After withstanding a multitude of global challenges last year, emerging markets look poised for improvement as inflation recedes and the path of monetary policy comes into view.

Inflation is receding and real interest rates are climbing in EM after a year of tightening monetary policy.

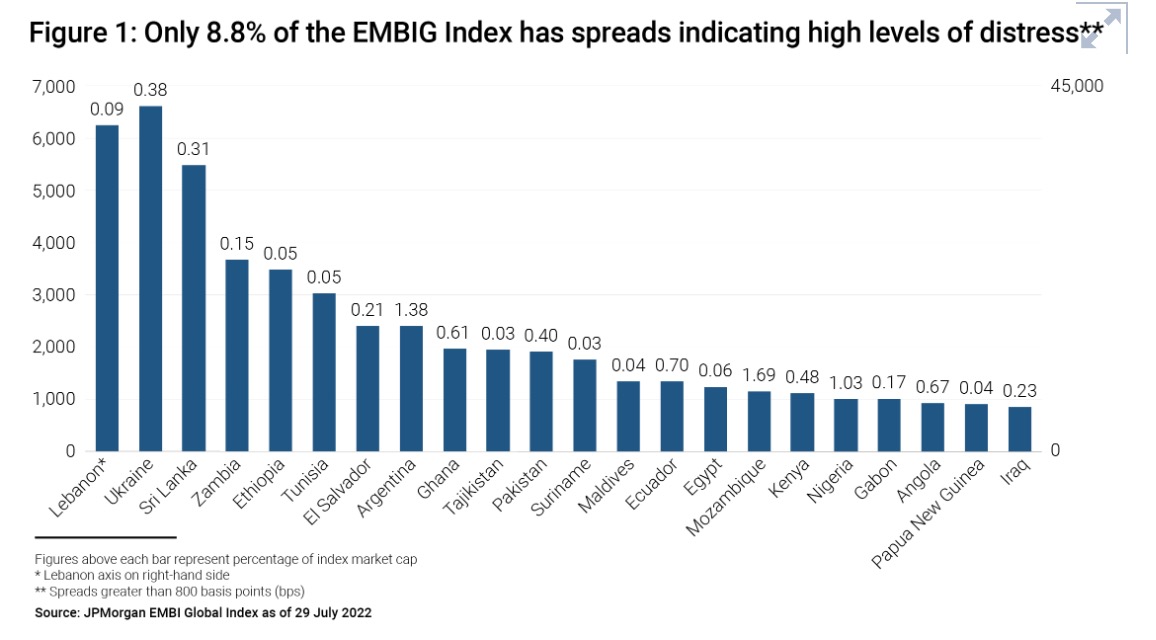

Emerging market valuations appear attractive, but country-specific risks can be critical to monitor amid global inflation and rising interest rates.

The varied responses of individual countries to global inflationary pressures have contributed to elevated real-rate differentials between developed and emerging markets.

Much of the global economy has transitioned quickly from an early-cycle recovery to a mid-cycle expansion that now appears to be rapidly progressing toward late-cycle dynamics.

