The investment environment has changed significantly since our January Cyclical Outlook, “Compounding Opportunity.” The conflict in the Middle East has disrupted oil production and transportation, causing financial markets to reprice the expected paths for growth, inflation, and central bank policy. In private credit markets, risks that were largely hidden from view – including illiquidity and opaque pricing – have moved to the front of investors’ minds. As AI continues to fuel an investment boom, it is also disrupting industries. Some of these shocks will have shorter-term implications while others appear more enduring.

Economic outlook takeaways

-

Energy shock raises stagflationary risks and deepens disparities

Global growth has been more resilient than expected despite growing divergence below the surface. The Middle East conflict represents a major global energy supply shock that, if sustained, is likely to be stagflationary – pushing inflation higher while weighing on growth. Higher energy prices are sharpening existing divides between winners and losers – and creating new ones – across countries, sectors, businesses, and households.

-

Governments may face a policy paradox

Central banks face a difficult trade-off between rising inflation pressures and slowing growth, with markets already tightening financial conditions on their behalf. We believe central banks are unlikely to match the market’s recent repricing of policy rate expectations. Recession risks have increased, while elevated sovereign debt levels limit the scope for fiscal responses, meaning shocks could transmit more directly to vulnerable households, smaller companies, and credit markets.

-

This is a different environment from 2022

In 2022, the energy shock from the Russia-Ukraine war collided with a post-pandemic economy shaped by pent-up demand, government stimulus, and tight labor markets, amplifying inflation. Today, fiscal policy is tighter, labor markets are looser, and policy rates are already neutral to restrictive, reducing the risk of sustained inflation.

Investment outlook takeaways

-

Seek resilience and quality

Resilient headline growth alongside widening dispersion strengthens the case for high quality fixed income. Investors can use bonds as a hedge against downside risks and active management to navigate divergent outcomes. Starting yields are much higher today than in 2022, providing cushion against inflationary tail scenarios.

-

Treat liquidity like an asset

Within private credit, corporate direct lending remains illiquid and opaque. Investors have an opportunity to rebalance toward liquid and transparent public fixed income at similar yields. Signs of late-cycle credit stress reinforce the need for selectivity, scrutiny of pricing and liquidity terms, and a preference for collateral-backed, higher-quality investments.

-

Stay diversified and selective

We favor leaning into global dispersion with targeted diversification across regions and currencies to further fortify portfolios. Similarly, consider inflation-hedging tools such as commodities and real assets.

Economic outlook: Resilience under strain

Resilient global headline growth has continued masking widening divergence across countries, industries, and households, as AI-fueled investment and wealth have offset tariff-related pressures. What has changed is the addition of a major new source of risk: the conflict in the Middle East. If this proves to be a short-term disruption, as markets are currently pricing, then the baseline outlook still assumes moderate global growth. However, a prolonged disruption would pose more significant challenges and increase global recession risks.

Geopolitical risks tend to transmit to the economy through changes to consumer and business confidence, financial conditions, and – most importantly today – energy prices. The Strait of Hormuz, a critical waterway for oil and energy shipments, remains effectively blocked. Similar to Russia’s invasion of Ukraine in 2022, this threatens to spark a global energy supply shock.

Energy supply shocks are stagflationary

Unlike in 2025, when divergent trends left global growth broadly unchanged, the Middle East conflict is likely to be stagflationary, lifting inflation while hurting growth. We see four main transmission channels:

