Hedged Equity vs. Bonds: Seeking A More Reliable Diversifier for Modern Portfolios

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhy the 60/40 Portfolio Doesn’t Always Diversify

“Diversification” has been the driving principle of investing and risk management for generations. But what does it mean to be “diversified?”

Merriam-Webster defines “diversified” as “composed of distinct or unlike elements or qualities.” When investing, shorthand for “diversified” is usually a portfolio consisting of 60% US large cap stocks and 40% investment grade bonds, represented by the S&P 500 index and the Bloomberg U.S. Aggregate bond index, respectively.

It is fair to ask- is the 60/40 portfolio really “diversified?” Are U.S. large cap stocks and investment-grade bonds distinct? Do they have “unlike elements or qualities”?

One could argue that yes, equities and bonds are distinctly different investment securities with different return expectations, risks, and claims upon a company’s cash flows. From this perspective, stocks and bonds are obviously different.

However, from a portfolio construction perspective, the answer to the stock-bond diversification question is “sometimes.” Sometimes stocks and bonds behave differently. Sometimes they behave similarly, to the benefit of the investor. Sometimes they behave similarly, to the detriment of the investor.

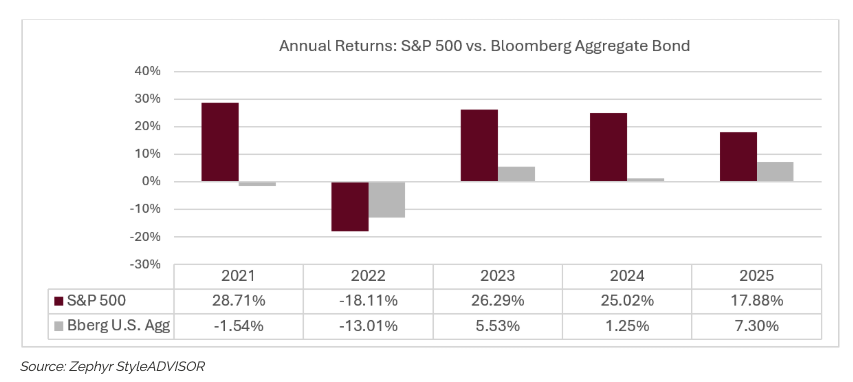

The graph above illustrates these different environments.

- In 2021 the S&P 500 had a fantastic year, up 28.7%. Bonds had a down year, losing -1.5%; clearly these two asset classes behaved differently.

- In 2025 both the S&P 500 and the Bloomberg Agg posted positive returns. An investor in the 60/40, or any combination of the two, would probably have been pleased with the results. But it’s harder to say this portfolio was “diversified” in 2025.

- However, 2022 represents a year when diversification’s benefits failed to materialize. Stocks and bonds both had double-digit losses, so it follows that the 60/40 or any other combination of these two assets would also have double-digit losses.

Stock-Bond Correlation: Why Diversification Is Only “Sometimes” Reliable

What is behind these numbers? Why is the answer to the stock-bond diversification question “sometimes” and not “always?”

The answer involves the economic conditions or market events that drive asset pricing. Some events lead investors to favor stocks over bonds, or vice versa. However, some events will have a positive or negative impact on stocks and bonds simultaneously. In these scenarios, a simple stock-bond portfolio isn’t diversified.

A prime example of a macro factor having a simultaneous impact on stocks and bonds is interest rates. Rising interest rates are generally negative for both stocks and bonds, so that is why 2022 was a bad year for both. Conversely, falling interest rates in 2025 provided a tailwind for both asset classes.

