Private Markets in Retirement Plans: Unlocking Opportunities

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

In August 2025, the US President Donald Trump signed an executive order aimed at broadening the investments available in defined contribution plans (DC plans). On March 30, 2026, the US Department of Labor issued proposed guidance regarding a plan fiduciary’s selection of investments, including private market and other alternative investments, in 401(k) plans.1 US Secretary of the Treasury Scott Bessent commented, “This proposed rule is an initial step in implementing the President's Executive Order in a safe and smart manner, broadening access to additional retirement plan options for millions of Americans while being mindful of the importance of protecting retirement assets.”

The term alternative investments is often used as a catch-all to capture anything that is beyond stocks and bonds. The traditional definition includes private markets—private equity, private credit, private real estate and infrastructure—as well as hedge funds. Some may expand the definition to include cryptocurrencies, non-fungible tokens (NFTs), and other non-traditional investments.

Read more:

The proposed rule is based on the duty of prudence that the Employee Retirement Income Security Act of 1974 (ERISA) imposes on plan fiduciaries when selecting designated investment alternatives (DIAs) for a participant-directed individual account plan (Plan). The proposed rule does not specify which investments are or are not appropriate for fiduciaries to consider but instead outlines the process to be used in selecting investment options. The rule also includes a process-based safe harbor that identifies a non-exhaustive list of six factors to be used in evaluating investments by fiduciaries: performance, fees, liquidity, valuation, benchmarks and complexity.

Why does this matter?

Institutions and family offices have long recognized the value of including private markets for decades. Private markets have historically provided an illiquidity premium relative to their public-markets equivalents,2 attractive risk-adjusted returns, and diversification benefits.

Private Markets Have Historically Delivered Attractive Risk-Adjusted Returns

Exhibit 1: Historical Performance vs. Risk

10 Years Ending December 31, 2025

Private credit has historically provided higher income than most fixed income options, and real estate and infrastructure have historically exhibited low-to-negative correlation to traditional investments. Private markets are versatile tools that can provide increased growth and income, diversification benefits and can help in hedging the impact of inflation.

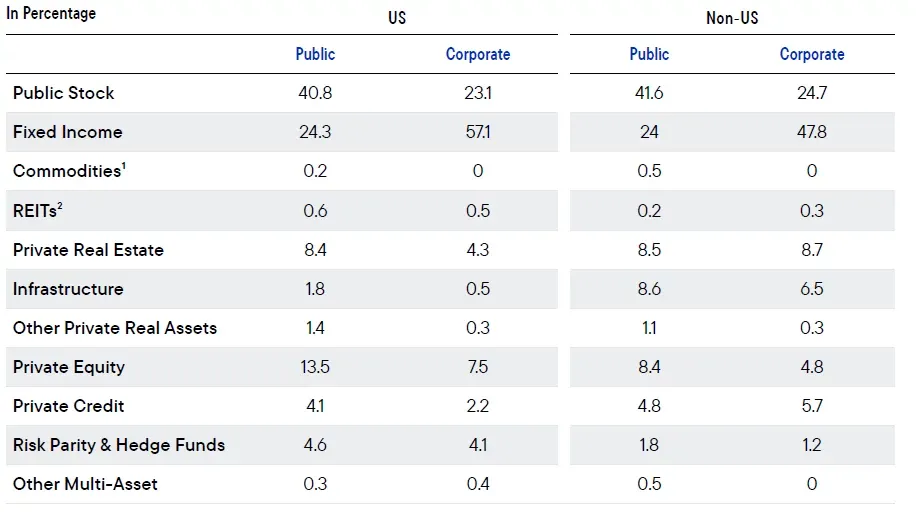

Based on research conducted by DCALTA,3 defined benefit plans (DB plans) have significant allocations to alternatives broadly, with roughly 30% to private markets. Of course, DB plans have had access to these investments for decades and often have sophisticated investment committees and/or consultants to conduct due diligence, develop strategic asset allocations, and monitor the results over time.

DB plans and other institutions have long recognized the growing opportunity set in the private markets and the narrower set of options in the public markets. In addition to the attractive risk-adjusted returns above, the size of the US public market is roughly half its count from two decades ago (down from about 8,000 companies in 1996 to about 4,000 companies in 2025),4 while the number of US private companies has been on the rise. According to a Hamilton Lane report, of all US companies with at least US$100 million in revenue, 87% are private,5 representing approximately 20,000 companies.

