the VIX is greater than 30 are quite impressive, although the risk is double its value for calm times in the market. It should be stressed that all average returns are positive, and so far in history the market has recovered from every downturn, often relatively soon after the crash. There is no reliable way to participate in these gains, based on available signals, other than staying invested.

The original study examined the periods when the VIX first passes into elevated ranges after relative calm. These are the times most likely to inspire doubt in risk-averse investors, since there is elevated downside potential and the time seems right to pull out if pulling out is a viable strategy to avoid downside returns. To examine the cost of pulling out at the first VIX spike, we look at the 1-week, 1-month, and 3-month returns for periods when the VIX first rises, i.e. there are no such elevated values of the VIX in the previous week. The average returns for these periods are shown in Table 2. The “Cumulative lost return” rows are calculated as the complete return from the possibly overlapping time segments of designated length following each trigger. The overlapping time segments are counted only once, so the calculation is a realistic estimate of wealth lost by selling the entire position and buying it back after 1 week, 1 month, or 3 months every time the VIX hits the threshold for the first time in 5 market days.

Table 2: Average forward returns and cumulative lost returns for the S&P500 following VIX spikes at three trigger levels, for three different time periods.

Table 2 is divided into time periods to serve as an update to the previous blog post.

This table confirms and validates the findings of the original study, which showed that investors in the S&P 500 who pull out when the VIX passes into higher ranges have historically lost money by not participating in some of the greatest gains in the market. These gains often happen in the period immediately following volatility spikes. In recent history, pulling out of the S&P 500 based on the strategies presented here would have resulted in net losses for investors, even pulling out for only five days after the spike. This may seem counterintuitive, but risk does have an upside, and historically, the best investment strategy has been to hold during periods of volatility. Indeed, according to this study, S&P 500 investors who have pulled out for three months whenever the VIX spikes to 20 since 1990 currently hold less than a third the value that they could have, had they stayed invested the whole time. Adopting this strategy since 2010 would result in half the current wealth, sacrificing a potential 132% gain.

To summarize, we have updated our simple examination of S&P 500 performance after VIX spikes, and our findings still stand. Our evidence suggests that across broad markets, investors will sacrifice gains over time if they withdraw at the first sign of turbulence. Volatility is unfortunately a fact of life for investing in capital markets, but investors who weather the storms are rewarded over time with superior returns.

By Dr. David Esch

Originally published at New Frontier Advisors

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures:

Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal. The indices are not investable securities.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© New Frontier Advisors

Read more commentaries by New Frontier Advisors