- Higher energy and food prices

- Disrupted supply chains and trade flows

- Tighter financial conditions

- Lower business and consumer confidence

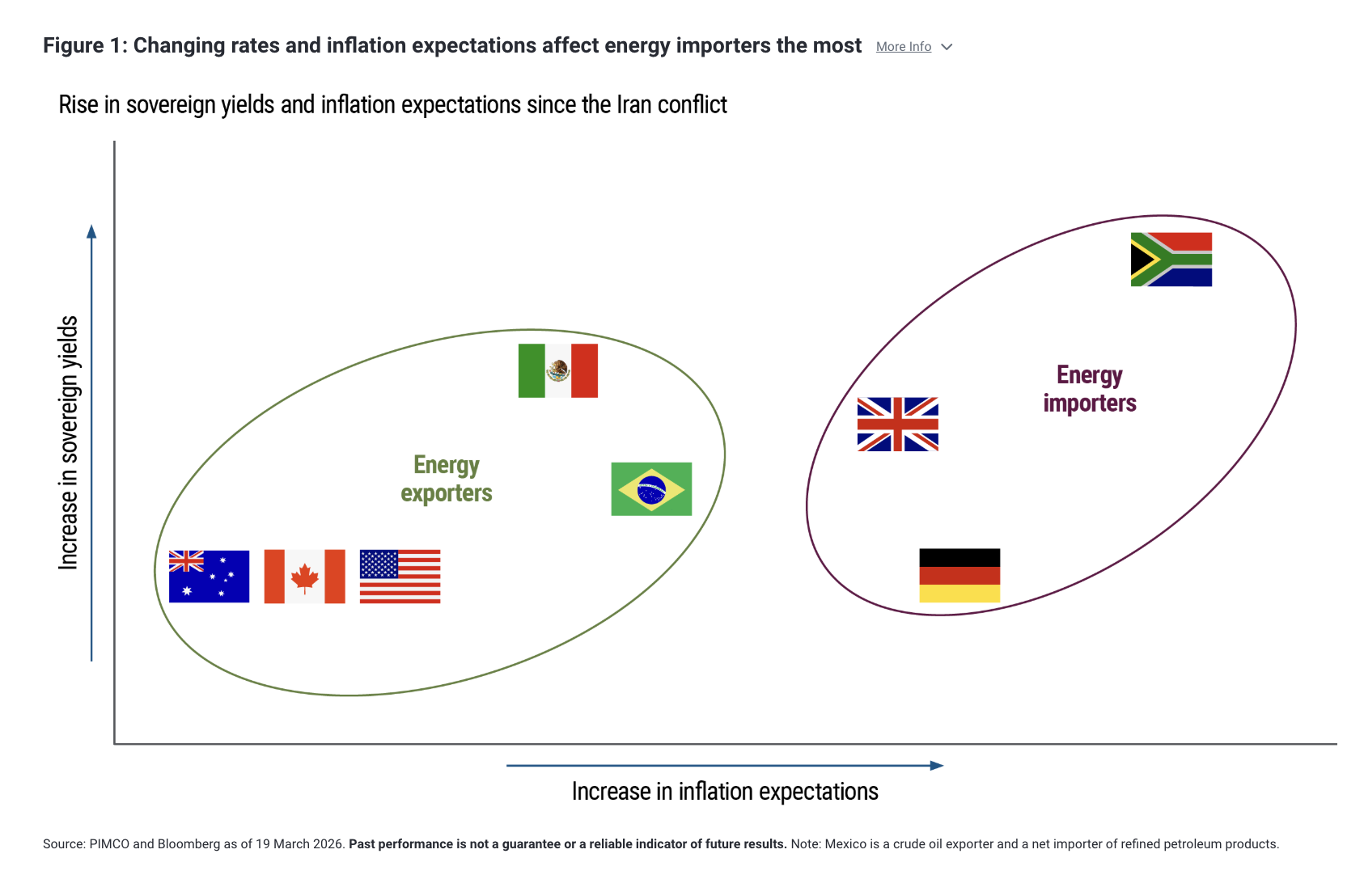

Negative oil supply shocks are inflationary for all economies, while growth effects will differ. Higher energy prices are stagflationary for net oil importers – transferring income abroad through more expensive energy imports while reducing household real (inflation-adjusted) income and business real profit – and expansionary for net oil exporters.

Within developed markets (DM), Europe, the U.K., and Japan are energy importers and face larger downside growth risks. Canada and Australia should benefit from their net energy export status.

Two decades of shale production increases have turned the U.S. from a net energy importer to a slight exporter. However, the U.S. is still a large economy with an energy sector as opposed to a commodity economy. Since energy is an important input into all goods it imports, the U.S. will likely still behave as a net energy importer to some extent.

The U.S. also enters this period with vulnerabilities. The energy shock will exacerbate K-shaped economic trends for households – with potential for a larger pullback in real consumption. Higher energy prices act as a transfer from households (via lower real incomes) to energy companies and their capital owners. Low- and middle-income households, with the highest propensity to consume relative to their real income, will be hurt the most.

Beyond the global drag from lower oil production, indirect effects – confidence and financial conditions – will also likely weigh on growth. Markets have reacted by tightening global financial conditions. The shortest-dated interest rates across DM have shifted toward pricing central bank rate hikes, along with generally higher real yields and lower equity prices.

