Despite strong gains in 2026 so far, commodities have remained supported by constrained supply, resilient demand and long investment lead times, pointing to a cycle that seems to remain fundamentally intact.

The commodity asset class has delivered strong returns so far in 2026, with the Bloomberg Commodity Index climbing more than 25% through the end of May. But for many investors, that raises a familiar question: Have I missed the opportunity?

We don’t think so. Commodity cycles often develop over long periods. They rarely move in a straight line, and rising prices alone don’t typically mark the end of a cycle. More often, they end when supply finally catches up with demand—a process that can take years, and in some cases, a decade or longer.

That distinction matters today. Recent price strength has been supported not only by geopolitical disruptions, but also by persistent supply constraints across several major commodity markets. For investors, the more important question may not be how far prices have already risen, but whether the underlying supply response has meaningfully improved.

Higher prices don’t quickly create new supply

In commodities, the process by which higher prices attract new capital is typically slow. New oil production, refinery capacity, mines, processing facilities, pipelines and transportation infrastructure all require investment, regulatory approvals, equipment and time. Metals projects, for example, can take well over a decade to move from discovery to meaningful production. Higher prices may eventually alleviate shortages, but they rarely solve them immediately. Until new supply arrives, markets often rely on inventories, substitutions or demand destruction.

Current examples are clearly visible across the commodity complex. In energy, oil markets have been roiled by geopolitical shocks, namely the restriction of oil flow through the vitally important Strait of Hormuz. Refined products such as gasoline and diesel remain especially sensitive to refinery outages and shipping disruptions because consumers ultimately depend on refined fuels, not crude oil.

In agriculture, grain markets have felt the knock-on effects of Middle East tensions via fertilizer availability, as the Strait of Hormuz is also a major export corridor for fertilizer shipments. Additionally, food markets remain acutely exposed to weather-related disruptions, especially with a predicted El Niño event expected to persist throughout 2026. Forecasters at the World Meteorological Organization project an 80% probability of a moderate-to-strong El Niño this year, which is typically associated with more extreme weather and rainfall patterns across the Americas. Neither of which contributes to optimal growing conditions.

And in base metals, including copper and aluminum, long-term demand tied to electrification, power grid investment and data center expansion continues to outpace the industry’s ability to bring on new supply quickly.

It’s clear that commodity supplies are not all tight for the same reason. They rarely are. The common thread, however, is that physical supply remains difficult to expand quickly. As a result, commodity prices can remain well supported even after meaningful rallies.