Similarly, while some investors may feel like they have adequate exposure to real estate via publicly traded real estate investment trusts (REITs), the lion’s share of the assets are in private real estate (more than 90%). Also, it is worth noting that publicly traded REITs are more highly correlated to equities than private real estate equity.6

Exhibit 2: Average Allocations in Defined Benefit Plans by Segment (As of 2024)

The DCALTA report notes that DC plans have less than a 1% allocation to private markets. This is due to a number of factors including lack of access, lack of experience with private markets, product structure, liquidity, and fiduciary concerns and litigation risks, among others. Note, although evergreen funds offer daily valuations, the underlying investments are illiquid and should be viewed as long-term investments.

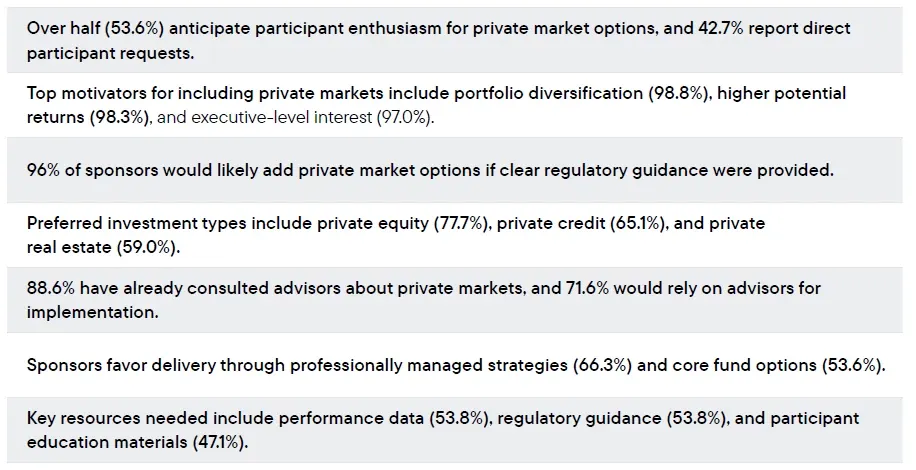

According to a Franklin Templeton, Harris Poll survey, there is growing demand from sponsors to include private markets in DC plans.7

Exhibit 3: What Does the Research Show?

Franklin Templeton Survey of Plan Sponsors

What are the challenges?

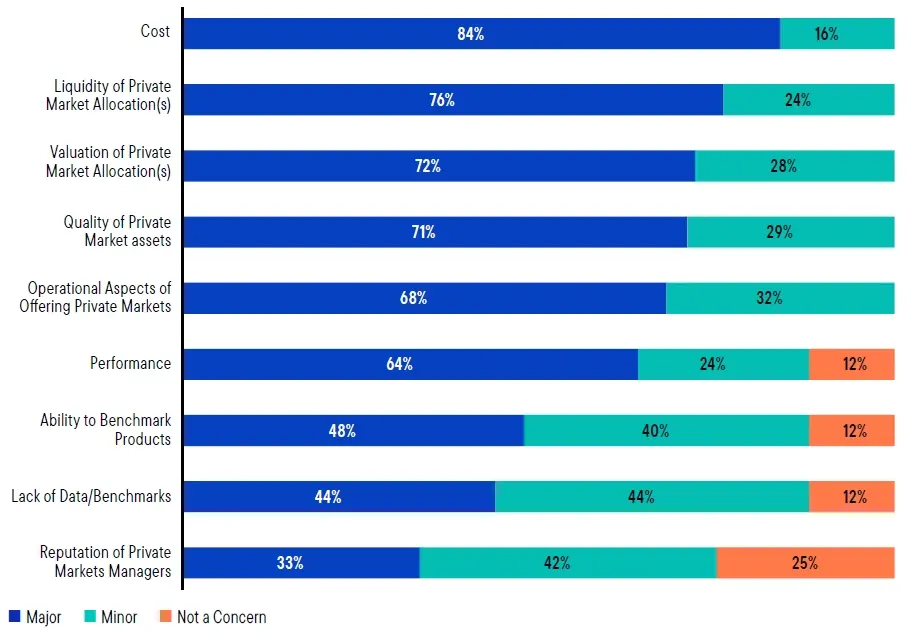

While DB plans have allocated significant capital for decades, these investments have not been broadly available in DC plans. According to research by Cerulli Associates, and the Defined Contribution Alternatives Association (DCALTA), “Unlocking the Potential of Private Investments in Defined Contribution Plans”, there are a number of challenges to incorporating private markets in DC plans.8 Similar to the proposed rule, the report notes challenges including liquidity, valuations, benchmarking, and performance.

The fees for private market funds are typically higher than those of traditional mutual funds, and may include multiple layers (i.e., management and performance fees). Proposed US Department of Labor (DOL) guidelines do not stipulate that a plan fiduciary select the lowest-cost investment option. Instead, the proposed guidelines focus on whether fees are appropriate, considering risk-adjusted return and any other value the investment would provide. In other words, the DOL recognizes that a plan fiduciary isn’t obligated to select the lowest fee and expense option; this is important for private markets, where the lowest-cost option may not be the best one.

Exhibit 4: There Are Natural Concerns about Introducing Private Markets in DC Plans

DC Consultants: Concerns about Private Markets in DC (2025)

![]()

As an industry, we will need to educate all stakeholders about the merits of private markets, their illiquid nature, and their long-term value in DC plans. Each fund will need to be transparent about their costs, valuation methodology, historical performance, benchmarking and underlying holdings.

We believe the broader ecosystem of plan sponsors, asset managers, recordkeepers and third-party providers can address these challenges. The Cerulli/DCALTA report notes that target-date-funds (TDFs) are the preferred vehicle for DC plans.9 Within TDFs, there is a growing acceptance that collective investment trusts (CITs) are effective structures in managing liquidity and rebalancing.

TDFs offer broad diversification, professional management and liquidity management. One of the biggest challenges with incorporating private markets in DC plans is dealing with liquidity management and the reallocation of capital. The CIT structure allows for more effective liquidity management. CITs can maintain a liquidity sleeve to help solve the challenges and move capital more efficiently.

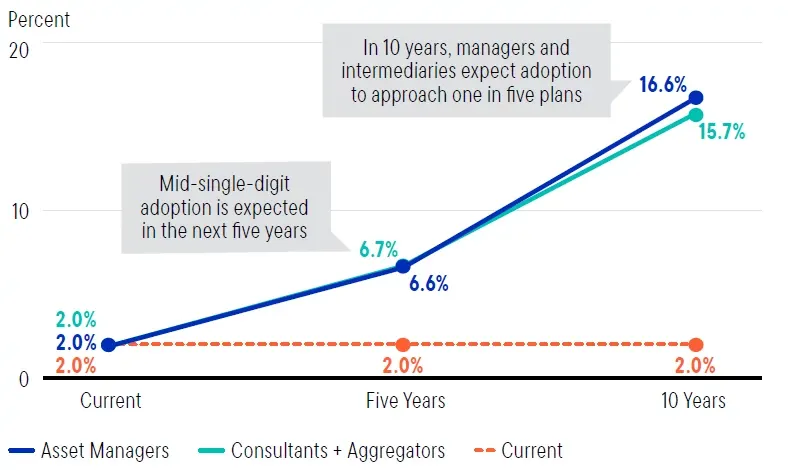

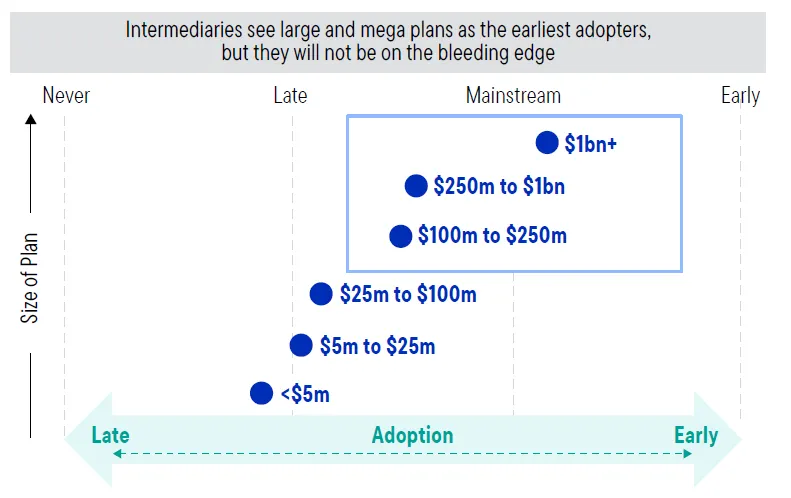

Exhibit 5: Planned Growth and Adoption of Private Markets in DC Plans

Asset managers + intermediaries: % of plan sponsor adopting private market solutions, 2025

DC consultants + advisors: Market segment adoption of private markets, 2025

As we consider the broader adoption of private markets in DC plans, we can leverage the experience of DB plans in allocating capital to private markets. This will likely be a gradual process as key stakeholders get comfortable with the investment merits, operational nuances, and the most appropriate investment options. Larger plans will likely take the lead in adopting these versatile investments, with meaningful adoption accelerating over the next decade.

