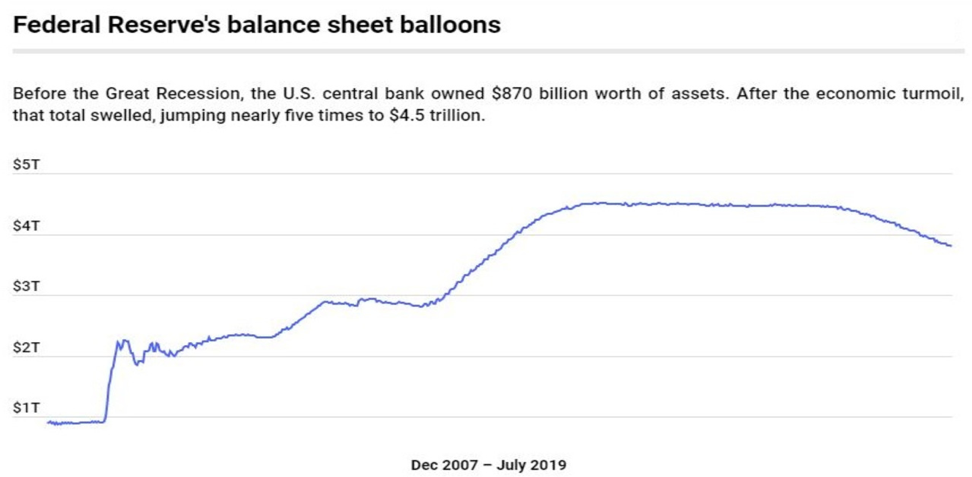

The Federal Reserve’s quantitative easing program in response to the Great Recession in 2008-09 resulted in the Fed buying more than $4T worth of Treasury bonds and mortgage backed securities to increase the supply of money in the financial system.

As the economy recovered, the Fed began to reverse that program, slowly reducing its portfolio of bonds. According to classical macroeconomic monetary policy, the plan was to have nearly robotic increases in the Fed Funds rate toward the theoretical natural rate of 3-3.5%. The theory of the natural rate is of a not-too-high not-too-low interest rate for hands-off monetary policy for the economy. Achieving the natural rate is a means of re-arming the Fed’s store of ammunition for managing the economy in any future unanticipatable economic collapse.

But monetary policy can be a punchbowl for politicians concerned with re-election. Cutting the Fed Funds rate in the U.S. will stimulate the economy by reducing the cost of servicing debt and encouraging investment. The impact, of course, all other things the same, is a reduction in the value of the currency. Domestic voters, however, may notice little side effects of a reduction in purchasing power.

The Fed raised interest rates four times last year, drawing severe criticism from President Trump. While the American economy is robust and unemployment historically low, the effects of the president’s $1.5T tax cut are waning and his trade war has begun to hurt some American industries, as well as slow global economic growth. Under pressure from the President, including threats of replacing the newly installed Federal Reserve chairman, the Fed reversed course and began to consider the potential weaknesses in the economy.

SOURCE: FEDERAL RESERVE BANK OF ST. LOUIS, JULY 2019

In a global economy where each country is concerned only with themselves, there is little incentive to modulate policy for global implications. This was evident recently when President Trump called out Dr. Mario Draghi, the outgoing European Central Bank President, for a policy of additional interest rate cuts that was motivated to stimulate Eurozone growth, but also had the side effect of reducing the value of the euro vis-à-vis the dollar.

At the moment, there are roughly 15T dollars of debt “earning” negative interest rates in the global economy, a state not anticipated in modern macroeconomic theory first proposed by Keynes and Samuelson during the 30s and 40s. Negative-yielding debt now accounts for more than 25% of the investment grade universe as represented by the Bloomberg Barclays Global Aggregate Index.

Dr. Draghi’s willingness to use more negative interest rate borrowing to stimulate the Eurozone economy is very risky. Modern monetary theory was not designed for such extreme situations. No one can predict whether the effort will succeed or what consequences will result. Problems of European fragmentation remain. Italy is fiscally unstable, and Brexit further challenges the bloc’s unity.

Despite Dr. Draghi’s economic and political brilliance, the problem has always been that there is no central banking system in the Eurozone and no political will for a coherent fiscal stimulus policy. A thriving Eurozone economy propelling global economic growth seems unlikely for the foreseeable future.

Macroeconomic monetary policy remains a theory in progress.

Dr. Richard Michaud is the President and Chief Executive Officer at New Frontier. He earned a Ph.D. in Mathematics from Boston University and has taught investment management at Columbia University. He is the author of Efficient Asset Management: A Practical Guide to Stock Portfolio Optimization and Asset Allocation (1998, 2nd ed. 2008 with Robert Michaud), a CFA Research Monograph (1999) on Global Asset Management, and numerous academic and research articles available on www.ssrn.com and www.researchgate.net. He is co-holder of four U.S. patents in portfolio optimization and asset management, a Graham and Dodd Scroll winner for his work on optimization, a former editorial board member of the Financial Analysts Journal, associate editor of the Journal Of Investment Management, and former director of the “Q” Group.

New Frontier Advisors is a Boston-based institutional research and investment advisory firm specializing in the development and application of state of-the-art investment technology. Founded in 1998 by the inventors of the world’s first broad spectrum, patented, provably effective portfolio optimization process, the firm continues to pioneer new developments in asset allocation and portfolio selection. Based on practical investment theory, New Frontier’s services help institutional investors across the globe to select and maintain more effective portfolios.

© New Frontier Advisors, LLC

© New Frontier Advisors

More Factor-Based Investing Topics >