Key takeaways:

- Despite geopolitical uncertainty, rate volatility and sector‑specific stress, the spreads on securitised investments have remained orderly, supported by diversification, short duration and structural protections.

- Securitised credit typically benefits from broad underlying loan diversification and floating‑rate structures, helping to limit performance drawdowns and reduce sensitivity to rate moves, compared with other areas of credit.

- While fundamentals remain broadly sound, dispersion across sectors and structures highlights the importance of bottom‑up analysis, active risk management and disciplined underwriting.

Looking through geopolitical noise

Securitised credit markets have navigated a volatile start to the year with resilience. Against a backdrop of heightened geopolitical uncertainty, shifting interest rate expectations and idiosyncratic stress, repricing in securitised spreads has remained orderly, underpinned by strong investor demand and supportive technicals.

Read more: The Gulf May Need New Vision

Amid such volatility, the defining benefits of securitised investments, namely diversification, structural protection and active risk management, come to the fore. Securitised investments tend to be driven less by geopolitical shocks and more by underlying consumer and collateral performance. That distinction has recently helped limit drawdowns and dampen volatility in securitised credit, in contrast to the larger gyrations experienced by broader risk markets.

Software exposure: Manageable, not systemic

This breadth of exposure has helped insulate portfolios from sharp drawdowns in individual sectors, including recent weakness seen in parts of the software market. Across Europe, we estimate approximately 10% of the investable collateralised loan obligation (CLO) universe has some form of software exposure. Crucially, only around 4% sits within the sub-sectors that have generated the most concern.1

This differentiation matters. CLO managers – who actively manage the loan pool – are not indiscriminately exposed to a single theme; rather, exposures vary meaningfully by strategy and mandate. Active engagement with managers has highlighted clear frameworks around what they own, why they own it, and how they seek to manage downside risk. In aggregate, software exposure has proven manageable.

Data centres: Structural demand from AI supercycle, defensive cashflows

In terms of opportunity from AI, data centres are emerging as a distinctive and increasingly relevant exposure within securitised markets. Demand is rising, underpinned by long‑term structural drivers, including cloud adoption, AI workloads and enterprise digitisation, rather than short‑cycle economic growth. For securitised investors, these assets are characterised by long 10–15-year contractual lease terms, high tenant quality and well-defined cashflow visibility, often extending beyond the shorter tenor of the bonds themselves.

Risk profiles also differ meaningfully from traditional real estate. Operating risk is typically limited, with tenants bearing the non-operational risk of energy, equipment and fit‑out costs, while lease structures embed strong protections, in terms of break optionality. In Europe, issuance remains relatively scarce and skewed towards higher‑quality sponsors and assets. Data centres offer attractive relative value and potential income stability, with the defensive high-quality bias that characterises securitised investments.

Orderly repricing underpinned by strong technicals

Market technicals entered 2026 on a solid footing, which was evident in February, at the time of the Structured Finance Association’s (SFA) conference in Las Vegas. While spreads widened, the moves were modest and orderly. Since then, issuance has slowed, allowing supply and demand to rebalance, with spreads largely reverting to pre-SFA levels, underscoring the market’s ability to absorb volatility without disruption.