Why now?

We believe that there has been a confluence of events over the last several years that will fuel the growth and adoption of private markets in DC plans. As we were reminded in 2022,10 the markets have become much more interconnected over the last couple of decades, and investors need better tools for diversification. In fact, correlations across traditional investments have risen over the past couple of decades.

Fortunately, we have seen product evolution that has helped provide access to a broader group of investors, while offering more flexible features. Evergreen funds are now generally available to investors at lower minimums, and with more flexible liquidity provisions. Note, the underlying investments are illiquid, but there are liquidity provisions for unforeseen changes in client circumstances.

Lastly, we now have access to institutional-quality managers. Many of these managers were initially reticent to offer funds in the wealth and retirement channels due to concerns about investors’ ability to stay patient during periods of volatility. However, these new hybrid structures (evergreen funds) allow the managers to invest capital for the long run, while maintaining a small liquidity sleeve to meet redemption requests.

The timing of the proposed DOL guidance for DC plan investments aligns with the evolution of private markets, which became much more accessible in the wealth channel and saw an acceleration in advisor adoption. Trusted advisors can help educate investors about the merits of these valuable tools, their unique nuances and the role they can play in client portfolios. Advisors can help investors with both their personal and retirement portfolios as we as an industry rethink retirement to better serve individual investors.

To learn more about private markets in retirement plans, please visit www.ftprivatemarkets.com and Expanding access to private markets in DC plans. To learn more about the expanding opportunities in private markets, subscribe to the Alternative Allocations podcast series Alternative Allocations Podcast.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnotes

1Source: “US Department of Labor proposes landmark rule to democratize access to alternative investments in 401(k) plans.” US Department of Labor. March 30, 2026. Release Number: 26-560-NAT.

2Source: Davidow, Tony. “The Cost of Being Too Liquid.” May 2026.

3Source: DCALTA and CEM Benchmarking Report. September 2025.

4Sources: US Census Bureau, World Bank, Macrobond. As of December 31, 2025.

5Sources: “Private Market Investing: Staying Private Longer Leads to Opportunity.” Hamilton Lane. April 14, 2022. “The Truth Revealed: The private markets universe is less concentrated and larger today than any other time in history” Hamilton Lane. March 08, 2023.

6Based on 10-year correlation as of December 31, 2025. Sources: SPDJI, NCREIF, FTSE, Macrobond, Analysis by Franklin Templeton Institute. Indexes used: US Equities: S&P 500 Index; Private Real Estate Equity: NCREIF Fund Index Open End Diversified Core Equity (ODCE) Index; REITs: FTSE Nareit All Equity REITs Index. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results. Important data provider notices and terms available at www.franklintempletondatasources.com.

7Source: The Harris Poll on behalf of Franklin Templeton. 2026.

8Source: “Unlocking the Potential of Private Investments in Defined Contribution Plans.” Cerulli Associates and DCALTA. September 2025.

9Ibid.

10Source: Davidow, Tony. “Building Better Portfolios with Private Markets: Rethinking Retirement.” 2024.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Past performance does not guarantee future results.

Investments in alternative strategies may be exposed to potentially significant fluctuations in value.

Investment strategies involving private markets (including investments in private companies and/or securities) are complex and speculative, entail significant risk, should not be considered a complete investment program, and are suitable only for persons who can afford to lose their entire investment. Such strategies may have limited liquidity in both the investment products and their underlying investments. Underlying investments may never list on a securities exchange and lack available information due to their private nature. These factors may negatively impact such investments’ market value and a manager’s ability to dispose of them at a favorable time or price. Additionally, certain investment fund types mentioned are inherently illiquid and suitable only for investors who can bear the risks associated with the limited liquidity of such funds. Such funds may only provide limited liquidity through quarterly repurchase offers that may be suspended at the discretion of the manager or the fund’s board. There is no guarantee these repurchases will occur as scheduled, or at all. Shareholders may not be able to sell their shares in the fund at all or at a favorable price.

The allocation of assets among different strategies, asset classes and investments may not prove beneficial or produce the desired results.

Investments in underlying funds are subject to the same risks as, and indirectly bear the fees and expenses of, the underlying funds.

Diversification does not guarantee a profit or protect against a loss.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Companies in the infrastructure industry may be subject to a variety of factors, including high interest costs, high degrees of leverage, effects of economic slowdowns, increased competition, and impact resulting from government and regulatory policies and practices.

Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits