As we have been holding calls with prospective and current investors of our firm, we have been arguing that the stock market is underwhelming the success of the economy.

Even before the war is over, the winning side needs to consider how to “win the peace” which will follow.

My wife are new residents to the Phoenix-area, since moving here in the middle of 2020. We haven’t fully settled on where to send a couple of our kids to school.

We think this is an excellent time to ponder the thoughts of Buffett and Munger.

Fortunately, human behavior has a history of repeating itself at extremes. The worst buying decisions are made at the top. Just like bonds, the convexity is true when yields rise going forward. It’s a slippery slope and could be vexing.

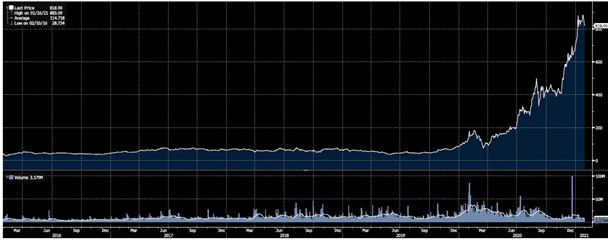

We have enjoyed watching what happens in the late stage of a financial euphoria episode play out in the escapades of millennial investors on Reddit, who seem to “rule the nation.” While politicians, regulators, the media and others try to sort this out, we thought some historical perspective might be helpful.

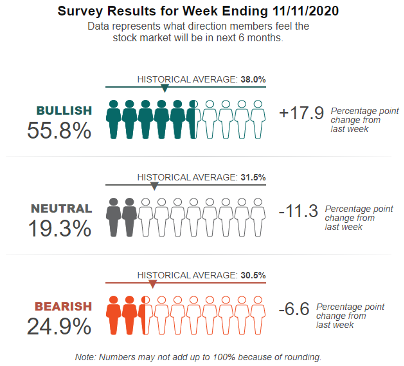

As we begin 2021, the investing public is tied up in a “frenzy,” to quote Charlie Munger from a recent interview. This “frenzy” can be captured a couple ways.

We were fortunate to watch a recent interview Charlie Munger did with Cal Tech as a distinguished alum. We consider him to be one of the most successful contrarian investment thinkers on the planet. At 96 years of age, he has no fear of being politically incorrect. We contrast this with the mountain of writing, media and rhetoric associated with the topic of climate change.

My wife brought me a box of ornaments that my mother has given to us over the years. I decided to check what I could sell them for on eBay (EBAY). What a great way to look at what is going on in equity capital markets!

As Buffett said, this looks like “one helluva party” with the individual investors, professional investors and insiders all joining in the fun. As a former fraternity member in college, the best parties were always when you couldn’t find anyone missing. It wreaks of that today in the stock market.

David Dreman’s book, Contrarian Investment Strategies, was gospel to investors when it was first published in 1979. Investors had been decimated by markets going nowhere over the prior 10 years. Stock investors were ready for something new. Dreman had produced a lot of success as an investor and wanted to share his gospel of contrarian value investing.

I got very excited when I came across an excerpt from Jordan Ellenberg’s book, How Not to Be Wrong. His book was written to teach readers how much logic and common sense is provided by math. He tells the story of Abraham Wald during World War II, who worked for the Statistical Research Group (SRG).

While listening to Rob Arnott on a recent Morningstar podcast, I became enamored with something that Arnott was emphatic about. He pointed out that the structural advantage of being a contrarian isn’t being smarter. Every winning purchase in the stock market comes as an opportunity cost to the seller.

Due to the pandemic, there is a sense of permanence on Wall Street to what has transpired. This permanence focuses on the changes that we have seen in the recent five months in our daily lives. These changes include shopping online versus shopping in-person, getting takeout versus sitting in a restaurant and working from home instead of talking sports around the water cooler with our colleagues.

The stock market is a big place with thousands of investments that you can make as an investor. It’s a frustrating place. There is a myriad of investing disciplines that you can seek out. As a millennial, my generation is learning this for the first time. Don’t kid yourself for one second: they will destroy wealth.

Everyone who owned common stocks in the U.S. went through hell in the first quarter of this year. The 36% decline in the S&P 500 Index in February and March was the fastest 36% decline of my lifetime. This hell was especially damaging to those of us who have a positive view of the U.S. economy over the next ten years.

The oddity of today’s stock market is exactly what any God-fearing value manager should pray for. There are very few scenarios in the last 50 years that can be used to model or forecast what is currently going on.

Late last year, there were three people that we observed as optimistic about the prospects of the oil business. These people were Warren Buffett, Sam Zell and Peter Lynch. In revisiting their comments before and after the shutdown of the economy, we can see that two of the three have significantly altered their opinion.

The capital markets are a highly complex system, where perturbations can cause a tidal change. Every business around the world has been affected by Covid-19. For a profitable business anywhere, this is a calamity. For a business that was losing money before this, it’s a tombstone.

Investors have been awoken to the carnage of the last three weeks. These circumstances, while unenjoyable, may be hiding the actual problems with today’s market. The unforeseen circumstances of today are no different than the past.

In a recent piece, Bloomberg journalist Keith Naughton laid out a wonderful counter-argument to the consensus of opinions for what the future looks like. His piece, “Millennials Could End Up Being a Boon to the U.S. Auto Market,” talks about the good news of the auto businesses future via Benchmark analyst Mike Ward’s research.

