Risk appetite has returned to European equity markets. Is there a way to capture the rally of value stocks while mitigating risks across an unsettled region? Focusing on cash flows can make the difference.

Undervalued stocks have led the way in Europe’s recent risk rally. Since the US election through December 12, the MSCI Europe Value Index has outperformed the broad market by over 2.4%. That continues a trend we’ve seen this year, in which value stocks in Europe have advanced by over 5.5% in euro terms, outperforming the broad index by over 5%. This year’s turnaround has been dramatic following five difficult years during which pervasive risk aversion suppressed returns of riskier stocks with recovery potential.

VALUE STOCKS WITH LESS VOLATILITY

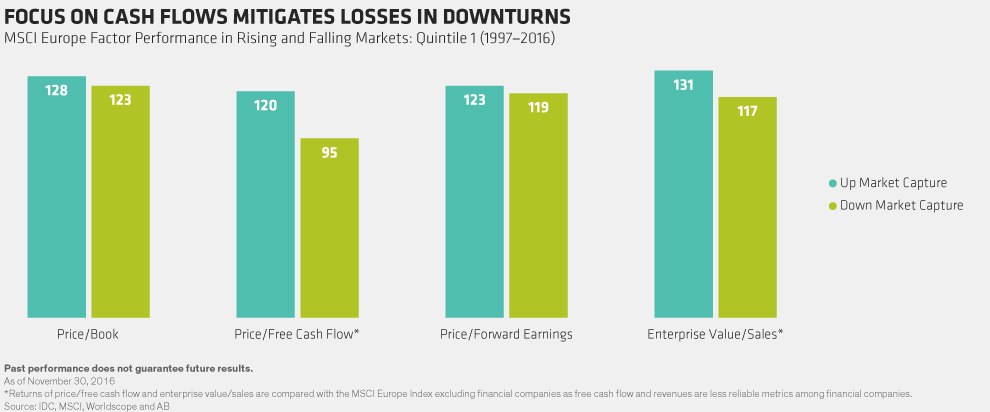

Investors are still uneasy. With the region facing a series of major political risks in the coming months and Brexit a probable source of instability for years to come, bouts of market turbulence and renewed flights to safety are expected. But we believe there is a way to take advantage of the outperformance potential of cheap stocks without adding too much unwanted volatility. The key is to emphasize cash flows in both quantitative and fundamental tools for finding undervalued stocks, which can help protect portfolios during downturns and create smoother return patterns.

The first step is to adopt a broader set of measures for discovering value. Investors have traditionally relied heavily on valuation measures based on accounting earnings and book value to identify undervalued stocks. Over the long run, stocks that are cheap on these measures have indeed outperformed. But the performance of stocks with attractive price/earnings or price/book value can be erratic from year to year. Our research shows that focusing on cash flows to identify attractive valuations can smooth the pattern of returns.

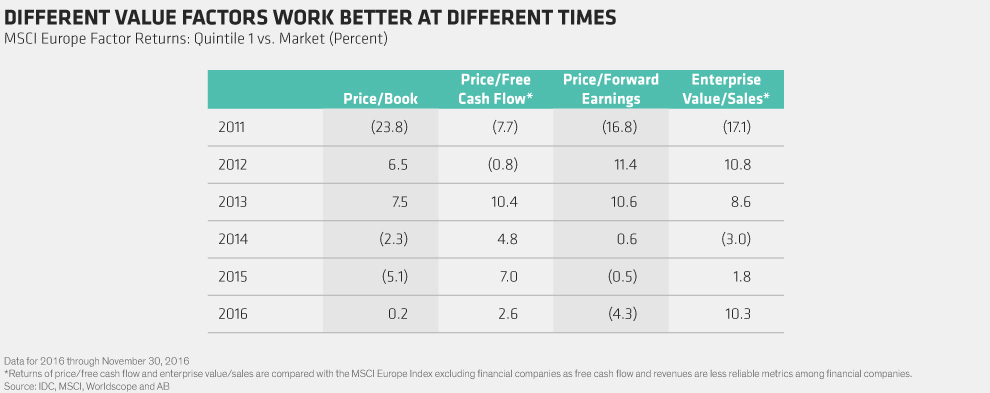

Since the outbreak of the eurozone crisis in 2011, performance patterns for different value metrics have been inconsistent (Display). For each value metric, we compared the performance of the cheapest 20% of stocks in the European universe against the market. A positive number shows cheap stocks doing well.

Different return patterns reflected market conditions each year. In 2011, all the factors did poorly during a severe bout of risk aversion. In 2013, all the metrics did well as a value recovery gathered steam. But in the last three years, return patterns have been more complex. Stocks that were cheap based on accounting book value and earnings underperformed while, in contrast, stocks with strong but undervalued cash flows—identified by the price to free cash flow metric—outperformed significantly. In other words, leaning in to cash flow helped smooth a value investor’s pattern of returns.