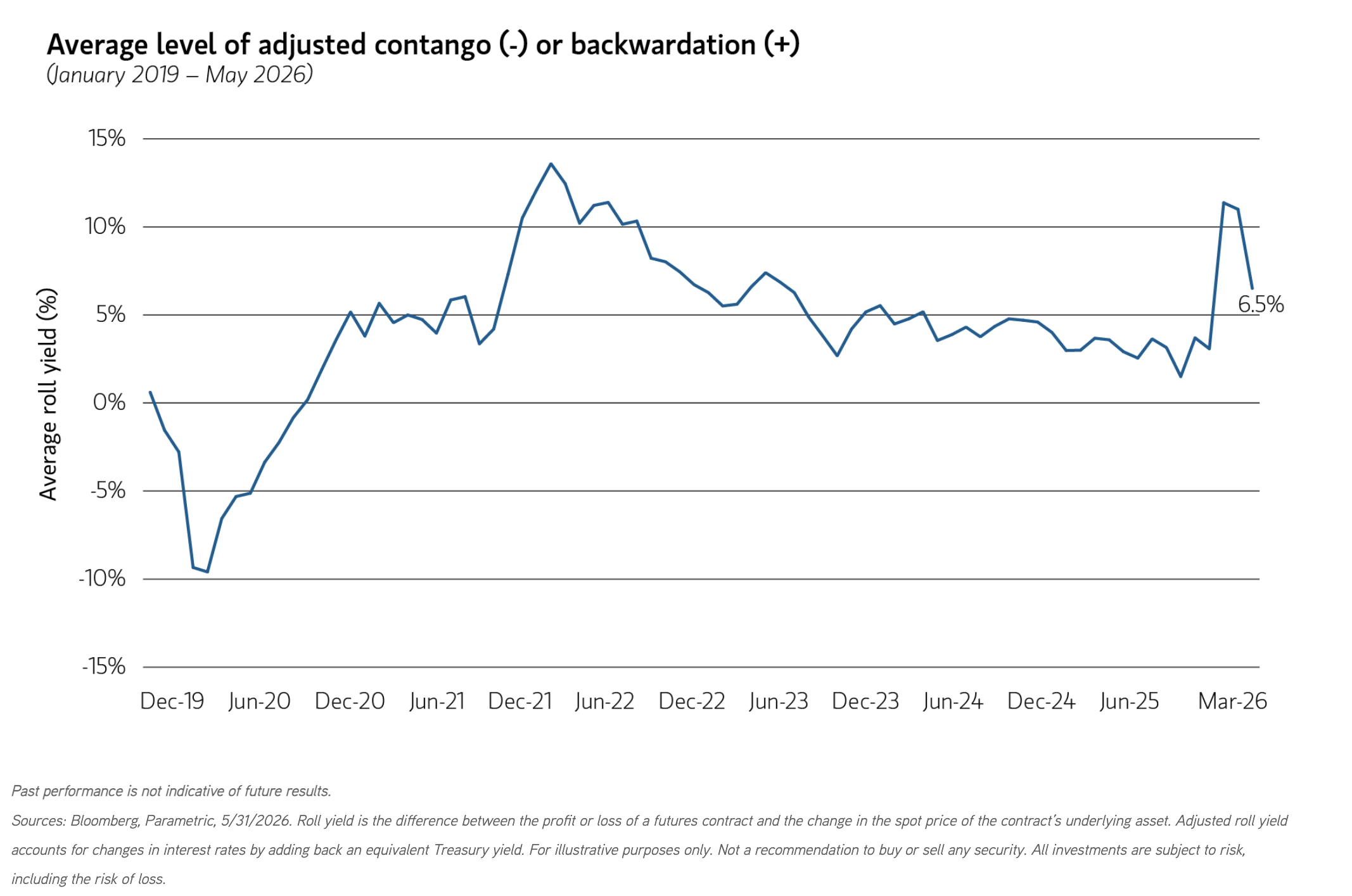

Futures curves are still signaling scarcity

Spot prices tend to capture the headlines, but futures curves can provide a useful read on market fundamentals. When a commodity market is in contango, longer-dated futures prices are above near-term prices. This is essentially the “normal” state of commodity curves that may indicate abundant supply, excess storage capacity and a limited urgency to “buy today.”

In contrast, when longer-dated futures prices are below near-term prices the market is said to be in backwardation. A backwardated commodities market is typically associated with supply deficits, limited storage capacity and a high degree of urgency to buy today. Put simply, backwardation indicates scarcity—buyers are willing to pay a premium for immediate supply. This is the current state of many commodity markets.

Backwardated commodity markets are noteworthy for two primary reasons. First, as discussed earlier, they help confirm that inventories are tight and market participants are concerned about current availability. The energy sector provides a clear example, particularly in crude oil and refined products, where the immediate need for physical supply has kept nearby prices firm. European diesel (also known as gasoil) currently leads the complex, with an adjusted roll yield of +25% as of the end of May.

Second, backwardated markets may produce a positive roll yield for investors in futures-based commodity strategies, as expiring contracts are replaced with lower-priced deferred contracts. While we would argue that commodity selection decisions shouldn’t be based solely on the shape of futures curves, it is worth noting that historical results, on average, have been more favorable during periods of backwardation than contango.

The bottom line

Commodity investors have been rewarded with strong performance recently, and pullbacks should be expected, as with any asset class. Leadership will likely rotate across energy, base metals, agriculture, and precious metals as weather, geopolitics, inventories and growth expectations shift.

But commodity bull markets are often measured in years, not months. Today’s environment remains supported by constrained supply, resilient demand and long investment lead times. That suggests commodities may still deserve investor attention, even after recent price strength.

For many portfolios, the practical takeaway is to avoid making the opportunity dependent on a single commodity call. A diversified allocation may help investors participate in the broader cycle while recognizing that individual commodity markets will move at different speeds, for different reasons and at different times.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

Diversification does not eliminate the risk of loss.

The value of commodity investments will generally be affected by overall market movements and factors specific to a particular industry or commodity, which may include weather, embargoes, tariffs, health, political, international and regulatory developments. Economic events and other events (whether real or perceived) can reduce the demand for commodities, which may reduce market prices and cause their value to fall. The use of derivatives can lead to losses or adverse movements in the price or value of the asset, index, rate, or instrument underlying a derivative due to failure of a counterparty or due to tax or regulatory constraints.

06.24.2028 | RO 5630661

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Parametric

More Commodities Topics >