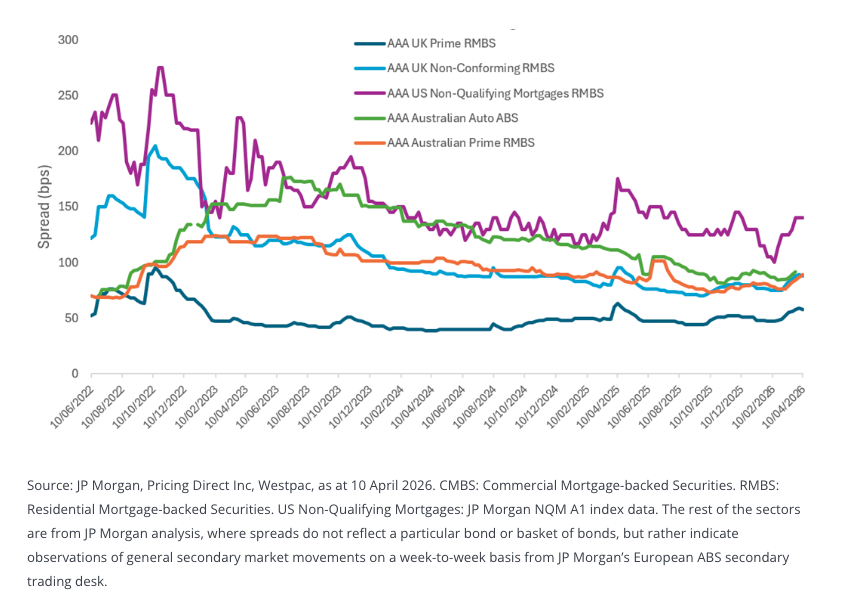

Importantly, the adjustment since late January has been measured rather than disruptive, and materially smaller than the volatility spike seen following Liberation Day. This repricing reflects both technical factors and a reassessment of risk, rather than a deterioration in underlying fundamentals. One illustration is the mortgages market, where demand was supported by policy direction for Fannie Mae and Freddie Mac to purchase up to US$200 billion of Agency Mortgage‑Backed Securities (MBS). This also lifted US non-qualifying mortgage spreads through 2026 given their correlation with agency MBS, while it is perceived this activity would lower mortgage rates and boost housing affordability. It also highlights the resilience of securitised collateral pools, which we tackle next.

Figure 1: Securitised spreads adjust in an orderly fashion despite renewed volatility

Resilient collateral pools

On the consumer side, much of the rates-related stress in 2022-2023 (as shown in Figure 1) has now washed through. Higher rates, inflation and house price adjustments prompted originators to tighten underwriting standards and rein in riskier lending. That discipline has transpired in the quality and performance of collateral pools, particularly in more recently originated transactions. Recent events in the Middle East raise concerns about a resurgence of inflation, however consumer lending is now in a relatively stronger position than the previous cycle.

While some segments, such as UK buy‑to‑let mortgages, show slightly higher arrears, performance remains within expectations, even at subordinate levels. In CLOs, rising CCC buckets over the past two to three years reflect pressure from higher floating rate costs, but absolute levels remain in low to mid‑single digits.in percentage terms. Structural protections continue to provide meaningful buffers across the capital stack. Around 65% of a typical securitised deal is rated AAA,2 offering high-quality debt that is also short dated.

Floating rate structures and duration protection

Another meaningful advantage then is that much of securitised universe is issued at the short-end, with spread durations – the sensitivity of an investment to the movement of spreads – of three to five years. Coupled with floating rate characteristics, this may help securitised portfolios avoid the duration‑driven losses seen elsewhere in some areas of the fixed income market.

With heightened selling activity earlier in 2026 now normalising, market conditions have stabilised. In the current environment, where the path of future rates is uncertain and inflation remains a risk, exacerbated by geopolitics, floating‑rate exposure offers a resilient income profile and reduced duration risk, reinforcing the role of the asset class within diversified portfolios.

Securitised investments also continue to benefit from attractive carry, driven by their floating‑rate structure and the steady pass‑through of higher reference rates. While moves in base interest rates are not an immediate driver of returns, the impact builds through daily compounding, supporting income over time. Price performance is therefore more closely linked to spread dynamics than interest rate volatility.

Volatility that is easier to stomach

A key distinction between securitised credit and the leveraged loan market (the building blocks of CLOs) has been the nature of volatility. Sudden price moves of several points in individual loans can be difficult for investors to digest as it can materially impact performance. However, diversified CLO portfolios can absorb those idiosyncratic loan price movements without materially impacting the overall credit quality, particularly for investment-grade-rated tranches. This means that the resulting price impact on those CLO tranches can be far less.

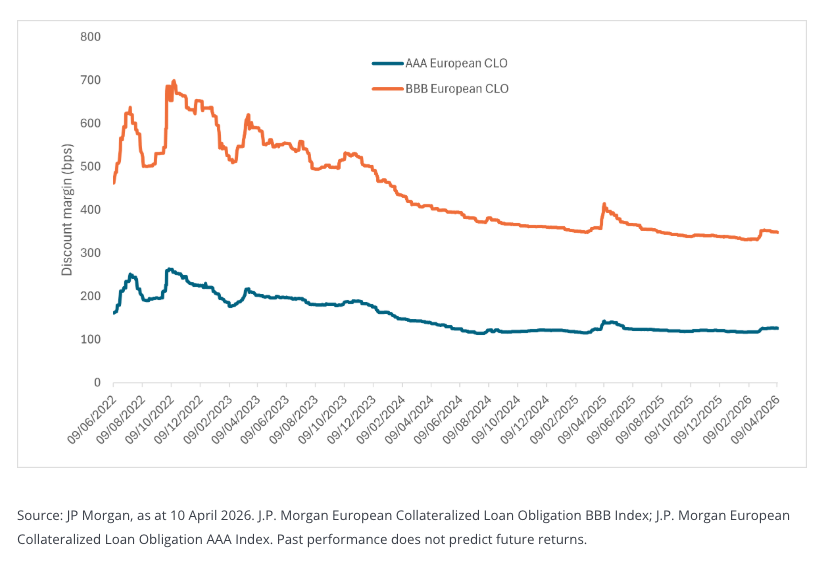

This relative stability has reinforced the reality that securitised investments exhibit less volatility than sometimes assumed. As an example of this, the stability of CLO spreads can be seen through the recent market volatility (Figure 2). Crucially, this stability is not solely due to the structure of securitisations. Active management plays an important role in smoothing performance across different market environments.

Figure 2: Stability in CLO spreads through the recent market volatility

Through disciplined credit selection, ongoing surveillance of underlying collateral and proactive trading, CLO managers can address emerging risks early, rebalance exposures and potentially preserve downside protection.

Solvency II reforms are unlocking insurer demand for securitised credit

Recent reforms to Europe’s Solvency II framework are materially lowering capital charges for selected securitised investments, making areas such as CLOs, commercial and parts of residential mortgage-backed securities far more accessible to European insurers.

This shift is already translating into growing interest from the insurance sector, broadening the institutional buyer base and supporting market depth. Over time, these regulatory changes could play a meaningful role in sustaining and strengthening European securitised credit markets as insurers reassess how and where they allocate capital.

Securitised credit: A resilient role within portfolios

Taken together, recent market dynamics reinforce the case for securitised credit as a resilient and adaptable allocation in uncertain times, with an increasingly globalised opportunity set emerging. Orderly repricing, robust collateral performance and strong technicals highlight an asset class driven less by headline risk and more by fundamentals.

In an environment where uncertainty around growth, inflation and policy remains elevated, securitised credit continues to offer a combination of stability, income and risk control that is increasingly difficult to replicate elsewhere. For investors seeking income, diversification and defensiveness within fixed income portfolios, we believe that securitised credit continues to stand out as a compelling allocation.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

IMPORTANT INFORMATION

Actively managed portfolios may fail to produce the intended results. No investment strategy can ensure a profit or eliminate the risk of loss.

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Bank loans often involve borrowers with low credit ratings whose financial conditions are troubled or uncertain, including companies that are highly leveraged or in bankruptcy proceedings.

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Fixed income securities are subject to interest rate, inflation, credit and default risk. As interest rates rise, bond prices usually fall, and vice versa. High-yield bonds, or “junk” bonds, involve a greater risk of default and price volatility. Foreign securities, including sovereign debt, are subject to currency fluctuations, political and economic uncertainty and increased volatility and lower liquidity, all of which are magnified in emerging markets.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

The opinions and views expressed are as of the date published and are subject to change. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Janus Henderson® and any other trademarks used herein are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.

© Janus Henderson Investors

More Leveraged and Inverse Funds Topics >