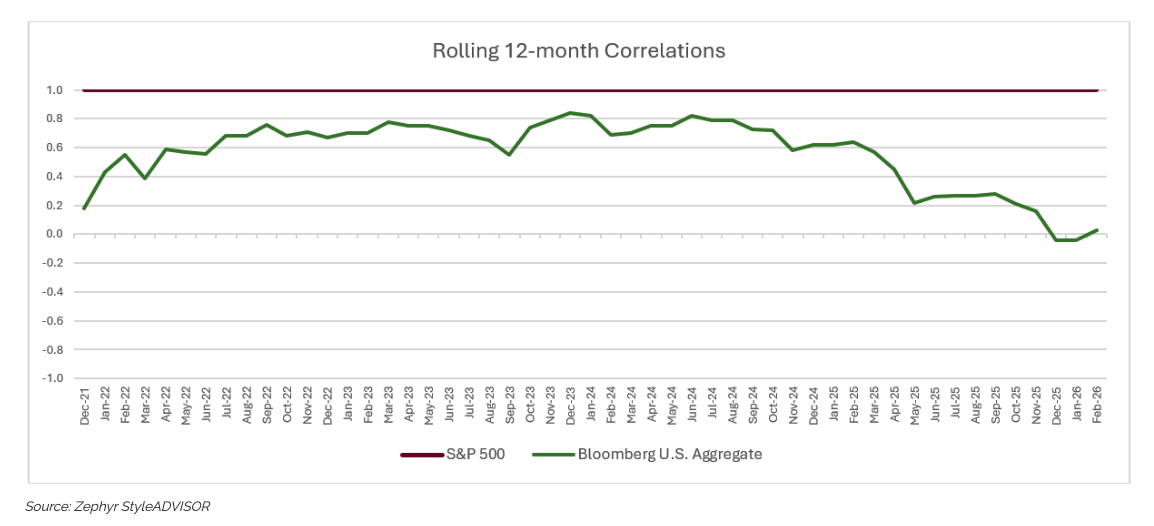

The benefits of diversification are measured by “correlation.” Correlation measures how closely two asset classes are related. The lower the correlation number, the more differentiation there is between two investments, and the lower the overall risk. The higher the correlation, the more the two investments move in lock-step. High correlations are good when both investments are up, but are detrimental when both asset classes are down– creating a correlation conundrum.

The above chart shows the “sometimes” nature of the correlation benefits between stocks and bonds. Sometimes bonds have a lower correlation to stocks, bringing diversification and risk reduction benefits to the investors. Sometimes the correlations between the two are high, and the portfolio isn’t diversified.

How Put Options Provide “Always-On” Diversification — Unlike Bonds

Most investors seek risk reduction when diversifying their portfolios. But in environments like 2022, when stocks and bonds fell in tandem they are left wondering, “what happened?”

How can investors achieve the goal of diversification and risk reduction if the correlations between stocks and bonds are unreliable?

Swan Global Investments believes that put options offer better diversification and risk reduction characteristics than bonds. Since 1997, Swan has managed hedged equity solutions utilizing put options and following the motto “Always Invested, Always Hedged.”

The Swan Hedged Equity US Large Cap ETF (ticker: HEGD) is the latest iteration of Swan’s Defined Risk Strategy. The “Always Invested” portion of the ETF is invested in S&P 500-based ETFs, similar to the stock portion of the traditional 60 stock/40 bond portfolio. However, rather than investing in bonds for diversification and risk reduction, Swan is “Always Hedged” using put options to fill that role.