A prolonged closure of the Strait of Hormuz also risks disruption to Asian manufacturing, the dominant supplier of goods to the rest of the world, which is particularly reliant on Middle East oil. Products across chemical, plastics, autos, electric vehicles, construction materials, and other sectors risk supply disruption, not just higher manufacturing costs.

Central banks face a tug of war – but this isn’t 2022

The risk of higher inflation alongside lower growth puts central banks in a tricky spot. Conventionally, central banks tend to look through supply shocks, especially in economies that are net energy importers. After the elevated post-pandemic inflation period, however, central banks will be closely focused on the risk that a large supply shock could lead to more persistent pressures as inflation expectations and wages also adjust higher.

Yet economies are in much different positions than they were in 2022, when Russia’s invasion of Ukraine sent energy prices soaring and central banks hiked rates aggressively. At that time, the world was still dealing with pandemic-related pent-up demand, and governments had injected trillions of dollars into the private sector. The result was a large demand shock on top of a large supply shock. Labor markets were also extremely tight as the pandemic spurred early retirements and job hiatuses, prompting one of the largest-ever mismatches in labor supply and demand. Across economies, job openings relative to the number of unemployed accelerated, driving both nominal wages and prices higher.

Today, by contrast, fiscal policy is tight across many regions as elevated post-pandemic sovereign debt forces restraint. The global economy doesn’t have a similar stockpile of savings from fiscal transfers. Labor markets are much looser. Monetary policy is already neutral to slightly restrictive across most DM economies. In emerging markets (EM), real rates have remained elevated despite moderating inflation. As a result, economies are much more likely to adjust to the current shock through lower real incomes, weaker nominal wage adjustments, and greater recessionary risks.

In practice, the knee-jerk market reaction toward tighter financial conditions and more hawkish monetary policy is already doing much of the hawkish work for policymakers. In the end, if inflation does prove temporary while downside growth risks materialize, central banks may need to ease more aggressively.

The Bank of England and the European Central Bank have been at the eye of the storm in terms of the repricing of central bank expectations (see Figure 1). But there has been a general move across DM, including the pricing out of the previously expected rate cuts by the Federal Reserve.

Similarly, in EM economies, prospective easing has mostly been priced out – again with greater differentiation between energy importers and exporters. EM central banks will have an even harder task than their DM counterparts in looking through the first-round inflation impacts of the energy shock, but most also started off with a greater real yield buffer owing to elevated policy rates going into the shock.

In the baseline of energy markets moving in line with the forwards, we anticipate significant reverses of the sell-off in front-end rates across DM and EM economies. But in line with the tone of central banks’ commentary at their March meetings, there is a lot of uncertainty in the immediate outlook.

Investment outlook: Repositioning portfolios toward quality and liquidity

This is not an environment set up to reward bold forecasts or narrow bets. Instead, today’s conditions favor more liquid, high quality portfolios built to weather shifts in market sentiment and a range of potential outcomes.

Markets rarely price geopolitical risk well. When there is a global shock, portfolio liquidity can allow investors to take advantage of market inefficiencies and valuation gaps that arise. Similar to the volatility that followed U.S. tariff announcements in April 2025, the rapid repricing of central bank expectations in response to the Middle East conflict has created localized volatility and opportunities to invest against the prevailing narrative.

Treat liquidity as an asset

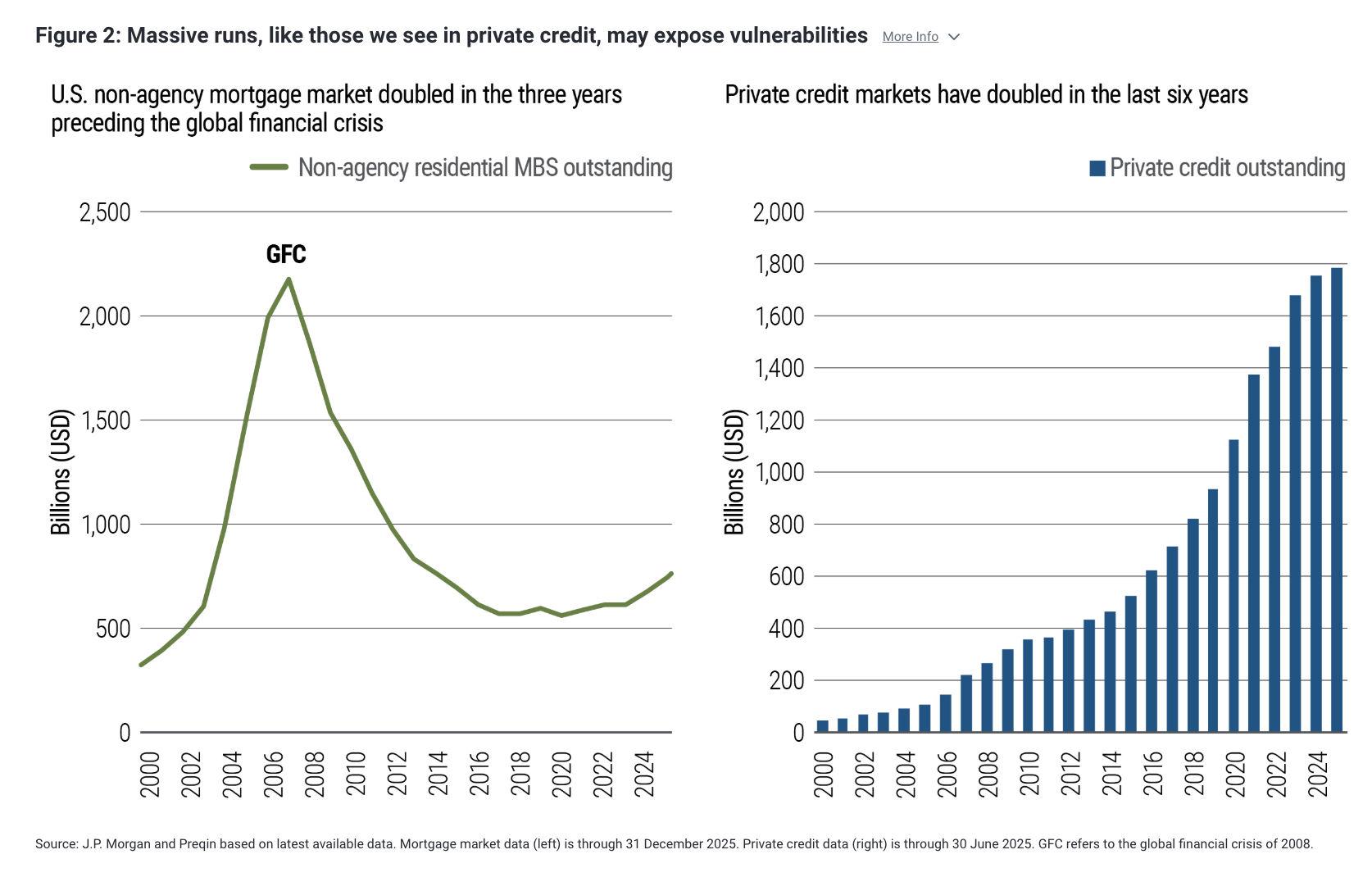

After a decade of strong private credit returns supported by rapid growth (see Figure 2), imbalances are coming into view. Signs of late‑cycle conditions are already visible within corporate direct lending, including elevated shadow default rates and greater reliance on payment‑in‑kind features. Smaller and midsize companies, the main borrowers within this market, are vulnerable to rising energy input costs, tariff pressures, and technology disruption, including from AI.

For investors, the trade‑off looks far less compelling in direct lending, the segment that has driven much of private credit’s growth, as financial conditions tighten. There is nothing inherently wrong with owning private assets – provided investors are adequately compensated for illiquidity. But in direct lending, that illiquidity premium has compressed just as refinancing risk, underwriting slippage, and questions around pricing transparency have become more pronounced. Direct lending strategies rely on reported price stability rather than market-based price discovery and may appear resilient until stress emerges – as it has lately.

As investors reconsider illiquidity risk, the disconnect between public and private market valuations has deepened. Publicly traded business development companies (BDCs) – investment vehicles for private direct lending – are trading at significant discounts to their net asset values (see Figure 3). This is a direct lending problem, in our view, not an indictment of private credit as a whole, which still encompasses strategies where illiquidity is better compensated and risks are more explicitly priced.

From a relative value perspective, this favors a shift out of direct lending and into high quality public fixed income. Many investments with attractive liquidity profiles and transparent pricing now offer yields comparable to private credit. As volatility rises and dispersion widens, the ability to manage downside risk and redeploy capital as conditions evolve matters more than trying to capture incremental yield by forfeiting liquidity.

Private credit does not pose a systemic risk, in our view, and there are many areas of the market that remain attractive (for more, see our March publication, “Private Credit’s Other Lanes Still Offer Value”). Still, stress in private credit could contribute to tighter financial conditions and weigh on hiring and investment.

As the cycle matures, credit markets – private and public – increasingly reward bottom-up analysis and differentiation. Balance sheet strength, durable cash flows, and high quality collateral matter more than headline yield, particularly in sectors undergoing structural change. It’s critical to focus on maximizing investment outcomes rather than simply deploying capital into an asset manager’s area of focus.

At PIMCO, we’ve managed through credit cycles for more than five decades. Looking across the continuum of public and private credit today, we see the greatest value in areas including U.S. agency mortgage-backed securities (MBS), investment grade issuers with stable, predictable cash flows, and high quality securitized credit.

In private credit, we favor asset‑based finance (ABF) and senior commercial real estate debt. While competition in ABF has grown, it remains a large and attractive market that offers collateral backing and is less correlated with the corporate earnings cycle than direct lending. Because global real estate has already gone through a cyclical downturn, investors can lend against assets that may be 15%–40% below peak values.

By contrast, we are cautious on direct lending and bank loans with weak covenants, lower‑quality high yield issuers, and many vehicle structures offering liquidity that doesn’t match the underlying assets.

Across credit markets, risk has been repriced only modestly in the wake of the Middle East conflict. Our emphasis is on adding downside mitigation, given risks have grown more than market pricing may reflect.

Fixed income is back at the center of portfolio construction

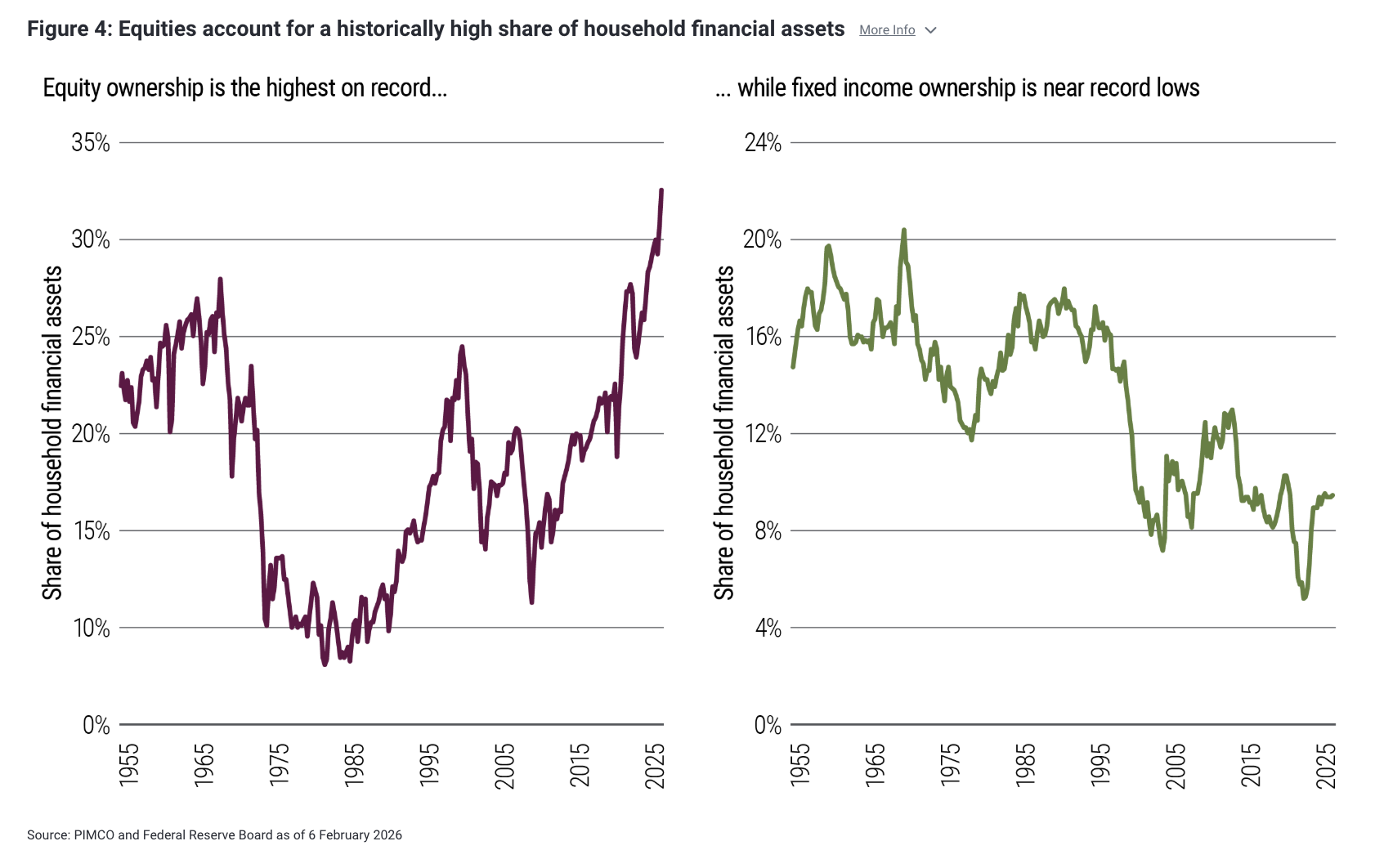

High quality bonds once again play a meaningful role in portfolios and look attractive across a variety of economic scenarios. For portfolios that have drifted heavily toward equities (see Figure 4), this is a practical moment to consider rebalancing. Yields across more liquid fixed income remain attractive, laying a solid foundation for market-driven income and return. When you overlay opportunities arising from volatility and mispricing, it creates an exceptional environment for active management to seek alpha, or outperformance versus the broader market.

High quality bonds can serve as a return generator, cushion against equity volatility, offer valuable diversification if growth disappoints or risk sentiment deteriorates, and provide liquidity that can be redeployed when markets dislocate.

We prefer a modest overweight to duration. In the U.S., the Treasury market is still a source of perceived “safe haven” yield and portfolio diversification benefits. We prefer more balanced curve exposure as yields look attractive across a range of maturities.

The case for global diversification also remains strong. Differences across countries are widening, creating both risks and opportunities. Rather than assuming correlated global outcomes, investors can potentially benefit from targeted exposures to select DM and EM countries with attractive real yields and credible policy frameworks.

Currency positioning matters more in this environment, particularly given the growing divergence between energy exporters and importers. Inflation‑sensitive assets also deserve a more deliberate role in portfolios today. Commodities, real assets, and Treasury Inflation-Protected Securities (TIPS) can help hedge real‑world purchasing power and diversify returns when traditional asset relationships become less reliable. These exposures may help improve portfolio resilience.

Conclusion

This is a market that rewards preparation for an uncertain set of outcomes. Higher yields, wider dispersion, and greater volatility create a favorable backdrop for active management, in our view, when portfolios are built with liquidity and flexibility in mind.

For investors, we believe it’s a compelling time to consider recentering portfolios toward fixed income, to use global diversification and inflation tools intentionally, to treat liquidity as an asset, and to emphasize quality and collateral in credit.

In short, this is a moment to consider rebalancing toward resilience – positioning portfolios to navigate dispersion while staying ready to act when opportunities arise.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. References to Agency and non-agency mortgage-backed securities refer to mortgages issued in the United States. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Investments in asset-based lending and asset-backed instruments are subject to a variety of risks that may adversely affect the performance and value of the investment. These risks include, but are not limited to, credit risk, liquidity risk, interest rate risk, operational risk, structural risk, sponsor risk, monoline wrapper risk, and other legal risks. Asset-backed securities may not achieve business objectives or generate returns, and their performance can be significantly impacted by fluctuations in interest rates. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. Diversification does not ensure against loss.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

Correlation is a statistical measure of how two securities move in relation to each other. Duration is the measure of a bond's price sensitivity to interest rates and is expressed in years. A K-shaped recovery is when segments of an economy recover from a recession at different rates. References to liquidity refer to normal market conditions. A “safe haven” is an investment that is perceived to be able to retain or increase in value during times of market volatility. Investors seek safe havens to limit their exposure to losses in the event of market turbulence. All investments contain risk and may lose value.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0318- 5318711

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO