Congressional confirmation hearings tend to generate far more noise than signal, and this one was no exception. Between politicians posturing for the cameras in hopes of becoming their party’s next rising star, and nominees exercising extreme caution to avoid missteps under oath, these hearings rarely produce actionable insights. Still, there were a few elements worth salvaging from the appearance of Federal Reserve (Fed) chair nominee Kevin Warsh that help clarify his guiding principles.

Those signals come from three main sources. Some are rooted in his prior tenure as a Fed governor, others stem from his long-standing public criticism of how the Fed has operated over the past several decades, and the rest reflect our interpretation of what he appears to view as the appropriate communication strategy for the Fed going forward.

Based on his testimony, it is clear that Warsh is a monetary policy traditionalist, although that was hardly a revelation. He places primary faith in the federal funds rate as the central tool of monetary policy, rather than in the newer instruments developed during and after the Great Financial Crisis. What is notable, however, is that many of these unconventional tools were introduced while he was serving on the Federal Reserve Board, where he emerged as one of Chairman Ben Bernanke’s most influential advisers. Warsh ultimately resigned in 2011, arguing that the Fed should have curtailed the use of these measures once the crisis environment had passed.

Since their introduction, these nontraditional tools have been criticized for blurring the line between monetary and fiscal policy. The expansion of the Fed’s balance sheet through purchases of mortgage-backed securities, asset-backed securities and US Treasuries, along with various interventions designed to prevent financial markets from seizing up, effectively shifted the central bank into areas traditionally associated with fiscal authorities. These programs also had the side effect of insulating investors from losses and supporting asset prices over time.

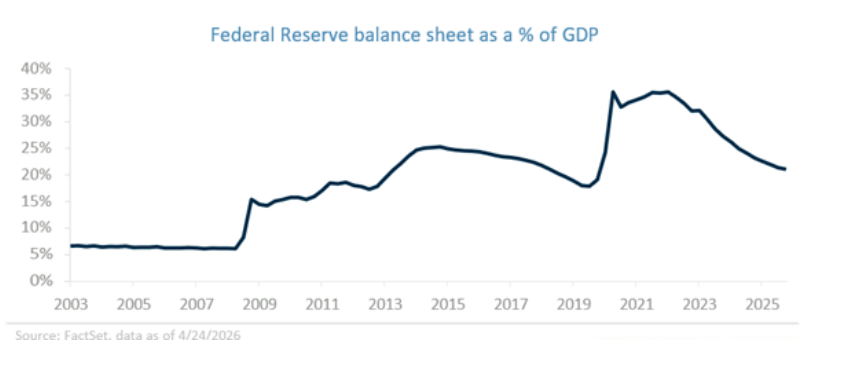

The graph above illustrates the evolution of the Fed’s balance sheet as a percentage of GDP since 2003, highlighting just how dramatic this shift has been. While quantitative easing is the most visible example of balance-sheet expansion, it was only one part of a much broader policy framework. The Fed also deployed a wide range of liquidity facilities, including the Term Auction Facility, the Primary Dealer Credit Facility and the Term Securities Lending Facility. It supported short-term funding markets through programs such as the Commercial Paper Funding Facility and the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility, and it intervened directly in credit markets through initiatives like the Term Asset-Backed Securities Loan Facility. Together, these measures fundamentally altered the scope of central banking in the United States.

Read more: A Pivotal Time for the Federal Reserve

As noted earlier, many of these programs produced an additional, often underappreciated outcome: They helped sustain asset prices. Housing values, equity markets and a broad range of financial instruments benefited from the implicit backstop provided by the Fed’s expanding toolkit. This has fueled the argument that these policies disproportionately benefited the investor class and amplified wealth gains for households with real estate and financial assets, relative to those without such exposures.

We share some of these concerns, which are evident in today’s K-shaped economy, where a relatively small share of households account for nearly half of personal consumption expenditures. At the same time, unwinding these monetary policy instruments, especially abruptly, could carry significant consequences for the broader US economy. The challenge lies in balancing legitimate distributional concerns against the risk of destabilizing financial markets and economic activity.

Another point that stood out in Warsh’s comments was his apparent discomfort with the Fed’s current communication strategy, particularly the dot plot. His remarks suggested that he views Fed officials as speaking too frequently and too loosely, potentially complicating policy rather than clarifying it.

Criticism of the dot plot is not new and has surfaced from within the Fed itself. Some policymakers have emphasized that it is not intended to be a forecast of the federal funds rate, but rather a snapshot of individual participants’ views at a moment in time. Nevertheless, financial markets have increasingly treated the dot plot as an implicit forecast, which can create false precision and, in some cases, misaligned expectations about the future policy path.

If confirmed, we would not be surprised to see Warsh eliminate the dot plot from the Summary of Economic Projections (SEP). He may even go further by reconsidering the SEP altogether, signaling a decisive shift away from the current transparency framework and toward a more restrained approach to central bank communication.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

© 2026 Raymond James Financial, Inc. All rights reserved.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition - September 2025 (PDF)

© Raymond James

Read more commentaries by Raymond James