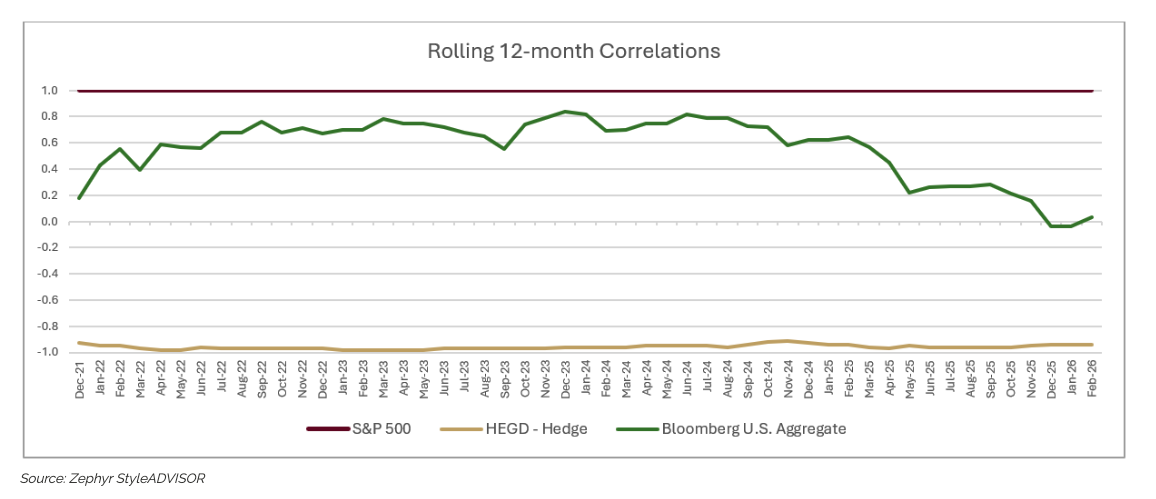

Rather than being “sometimes” uncorrelated with stocks, put options have always had strong negative correlations with the underlying stock or stock index. The chart below shows the strong negative correlations Swan’s put option hedges have historically had vs. the S&P 500 (a correlation of -1.0 is the maximum mathematically possible).

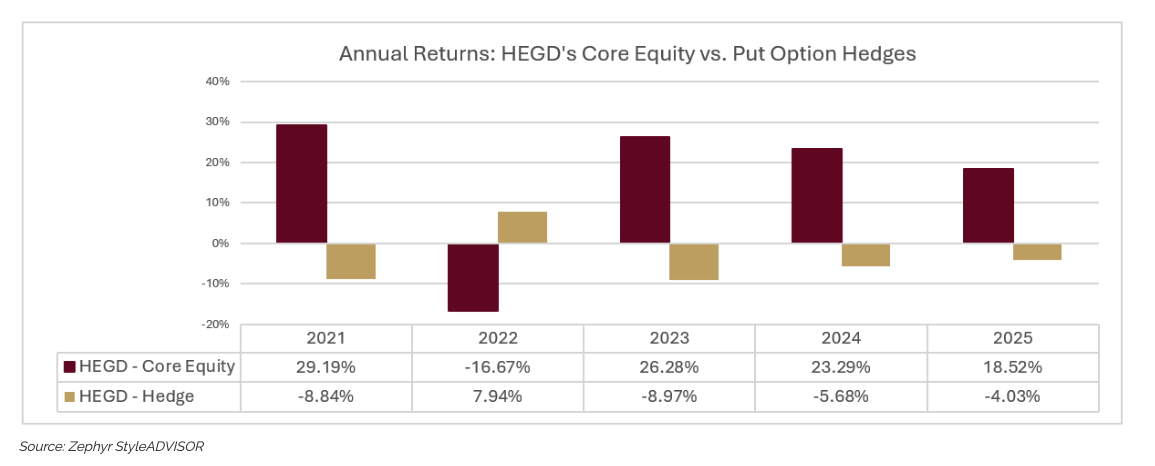

The correlation benefits are clearly evidenced in the year-by-year returns of HEGD. Historically speaking, the returns of the two legs of HEGD (equity and hedge) have moved in opposite directions- precisely the goal of a truly diversified portfolio.

