Tax reform in 2017 reduced the statutory tax rate for corporations from 35% to 21%. As a result, lawmakers had to address taxes paid by noncorporate business owners who are considered “pass-through” entities for purposes of income taxation. These types of business owners are subject to a maximum individual tax rate of 37%, a much higher rate than the 21% rate applying to C-corps.

To address the disparity in taxing business owners, the deduction for qualified business income (QBI) was included as part of the 2017 Tax Cuts and Jobs Act (TCJA). This deduction allows certain pass-through business owners (sole proprietors, partnerships, most LLCs and S-corps) to generally deduct 20% of net business income from their individual tax return. This is a “below-the-line” deduction, meaning that it does not reduce adjusted gross income, and taxpayers can claim it regardless of whether they itemize deductions on their tax return. It’s important to note that there are other differences and considerations that need to be considered when comparing taxation of a business established as a C-corp versus pass-through businesses such as S-corps, partnerships or sole proprietors.

The 2017 tax law called for the QBI deduction to expire at the end of 2025, but the recent legislation (OBBBA) extended it permanently. The income requirements for the deduction were modified as well, meaning that more business owners will qualify for the deduction beginning this year. Given the potential value of this deduction, business owners should consult with their tax professional to understand how this deduction works and identify opportunities to maximize its impact.

The type of business and household income are key factors

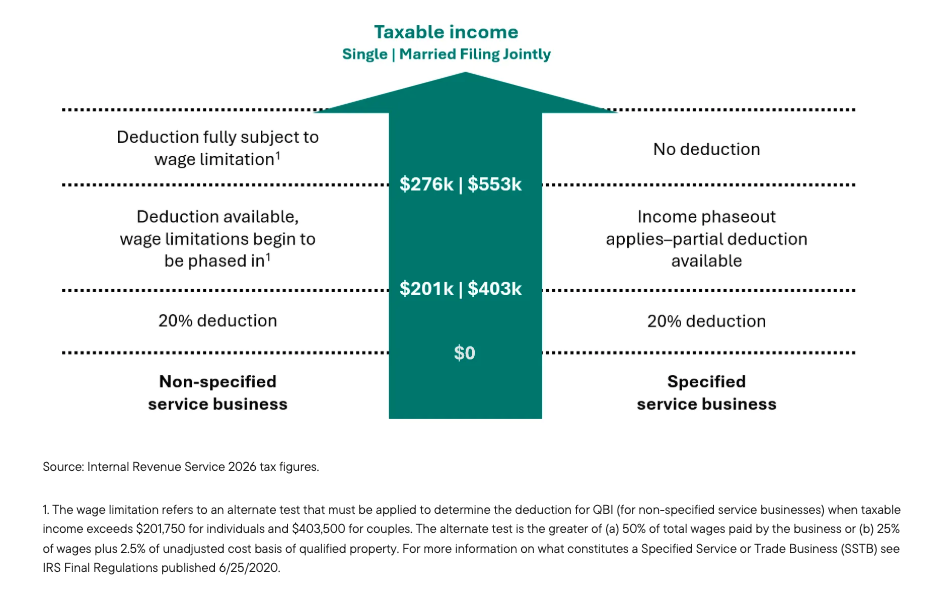

The QBI deduction is subject to income phaseouts (based on taxable income) that may reduce or disallow the deduction for certain professional service-related businesses in the areas of law, finance and accounting, to mention some.* For example, once household taxable income exceeds $553,500 for married couples filing a joint tax return for 2026, the deduction is no longer available. In the case of nonservice businesses, such as small manufacturing firms, once household income exceeds thresholds, the calculation of the deduction may change based on the aggregate wages paid to employees and the cost basis of certain property owned by the company. This is a very complex area requiring consultation with a tax professional.

* For more information on what constitutes a “service business” for purposes of applying the QBI deduction, see IRS publication 8995, Qualified Business Income Deduction.

QBI income phase-out thresholds for 2026

Maximizing the Deduction for Qualified Business Income (QBI)

Planning strategies to maximize the QBI deduction

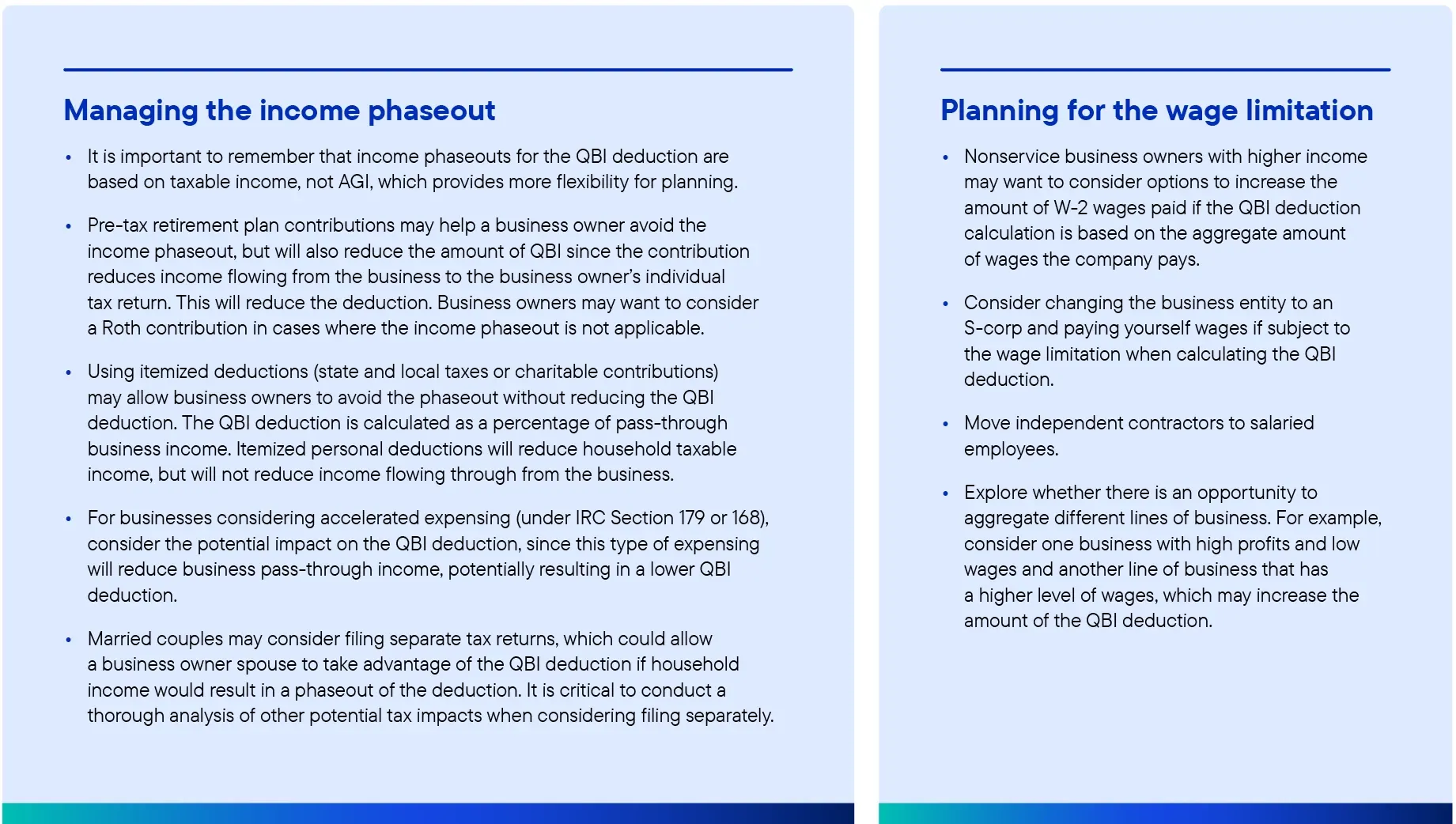

By tactically managing household income, business owners may be able to generate tax savings through strategies to maximize the deduction. Since the income phaseouts applying to the deduction are based on taxable income rather than adjusted or modified adjusted gross income, there are more flexible options for planning. For example, there are fairly limited alternatives in the tax code for reducing adjusted gross income (AGI). One option is contributing to a traditional retirement account. In contrast, there are more opportunities to reduce taxable income, including the use of itemized deductions such as charitable contributions. Lastly, business owners of nonservice companies with higher incomes may be subject to calculating the amount of QBI deduction based on the aggregate amount of wages paid. In some cases, increasing wages may lead to a larger QBI deduction.

Seek expert advice

It’s important to seek expert advice from a financial professional and legal or tax expert. The QBI deduction is complex, and it is important to work with a tax professional who specializes in working with business owners.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

© Franklin Templeton

Read more commentaries by Franklin Templeton