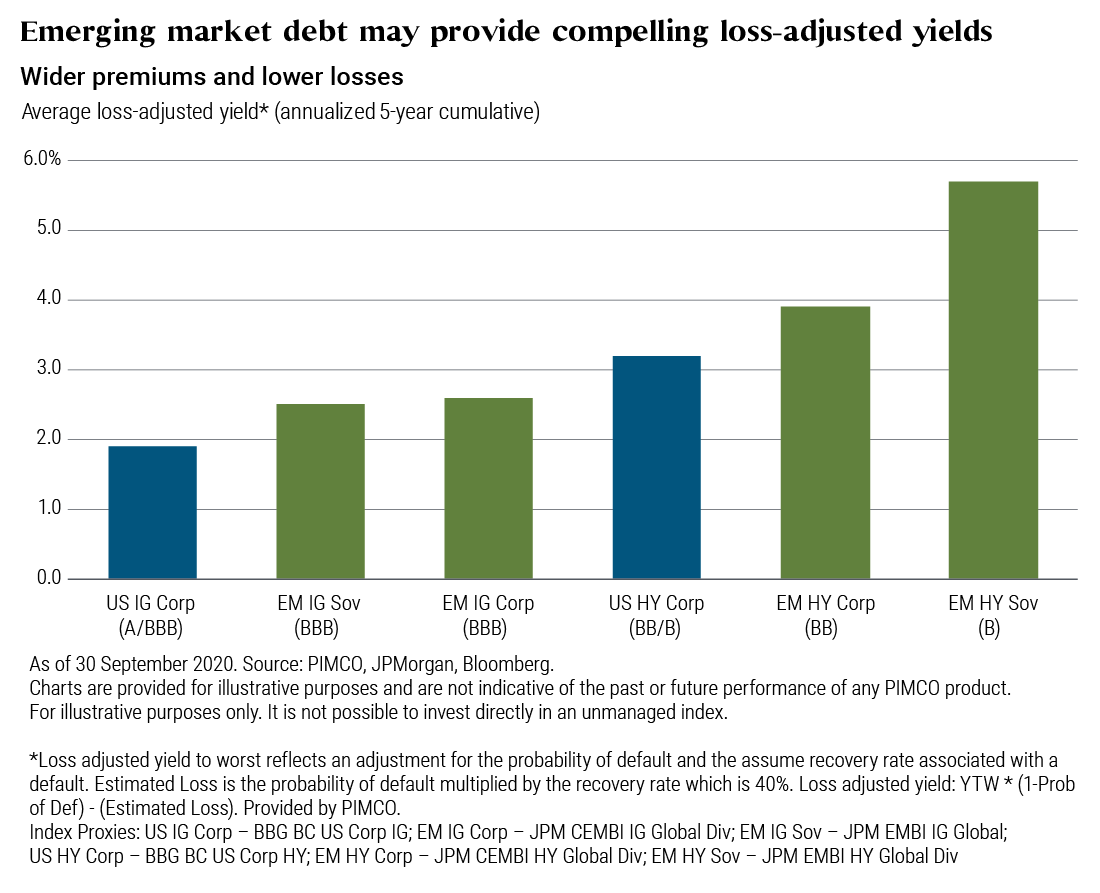

Debt of many emerging market countries can offer robust yields and enhance portfolio diversification, provided the asset manager has the resources and sophistication to avoid potential pitfalls.

The Federal Reserve wants to avoid a crisis of confidence.

Trade, geopolitics, and emerging markets were top of mind at the recent annual meetings

Global central bankers, finance ministers and representatives from the private sector and civic groups gathered in Bali recently for the annual meetings of the IMF (International Monetary Fund)/World Bank Group. Below are 10 key takeaways from the discussions.

Environmental, social and governance (ESG) indicators are integral to PIMCO’s sovereign credit assessments, which inform our investment decisions. But how exactly do we incorporate ESG considerations into our decisions?

Global central bankers, finance ministers and representatives from the private sector and civic groups gathered in Washington recently for the spring meetings of the IMF (International Monetary Fund)/World Bank Group. With trade policy, geopolitics and emerging markets currently top-of-mind for many investors, the meetings were especially relevant this year.

Integrating ESG into sovereign risk analysis adds a holistic and long-term perspective that is aligned with investing in sovereign fixed income.

Global central bankers, ministers of finance and representatives from the private sector and civic groups gathered in Washington, D.C., last week for the Annual Meetings of the IMF (International Monetary Fund) and the World Bank Group.

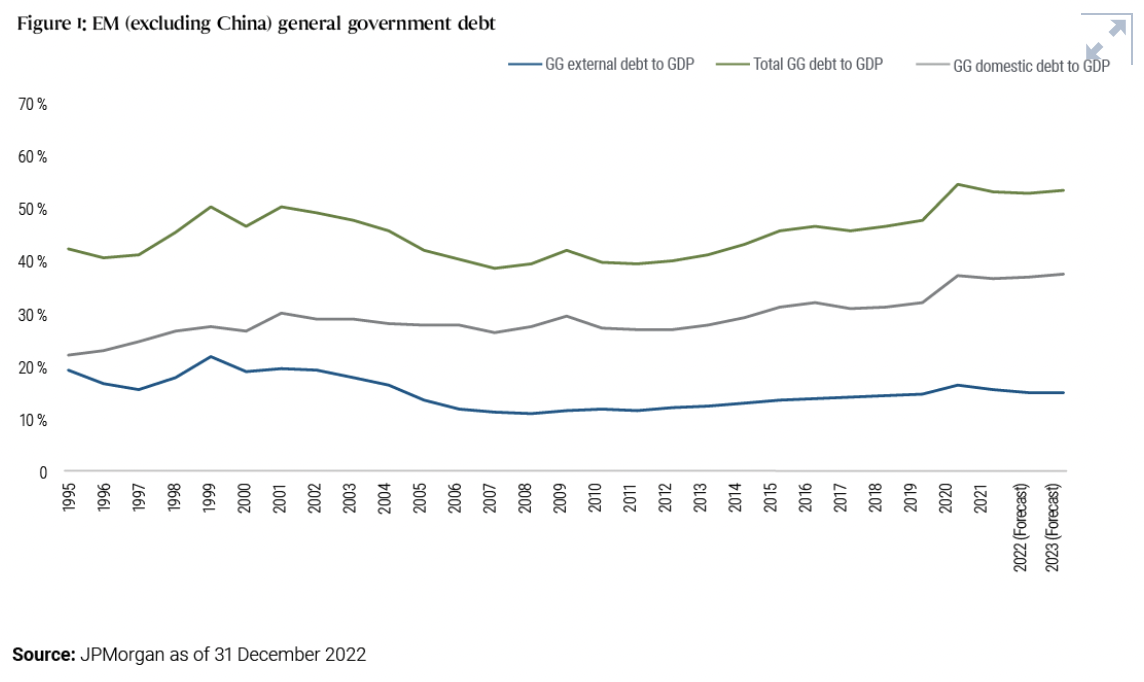

While PIMCO’s cyclical outlook is cautious overall, our outlook for emerging markets ex-China (EM) is more constructive. We expect further improvement in the EM macro picture as most emerging economies are at a different stage of the economic cycle than developed economies and they are still benefiting from relatively easy global policy conditions.

Brazil is often known for soccer, samba and pristine beaches. Among investors, something else also stands out about Brazil: double-digit interest rates that are significantly higher than its peers’ (see chart). That may soon change.