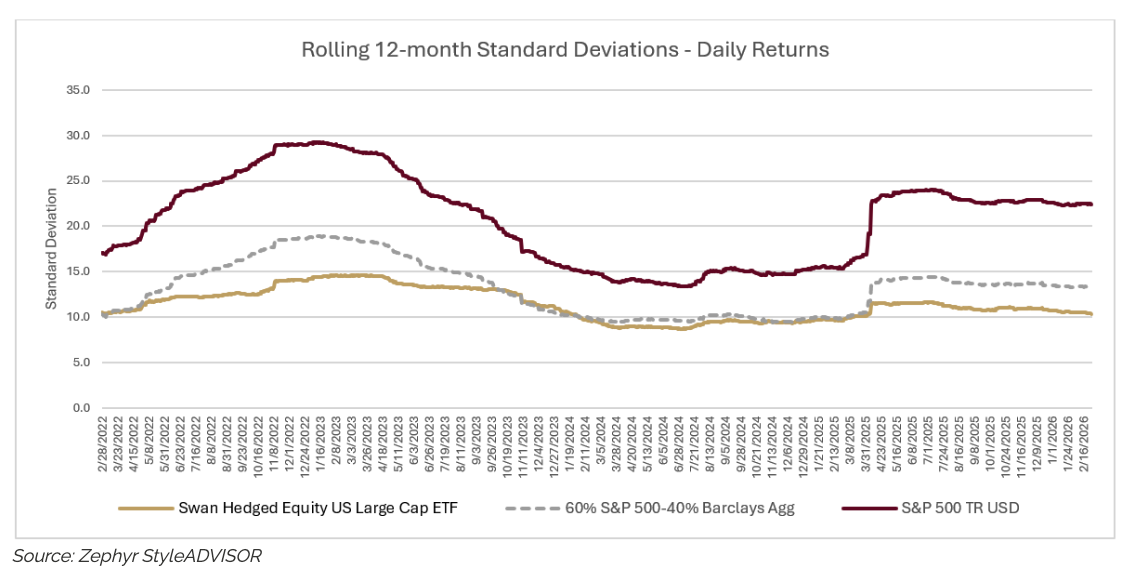

When correlations are favorable, the risk of an overall portfolio can be reduced. This insight inspired Harry Markowitz to develop Modern Portfolio Theory in 1952, which shaped investing for generations. Volatility risk, measured by standard deviation, can be reduced.

The graph below shows how the volatility risk or standard deviation of the S&P 500 has been reduced by diversifying into bonds in a 60/40 portfolio.

In addition, the above graph also shows that HEGD’s use of put options has historically reduced the volatility of the S&P 500 even more than bonds. This is because put options on the S&P 500 always have negatively correlated returns, whereas bonds’ correlation benefits are only “sometimes.”

Adding a Hedged Equity ETF to a 60/40 Portfolio: Efficient Frontier Analysis

There are multiple ways to measure risk. Volatility is one way, but many clients are more concerned about capital preservation – i.e. “not losing money.”

Put options have historically been used to hedge a portfolio because the further the underlying asset (like the S&P 500) falls the more valuable a put option becomes.

