There is a great deal to unpack from this week’s press conference by the new chairman of the Federal Reserve, Kevin Warsh. Most striking is his markedly different approach to Fed communications. This was evident not only in the statement accompanying the federal funds rate decision, but also in the abandonment of forward guidance and his reluctance to provide insight into the committee’s internal deliberations.

Even the first line of the press release stood out: “The Federal Open Market Committee approved the following statement for release by a 12–0 vote.” Notably, this unanimity referred only to the release of the statement, not to the policy decision itself. As a result, we are left without visibility into dissent within the committee, including who supported or opposed the policy stance. This represents a meaningful shift in how monetary policy decisions are communicated.

It remains unclear whether this new communication framework will limit Fed members’ ability to express independent views, the practice commonly referred to as “Fed speak.” If those channels remain intact, then such commentary may become the primary way markets gauge the Fed’s policy leanings. For now, however, the degree of openness of Fed speakers is uncertain.

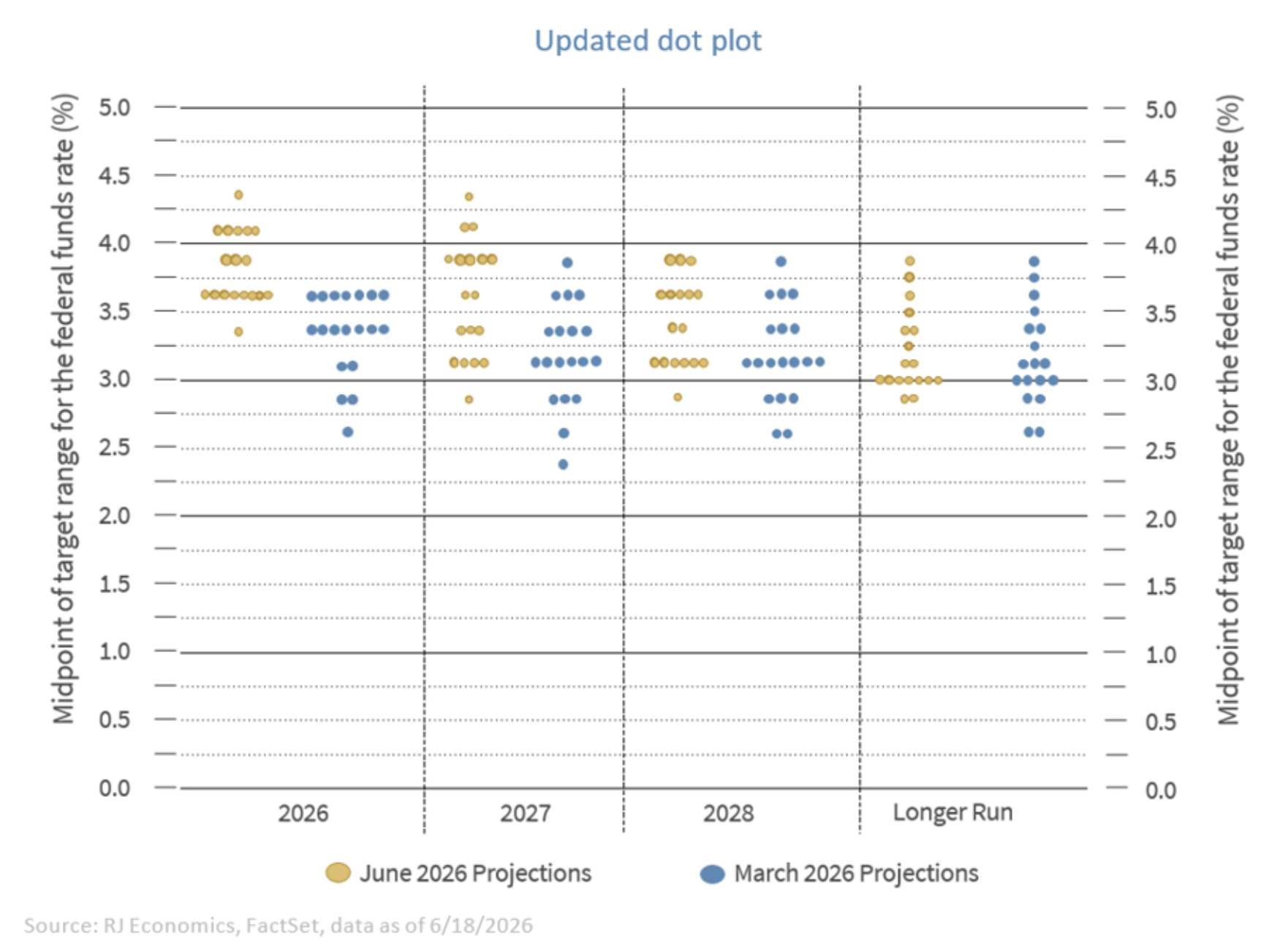

One can reasonably infer that discussions were likely intense and divided, given the more hawkish tone of the dot plot relative to March. Yet the decision to hold rates steady indicates that a majority ultimately aligned around that outcome.

What surprised us most, however, was Chairman Warsh’s assertion that “inflation is a choice.” This is an unusual framing for the head of a central bank. Taken literally, it implies that policymakers knowingly allowed inflation to remain elevated over the past five years rather than bringing it back to target. Such a deterministic view risks oversimplifying the complex forces that drive inflation and, in doing so, raises questions about the Fed’s policy framework.

It is true that the Fed faced criticism for not acting more quickly when inflation began rising in early 2021, likely prolonging the period of elevated price pressures. Still, the chairman’s comment could be interpreted as a veiled critique of prior leadership, including the former chair, board members, and regional presidents, not something you want to do so publicly if you want to lead the institution.

Milton Friedman famously argued that inflation is “always and everywhere a monetary phenomenon,” meaning it can ultimately be controlled through the growth of the money supply. This may be the intellectual foundation behind Warsh’s statement. However, asserting that inflation is a choice suggests that external conditions – such as the global recovery from COVID – were largely irrelevant. That interpretation is difficult to reconcile with reality.

Read more: Embracing Sustainability May Benefit Business

