Over the past three decades, the Federal Reserve has raised the official short-term rate when the US economy has shown signs of overheating. When the Fed moves, savvy bond investors also move—toward opportunity.

Part of the Fed’s congressional mandate is to promote job growth and control inflation, so it hits the brakes when the US economy approaches full employment or when there are signs of higher inflation. The Fed has held short-term rates near zero since December 2008, but has been signaling that it will soon start to tap the brake pedal and reduce the amount of monetary stimulus it is providing the economy.

Long-Term Muni Bonds Have Held Their Value

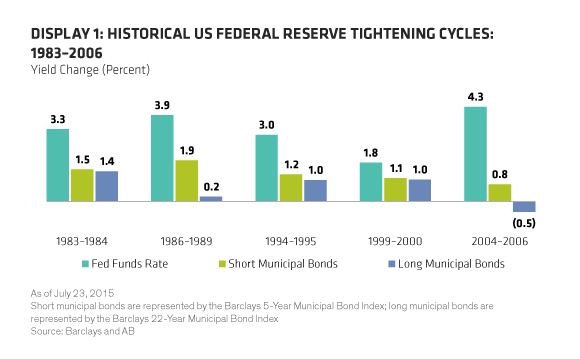

The Fed has raised the fed funds rate five times since 1983 (Display 1). During these episodes, longer-term bonds haven’t suffered the way investors feared. That’s because the Fed has been pretty effective at slowing down growth and tempering market expectations about inflation. Muni bond yields, in particular, haven’t moved in lockstep with fed funds rate changes. Short-term muni yields have increased only half as much, and long-term muni yields by even less over the whole tightening cycle.

When Necessary, the Fed Takes Action

Despite the buffering impact of muni bonds, many bond investors get a case of the nerves at the thought of higher rates, since rising yields tend to push down prices on their bond portfolios. While that’s true in the early months of a Fed policy reversal, bond markets have rallied over time, as bond markets become convinced that the Fed’s brakes are working.

The Bond Market Likes a Decisive Fed

The Fed took decisive—and successful—action against double-digit inflation in the 1970s. Since then, officials have convinced bond investors that the Fed’s economic policies protect the future purchasing power of bond portfolios. Many investors understand the notion that US monetary policies will dampen inflation pressures, helping to preserve the purchasing power of their future bond income.

Muni bond investors who both understand and embrace that notion have continued to add to their portfolios, even during cycles when the Fed is raising short-term rates. And in past cycles, this conviction has allowed them to benefit from higher interest rates and the market’s confidence in the Fed.

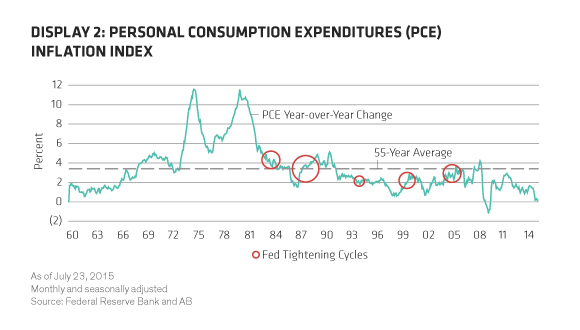

The expectation that the Fed will begin tightening in the months ahead is growing, but so is the forecast for lower global inflation rates. This is partly due to the abundant labor supply, factory capacity and a surplus of most industrial commodities. US long-term inflation rates have tumbled in the last three decades, as confidence in the dollar has surged (Display 2). The upshot: we don’t think bond investors need to fear the effects of inflation.

Opportunity in Steady Fed Policy Moves

Of course, the past doesn’t always indicate the future, and the Fed has never started a rate-hike cycle from such a low level of interest rates, or with such a large balance sheet. But we believe that it will be successful in managing monetary policy.

Over the past thirty years, the Fed has acted responsibly and decisively to keep the economic engine from overheating and to prevent inflation from eating away at bond income. As the Fed waits with its foot poised over the brake pedal at the onset of a new tightening phase, muni bond investors should feel confident that those brakes will work—and consider playing offense.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.