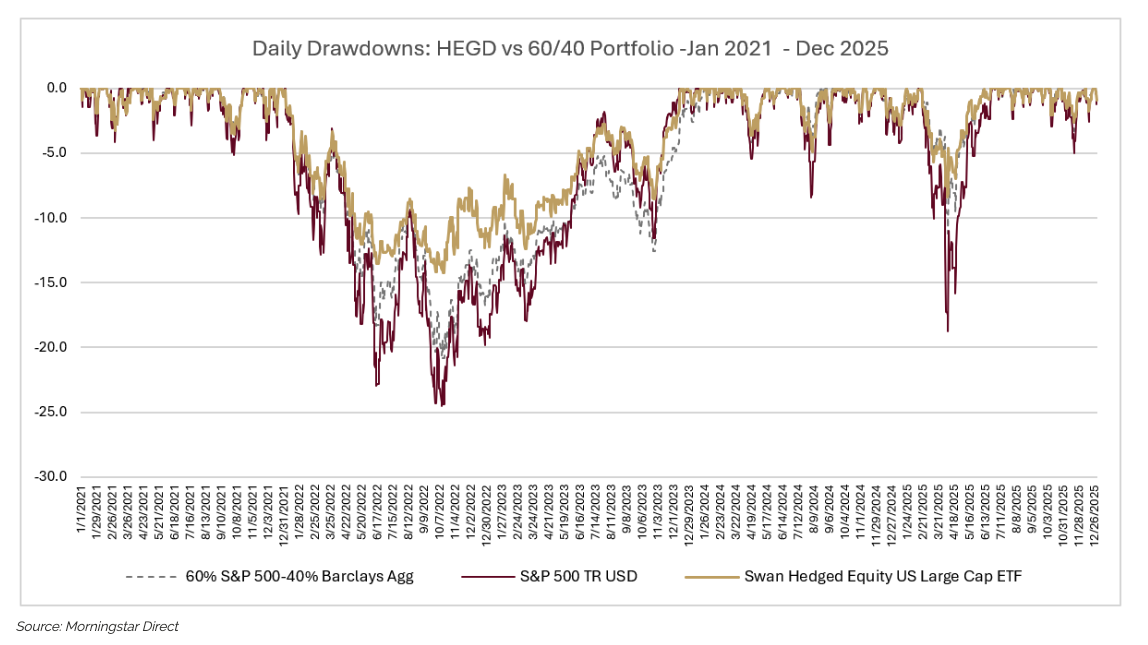

The graph below shows the historical drawdowns of the S&P 500 Total Return Index and compares them to the traditional 60/40 portfolio (60% S&P 500 TR Index / 40% BBg US Agg Index) and HEGD.

The 60/40 portfolio uses bonds as a diversifier against the stock holdings, but in years like 2022 bonds and stocks fell simultaneously due to rising interest rates. Conversely, notice how HEGD’s put options did a better job of offsetting losses, regardless of what interest rates were doing.

That said, it may not be prudent for bond investors to completely abandon all their bond positions for HEGD.

Moreover, we recognize many investors hold stocks and bond in proportions different than the standard 60/40 mix, such as 40/60, 50/50, 70/30, etc.

However, given HEGD’s favorable risk and return characteristics, it can be used as an effective diversifier to any blended stock/bond portfolio.