During the pandemic recovery, households accumulated roughly $2.5 trillion in excess savings and subsequently spent a significant portion of it. Preventing that spending surge would have required extraordinarily restrictive interest rates, levels that would likely have been untenable. It is difficult to imagine any credible policy path that could have fully offset that impulse.

Moreover, the inflationary episode of the past several years was not driven primarily by traditional monetary channels. Rather, it reflected an unprecedented fiscal expansion, with the federal government transferring large sums directly to households and businesses. These funds were not intermediated through the banking system in the usual way; they were injected directly into the economy. In this context, standard monetary tools, including a monetarist view, had limited capacity to immediately counteract those forces.

In that sense, inflation is not a “choice” but the outcome of a confluence of factors, including policy decisions – both fiscal and monetary – household and business choices, as well as external shocks. What is a choice is the response: the commitment to bring inflation back toward target once it deviates. That is the essence of the Fed’s inflation mandate and of today’s inflation targeting.

Could the Powell Fed have acted more quickly? Perhaps. But such judgments are easier in hindsight. Policymakers were operating in an environment shaped by the lessons of the Global Financial Crisis, an episode in which insufficient accommodation was seen as a greater risk. That perspective influenced the decision to allow inflation to run somewhat above target before tightening policy. With the benefit of hindsight, that approach proved costly. But it is also clear that policymakers have learned from that experience.

This raises an important inconsistency. If inflation is indeed a choice, and if the Fed has been making the wrong choice for several years, then why did the Warsh Fed refrain from tightening policy at this meeting? One explanation is that the chairman was unable to build a majority in favor of an immediate rate increase. Alternatively, the committee may be buying time as internal reviews of the inflation framework get underway.

There was also little discussion of the Fed’s balance sheet. Chairman Warsh noted that interest rates appear restrictive primarily for the housing sector, a sector that benefited disproportionately from quantitative easing. How this view evolves, particularly if the Fed resumes tightening as suggested by the dot plot, will be important to watch.

In short, there is still much to be unpacked from this meeting in the weeks ahead as well as from Fed speak, it if is allowed to go uncensored. What is already evident, however, is that the internal debate was likely more contentious than the chairman’s remarks suggested.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Raymond James

More Closed End Funds Topics >