One of our favorite financial writers is Bloomberg’s John Authers. He recently wrote a tongue-in-cheek article about an investment company by the name of Hindsight Capital. In hindsight, or in the company’s case, Hindsight Capital, he talked about what the firm did and what you should have done over the last ten years to produce outstanding returns.

One of the exciting buzz words among advisors and institutional investors is ESG, which stands for Environmental, Social and Corporate Governance. This subject is almost always granted a wonderful panel reception at any conference our firm attends as it is the topic du jour.

In 1936, John Maynard Keynes penned his work The General Theory of Employment, Interest and Money. Most of the work was trying to strike against the consensus of economics. Many in the intellectual communities of the west believed in the classical theory of economics.

When baby-boomer adults were in their twenties, we sang along with Mark Knopfler and Dire Straits. Their song, “Money for Nothing” defined the era of music videos. We got cable in 1981 and will admit that we were glued to the TV watching music videos of the bands and performers we loved.

Michael Milken rose to the top of Wall Street by way of the Wharton Business School with Drexel Burnham Lambert in tow. Milken’s work at Wharton was founded on the core theory that bond investors were rewarded by taking junk bond risk.

As rates fall to zero in most of the world, the line that has been ringing in our mind is “You can check out any time you like, but you can never leave!” This is a chorus investors have sung through their capital allocations. We believe the Eagles provided an excellent understanding of what today’s market is giving investors in their song, Hotel California.

The stock market has a history of torturing highly-valued knowledge. About every seven years a consensus forms around the fastest growing sector of the stock market, or the fastest growing country, or the fastest growing industry.

For most millennials like myself the last ten years have formed what we believe the business to be: a bull market reinvigorated by the whims of the Federal Reserve Board. If anchoring is a powerful force in investor behavior, the anchor at the depths of our millennial beliefs is that value hasn’t worked.

As I watched this year’s Berkshire Hathaway Annual Meeting, one thing struck me. There was sheer enthusiasm around the annual shareholder meeting for anything tech-oriented. Yes, it was disclosed that Berkshire had taken a position in Amazon that Friday, but it goes deeper.

Late in bull markets there is often a pervasive excitement that arises. At that time, not all profit margins are created equal. Financial euphoria can cause distortions in industries and businesses.

We go through life being taught far more certainty than is actually present. Life isn’t black and white, but instead various shadings of grey that end in black or white, only after the fact.

In the famous book, Strange Case of Dr. Jekyll and Mr. Hyde, Dr. Jekyll and Mr. Hyde were one human being with a split personality. Dr. Jekyll healed people and Mr. Hyde murdered them. This economic environment and the U.S. stock market have the same kind of split personality.

We are revisiting our discussion of what the real world is like versus what academics claim in papers and debates. A good way of putting this is “Academia has a tendency, when unchecked (from lack of skin in the game), to evolve into a ritualistic self-referential publishing game.”

In preparation for a talk, I began to review Sir John Templeton’s track record with the Templeton Growth Fund (TEPLX), which he managed from 1954 to 1991. At the age of 34, with a father that broke into the investment business in 1980, I was very aware of Templeton’s success in his career, but unaware of how the results came to his clients.

The actor, Tom Cruise, is as enigmatic as the U.S. stock market. He has made many terrific movies over the years and today’s stock market reminds us of his classic sports movie, Jerry Maguire. Jerry was a top sports agent for a large agency and then suddenly, out of nowhere, was dumped out on the street with one client and a top college recruit to work with.

In 1720, the South Sea Bubble arose from what seemed to be good intentions. The South Sea Company was given an exclusive monopoly on the Spanish Americas in exchange for assuming a large part of England’s debt. The debt holders received preferred shares in the South Sea Company that paid 6% interest.

For Templeton and Price to execute a “new era” approach today, we believe they would likely advocate avoiding the S&P 500 Index, mutual funds and ETFs, emphasizing growth stock investing and they would be very careful with ownership of anything related to technology. Price recognized that growth eras don’t continue forever and Templeton went wherever he thought he could make great money buying companies at depressed prices with positive economics. We believe our eight criteria for common stock ownership will shepherd us through this “new era.”

In the 1960’s, the slogan “Make Love, Not War” became a rally cry for anti-war protestors, but also typified their free love expression. They used the slogan to explain the harshness of the situation in Vietnam and to be countercultural to the capitalist and traditional way of life they saw in American society.

The patriarch of value investing, Ben Graham, once said, “In the short run the market is a voting machine, but in the long run it is a weighing machine.” His statement is just as profound as the day it was first spoken. However, it is timelessly mystifying to most investors.

Elon Musk is possibly the most interesting man in the world, in our opinion. His nobility comes from his past as a founder of PayPal, but his popularity only grows in this era as he seeks to tackle big projects that include the car business, space, mass transit and other subjects.

I came across a book titled The Matter of the Heart by Tom Morris that is a great history of the medical accomplishments and advances for the human heart. Mr. Morris details eleven operations and their evolutionary success over the course of the book.

A few weeks ago, I caught myself pulled in by an old James Bond classic, The World is Not Enough, starring Pierce Brosnan. In the movie, an oil heiress, Elektra King, is kidnapped. While in captivity, she becomes a victim to Stockholm Syndrome and plots with her captor to destroy an oil pipeline running to the Bosphorus Sea. There is a scene in the movie that encapsulates where we are in today’s stock market environment.

During the most-recent Berkshire Hathaway Shareholder Meeting, Warren Buffett and Charlie Munger reiterated a point during the question and answer portion that has stuck with us. We feel compelled to share what we learned.