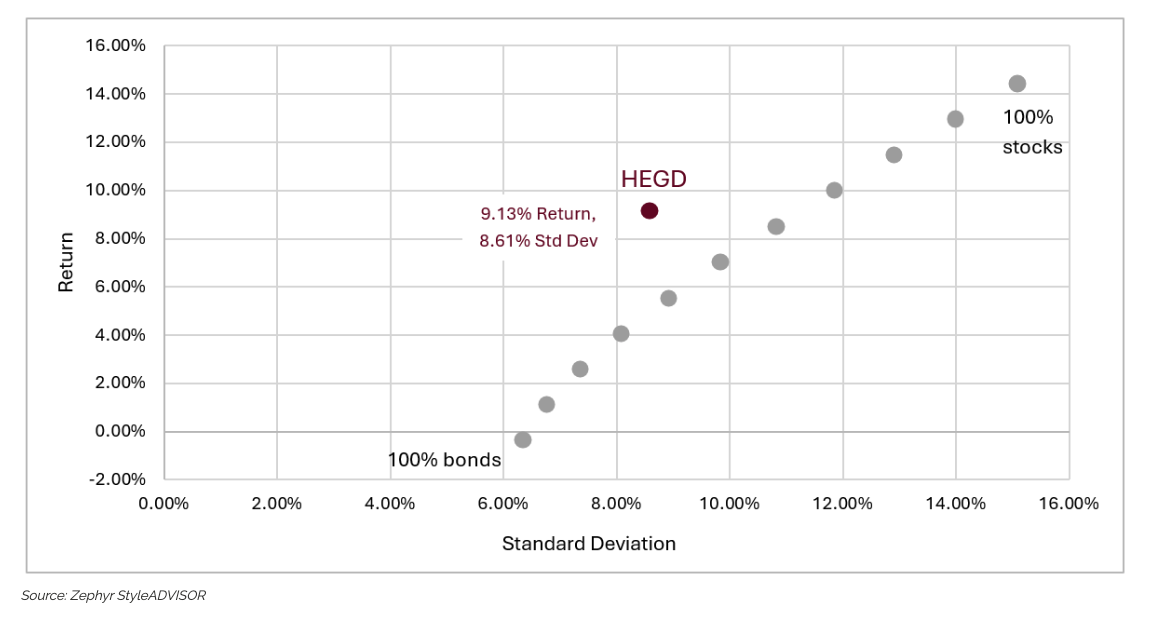

The following graph is referred to as an “efficient frontier.” The graph plots the historical return on the vertical y-axis against risk, typically measured by standard deviation, on the horizontal x-axis of a given set of combinations of investments.

The line of grey dots represents the historical return and risk levels for portfolios consisting of different combinations of stocks and bonds, each in 10% interval variations.

- The dot with the lowest return and the lowest risk is 100% bonds.

- Each successive dot increases the stock allocation by 10% and decreases bonds by 10%

- The dot with the highest return and risk is 100% stocks.

- The red dot shows the historical return and risk of HEGD.

This graph above clearly illustrates that an investor could have improved returns and/or decreased risk by incorporating HEGD into a standard stock-bond portfolio.

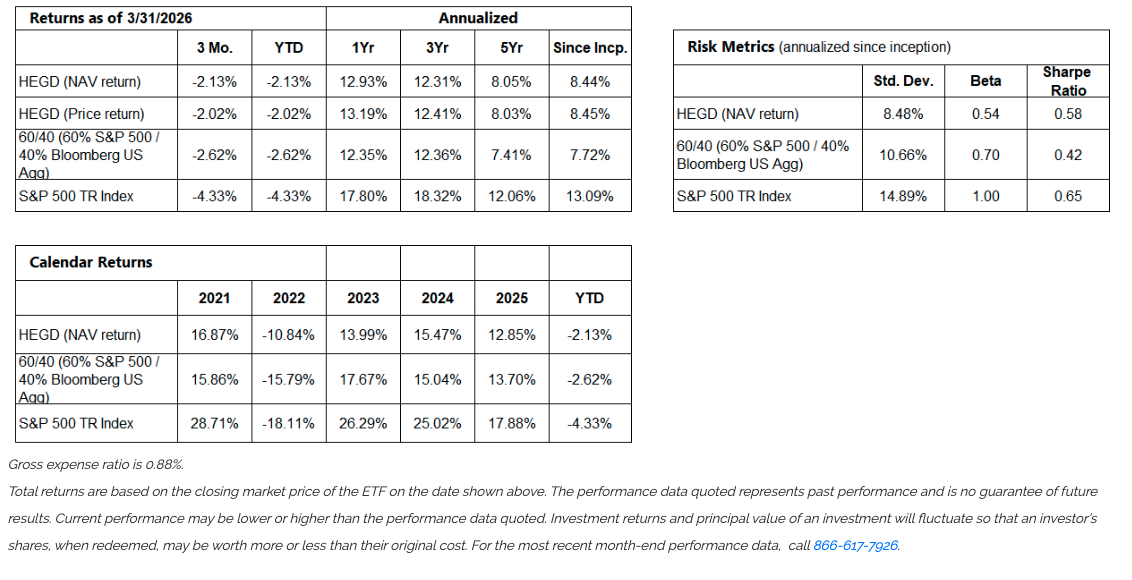

HEGD – Performance Overview: Here are standard return and risk tables for a more complete view of performance.

Key Takeaways:

Bonds Offer “Sometimes” Diversification.

Put Options Offer “Always.”

Diversification is a worthy goal, but how you diversify makes all the difference in the world. The key is to obtain diversifiers that offer real risk mitigation by moving in independently, and ideally in opposite directions (the essence of diversification).

- Bonds offer ‘sometimes’ diversification.

- Put options offer ‘always’ diversification.

- That difference is what HEGD is built on.

