After more than three years of underperformance, our prognosis for global health care stocks remains positive. The sector now offers a broader set of high-quality companies at valuations that appear increasingly disconnected from fair value.

We see six drivers that may lead to a turnaround in health care stocks.

1. Companies are changing how they do business.

Many health care companies are updating their business models. For example, some companies are moving away from complicated pricing systems to simpler, more upfront pricing. Others are focusing on faster-growing areas and leaving slower ones. These changes make companies easier to understand and help them grow more steadily in the future.

2. Artificial intelligence (AI)I is helping companies work faster and grow.

AI is becoming very important in health care. It helps companies run clinical trials, manage data and improve operations. In medical technology, AI is also being used in tools like surgical robots to improve results and efficiency.

3. Companies are working to increase profits.

Health care companies are trying to improve their profits in different ways. They are handling more patients, cutting costs, improving pricing and making manufacturing more efficient. Many are also using technology and AI to save time and money.

4. Demand for health care is strong.

Even though many investors are not very excited about the sector right now, demand for health care services remains steady or is growing. Hospitals have been seeing more patients, and companies in life sciences have seen strong demand for their services. Overall, people continue to need health care regardless of economic conditions.

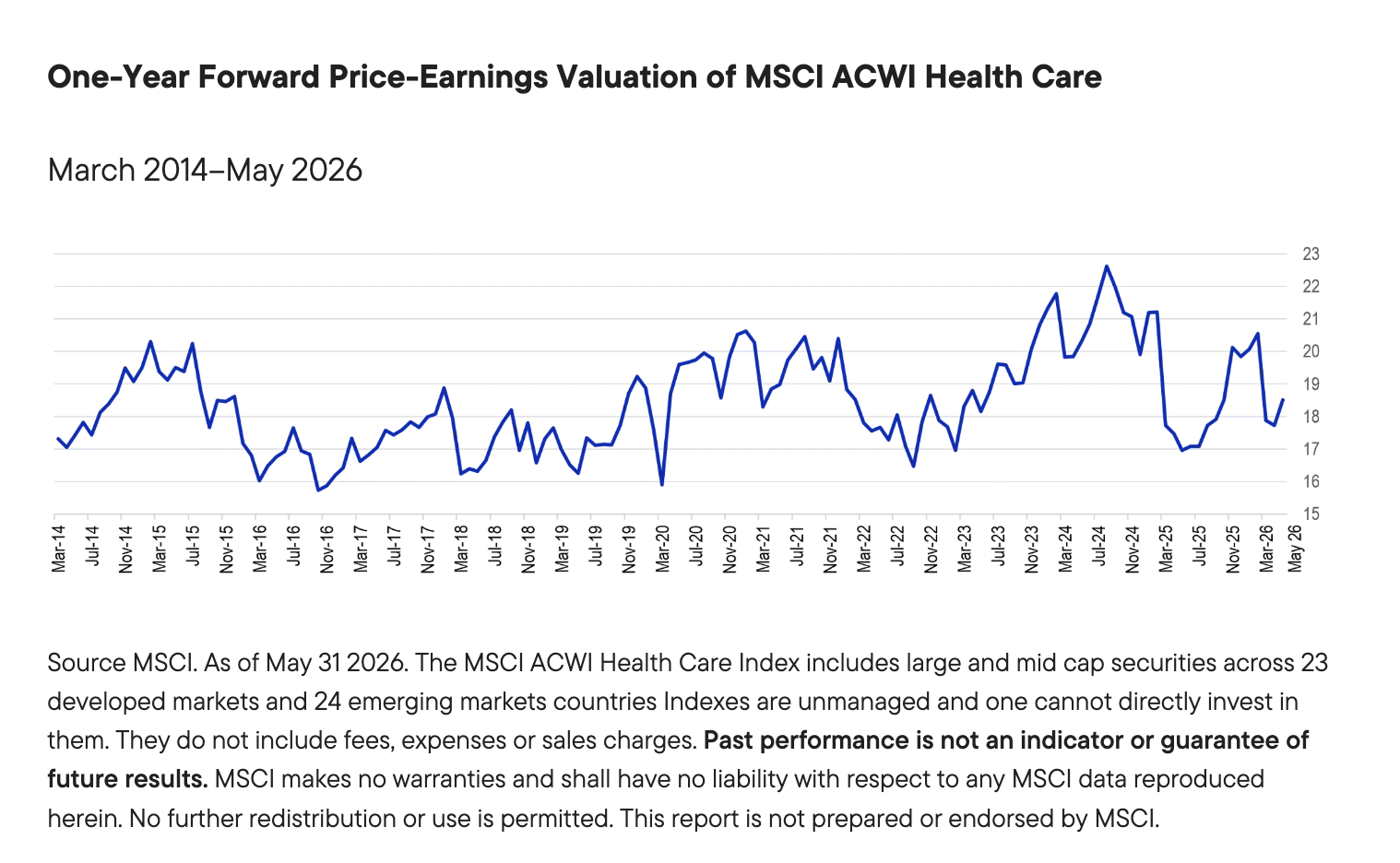

5. Stocks are cheaper than they should be.

Many investors have been putting money into technology stocks, especially those related to AI, instead of health care. As a result, health care stocks are now priced lower, even though the companies are still performing well. This could make them a good buying opportunity.

6. Companies are buying back their own stock.

Many health care companies are using their extra cash to buy back their own shares. This can increase the value of the remaining shares. Some companies are doing this because they believe their stock is undervalued.

A Long-term approach to better portfolio health

We believe the key to health care investing is to stay patient and selective. We maintain our focus on companies with the defensive growth characteristics that can anchor portfolio resilience over the long term. Among our holdings are companies with strong free cash flows and cost discipline, as well as competitive advantages and product leadership over their peers.

In pharmaceuticals, we favor companies with strong product pipelines that may have become underappreciated. We also favor devices companies that can execute their business strategies well and protect or restore their margins amid tariffs.

At a broader level, we believe the sector provides a good proxy to aging populations, rising health care spending and the advancement of bio-medical technologies. This long-term view will continue to frame our perspective as the market cycle turns and macro conditions evolve.

Market review

Global equities advanced in May, extending the rebound from April, although the path higher was uneven. Market direction was shaped primarily by shifting expectations around US-Iran talks and the status of the Strait of Hormuz. Periods of optimism that a deal could be reached, or that shipping flows might normalize, pushed oil prices lower and supported risk appetite, while setbacks in negotiations and renewed blockade rhetoric briefly revived concerns around inflation and growth. Against that backdrop, regional performance diverged, with equity markets in the United States and Asia Pacific outperforming Europe.

Outlook

The AI theme continues to drive our outlook for global equity markets. US hyperscalers are planning to invest almost US$700 million this year. Estimates for next year are as high as US$1 trillion.

In the United States, we expect strong demand for AI to continue in the coming years. Nevertheless, we acknowledge the risk of overinvestment. European equities remain shaped by the US-Iran conflict and hopes of a peace deal. Energy prices are the main risk for Europe. Emerging market equities offer many opportunities, including those related to domestic demand and AI. Taiwan and South Korea play key roles in the supply of AI chips. They are benefiting from strong demand for advanced chips and memory products.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments.

Equity securities are subject to price fluctuation and possible loss of principal.

The investment style may become out of favor, which may have a negative impact on performance.

To the extent the portfolio invests in a concentration of certain securities, regions or industries, it is subject to increased volatility.

Large-capitalization companies may fall out of favor with investors based on market and economic conditions. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

WF: 10933258

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Franklin Templeton

More Innovative ETFs Topics >