If you are concerned about the level of risk mitigation in your portfolio—if it is truly diversified—or whether 2022 could happen again, HEGD is worth a closer look.

The hedge in HEGD is built in and always there—a true diversifier that doesn’t depend on interest rates or credit worthiness of bond issuers. And it’s been running on a process that’s time-tested since 1997.

Learn more about HEGD here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Disclosures:

Investors should carefully consider the investment objective, risks, charges and expenses of Exchange-Traded Funds. This and other information is contained in the prospectus and should be read carefully before investing. To obtain a prospectus for the Swan Hedged Equity U.S. Large Cap ETF (ticker: HEGD) containing this and other important information, please call (855) 772-8488, or visit etfs.swanglobalinvestments.com.

The fund’s investment objective is to seek long term capital appreciation while mitigating overall market risk.

An investment in the fund involves risk, including possible loss of principal.

Exchange Traded Funds and Mutual Funds involve risk, including possible loss of principal. There is no guarantee the Fund will meet its objective. The fund will use put and call options, which are referred to as “derivative” instruments since their values are based on, or derived from, an underlying reference asset, such as an index. Derivatives can be volatile, and a small investment in a derivative can have a large impact on the performance of the Fund as derivatives can result in losses in excess of the amount invested. Options used by the Fund to reduce volatility and generate returns may not perform as intended. There can be no assurance that the Fund’s option strategy will be effective. It may expose the Fund to losses, e.g., option premiums, to which it would not have otherwise been exposed. Further, the option strategy may not fully protect the Fund against declines in the value of its portfolio securities. The prices of options may change rapidly over time and do not necessarily move in tandem with the price of the underlying securities. Selling call options reduces the Fund’s ability to profit from increases in the value of the Fund’s equity portfolio, and purchasing put options may result in the Fund’s loss of premiums paid in the event that the put options expire unexercised. To the extent that the Fund reduces its put option holdings relative to the number of call options sold by the Fund, the Fund’s ability to mitigate losses in the event of a market decline will be reduced. The Fund is non‐diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

Shares of any ETF are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

Swan Global Investments is an SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (DRS). Please note that registration of the Advisor does not imply a certain level of skill or training. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be no assurance that future performance will be comparable to past performance. This communication is informational only and is not a solicitation or investment advice. Further information may be obtained by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com.

The Swan Hedged Equity U.S. Large Cap ETF (HEGD) is distributed by Foreside Fund Services, LLC, member FINRA / SIPC. Foreside Fund Services, LLC and Swan Capital Management, LLC & Swan Global Investments, LLC are not Foreside Fund affiliated. There is no guarantee the funds will meet their investment objectives. Past performance does not guarantee future results. SCML-914081-2026-04-09

Glossary of Terms

Options: An option is a contract that gives the buyer the right to either buy (in the case of a call option) or sell (in the case of a put option) an underlying asset at a predetermined price by a specific date. Options are a powerful tool for creating a wide array of potential payoff profiles and may be used on a standalone basis or integrated into a broader portfolio strategy.

Volatility: a statistical measurement of the degree of variability of the return of a security or market index.

Standard Deviation: a measure of the dispersion of a set of data from its mean. The farther apart from the benchmark, the higher the deviation.

60/40 Portfolio: The 60/40 portfolio referred to herein consists of 60% S&P 500 Index, a index of approximately 500 U.S. large cap stocks by market capitalization and 40% Bloomberg US Aggregate Bond Index, a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

1099 Main Avenue | Suite 206 | Durango, CO 81301 | 970.382.8901

Swan Global Investments is a SEC-registered investment advisor providing asset management services utilizing the Swan Defined Risk Strategy, allowing our clients to grow wealth while protecting capital. Please note that registration of the Advisor does not imply a certain level of skill or training. Swan Global Investments, LLC is affiliated with Swan Capital Management, LLC, Swan Global Management, LLC and Swan Wealth Advisors, LLC. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance.

Downloadable ADVs and Privacy Policy.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All