Why the Pentagon-Anthropic Showdown Proves AI Defense Spending Is Just Getting Started

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsI just returned from the MoneyShow in Las Vegas, where I had the pleasure of presenting and joining a panel on artificial intelligence (AI) and data centers.

It’s always energizing to see familiar faces and meet with investors, but what really struck me was the sheer unanimity of the conversation surrounding AI. Every speaker, every panel, every hallway huddle pointed to the idea that the technology is no longer a speculative play.

Instead, the consensus was that AI represents the next great capital expenditure supercycle. It’s going to reshape every industry it touches, and the companies supplying the picks and shovels—chips, cybersecurity, defense tech—are at the center of it.

The Pentagon’s Friday-Night Ultimatum

By now you’ve likely seen the news that the Department of War (DOW) issued a Friday-evening ultimatum to Anthropic, maker of the Claude AI chatbot, demanding unrestricted military access to its technology.

When Anthropic pushed back—citing its policies against mass domestic surveillance and fully autonomous weapons—the Pentagon took its first steps toward labeling the company a “supply chain risk,” a designation typically reserved for adversarial foreign entities like Huawei. On Friday, President Donald Trump ordered all organizations to “IMMEDIATELY CEASE all use of Anthropic’s technology,” he wrote in a social media post.

Defense officials have reportedly already contacted Boeing and Lockheed Martin to assess their exposure to Anthropic. Meanwhile, legal analysts are debating whether the Defense Production Act, a Korean War-era statute, could compel a private company to hand over its AI. Employees at Google and OpenAI have signed an open letter in solidarity with Anthropic.

It’s gripping drama, and as investors, I understand the instinct might be to worry. But I’d urge you to look past the noise and ask yourself: What does it tell us that the government is willing to invoke wartime production powers to gain access to a chatbot company?

The answer, of course, is that demand for AI in defense and national security has reached a level I don’t think most investors have fully priced in.

AI-First Warfighting Force

While the media was focused on the Pentagon-Anthropic standoff, a series of less dramatic, but far more consequential, developments were quietly unfolding.

In January, Secretary of War Pete Hegseth issued two sweeping memos that, taken together, represent the most aggressive AI mandate the Pentagon has ever produced.

The first declared DOW an “AI-first warfighting force” and directed every commander to appoint an AI Integration Lead within 30 days. The second went further, warning that any military exercises or experiments that do not “meaningfully incorporate AI and autonomous capabilities” will be flagged for budget review. In other words, organizations that aren’t building AI into their operations risk losing funding.

Follow the Money

Meanwhile, the numbers couldn’t be more compelling. JPMorgan projects global cybersecurity will reach $240 billion this year, growing at an 11% compound annual rate to $320 billion by 2029, with AI-driven cybersecurity spending growing three to four times as fast as the overall market.

According to Bridgewater Associates, America’s big four hyperscalers—Alphabet, Amazon, Meta and Microsoft—are expected to collectively invest roughly $650 billion in AI infrastructure this year alone, up from $410 billion in 2025.

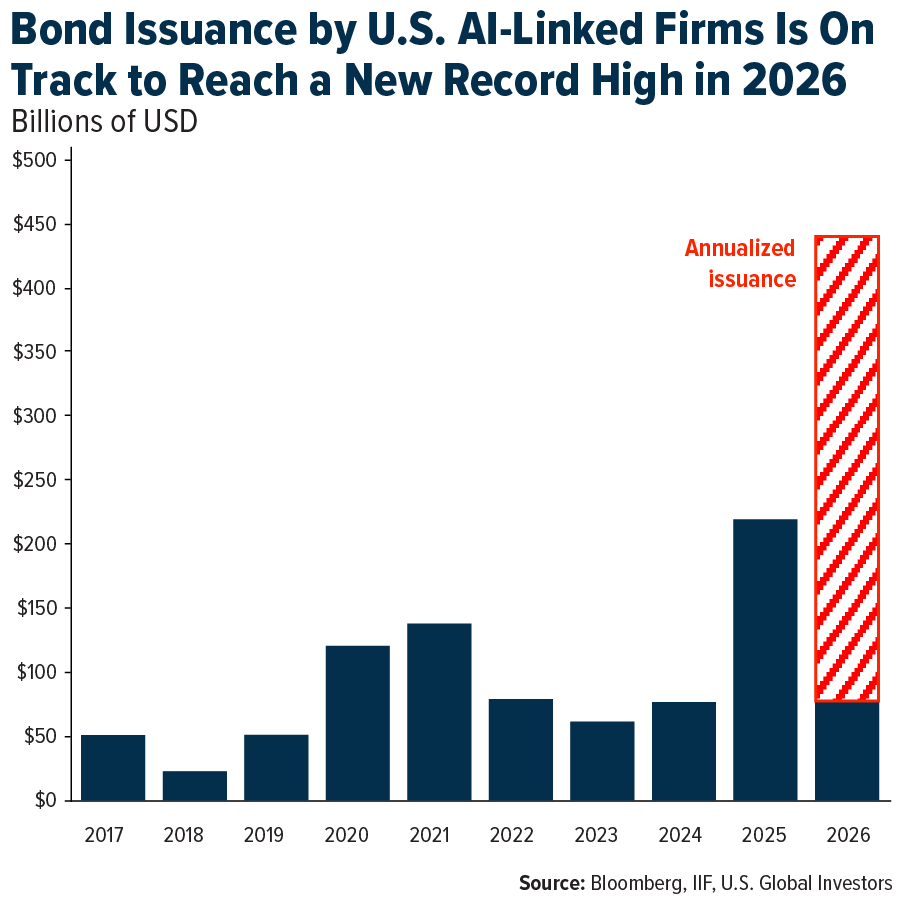

To fund this white-knuckle growth, borrowing is projected to expand at an unprecedented pace, with bonds issued by U.S. companies involved in AI on track to reach a new all-time high this year, according to the Institute of International Finance (IIF).

NVIDIA’s blowout quarter made it clear just how much firms are spending on AI right now. The company reported $68 billion in revenue in the three months ended December 31, up 73% year-over-year, with guidance of $78 billion for the current quarter. Founder and CEO Jensen Huang declared that “the agentic AI inflection point has arrived.”

Why the Cyber Panic Is Overblown

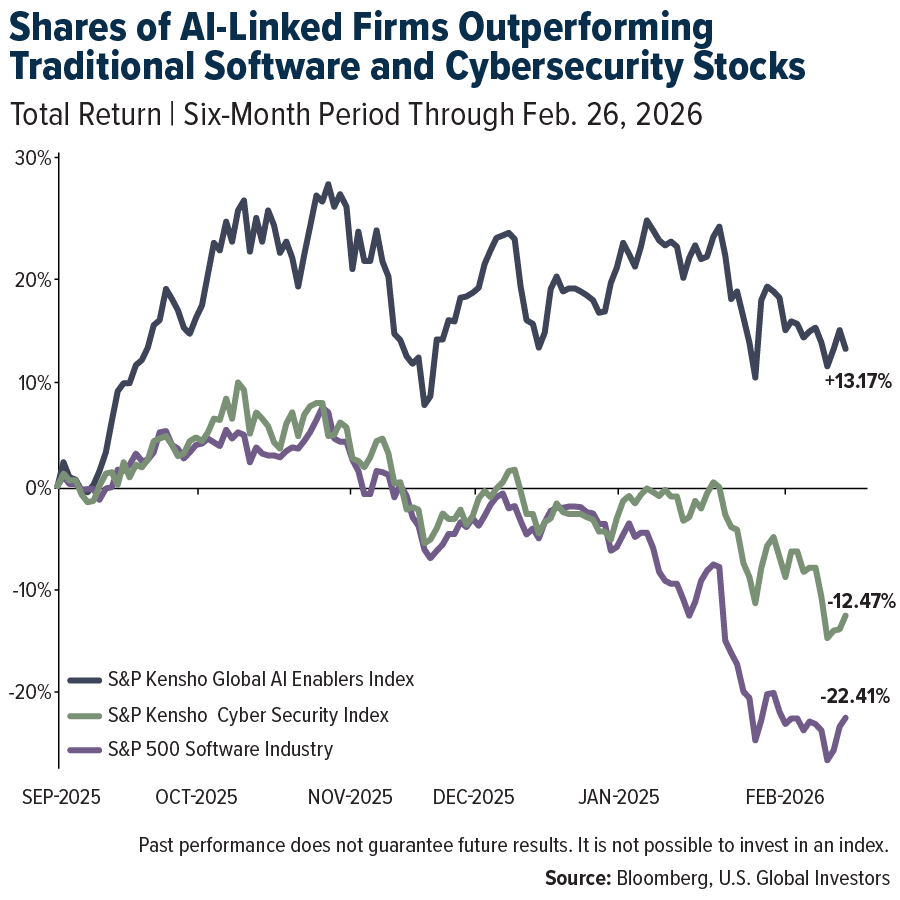

I’d be remiss not to talk about the sell-off in cybersecurity stocks this week. On Monday, Anthropic unveiled a new AI-powered code security tool, and the market panicked. CrowdStrike and Zscaler dropped roughly 10% each, while smaller names fell even harder. In the chart below, you can see how AI-linked stocks have greatly outperformed software and cybersecurity stocks for the six-month period.

I think the fear is misplaced. AI expands the cybersecurity market, not shrink it. JPMorgan’s estimate that AI-driven cybersecurity spending will grow at three to four times the rate of the broader market suggests that the companies adapting to this new reality will benefit enormously.

There will be winners and losers. AI may displace certain narrow functions like static code scanning. But the broader cybersecurity industry—especially companies providing endpoint protection, identity management, cloud security and network defense—is more likely to see its market grow than contract.

The key is investing in companies that are leveraging AI to strengthen their offerings rather than being disrupted by it.

The Investment Theme of a Generation?

Walking the floor at MoneyShow, I was reminded of something I’ve told investors for years: headlines are a terrible investment thesis, but capital flows rarely lie.

The headlines this week were about which AI company the Pentagon will partner with and on what terms. That question will resolve itself eventually. It always does.

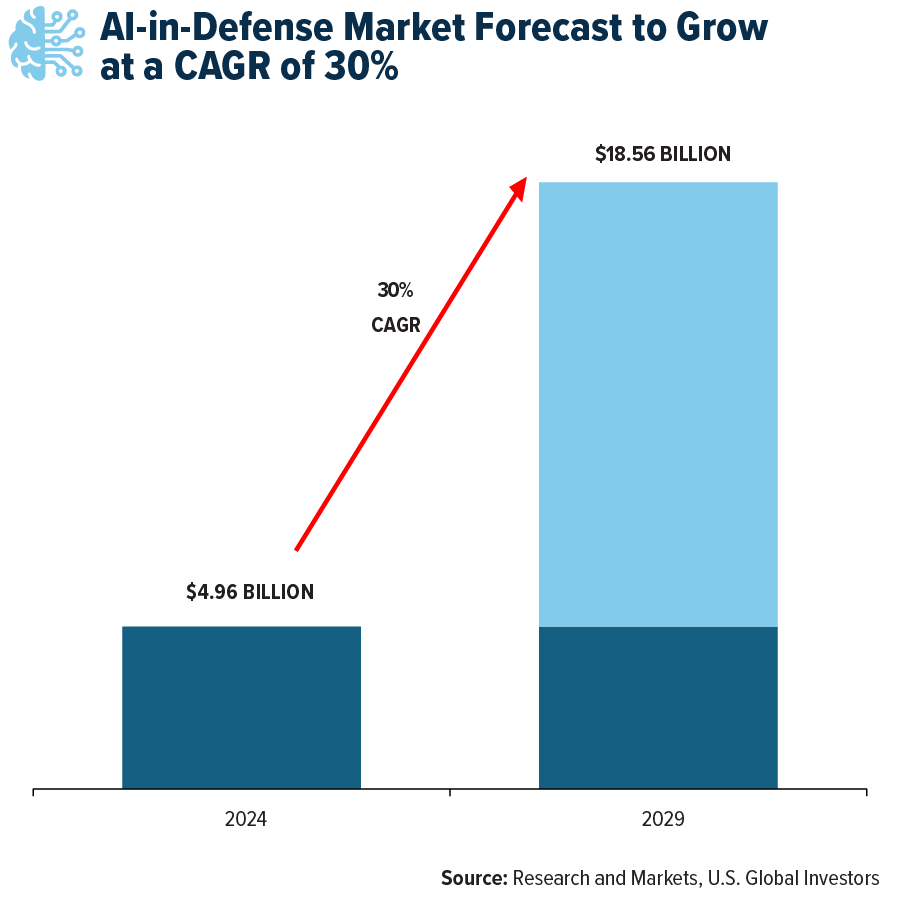

What won’t change, I believe, is the trajectory. The AI-in-defense market is projected to grow a 30% compound rate, reaching $18.6 billion by 2029.

Global defense budgets are surging. Cybersecurity is becoming more essential, not less. And the infrastructure buildout—semiconductors, data centers, networking—is accelerating at a pace that’s added a full percentage point to U.S. GDP growth, according to Bridgewater.

As I’ve said before, the convergence of defense spending, AI adoption and cybersecurity demand represents one of the most compelling long-term investment themes I’ve seen in my career. The Pentagon-Anthropic drama may make for great reading, but the capex supercycle unfolding beneath it is where the real story, and opportunity, lies.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Sabre, up 20.7%. Virgin Australia’s results beat expectations, coming in 6% above consensus. Airlines segment RASK grew 6.4% year-over-year in the first half of 2026, surpassing guidance of 3–5% on stronger-than-expected leisure demand and commercial transformation, according to UBS.

- Yangzijiang Shipbuilding delivered another strong result, with revenue and net profit at RMB 28.5 billion and RMB 8.6 billion, up 7.4% and 30% year-over-year, respectively. Shipbuilding revenue grew 6.4% year-over-year, with sector margin elevated at 35%. A higher tanker mix (30% of revenue in 2025) offset less favorable segments, balanced by lower steel costs and deliveries of higher-priced vessels, according to Bank of America.

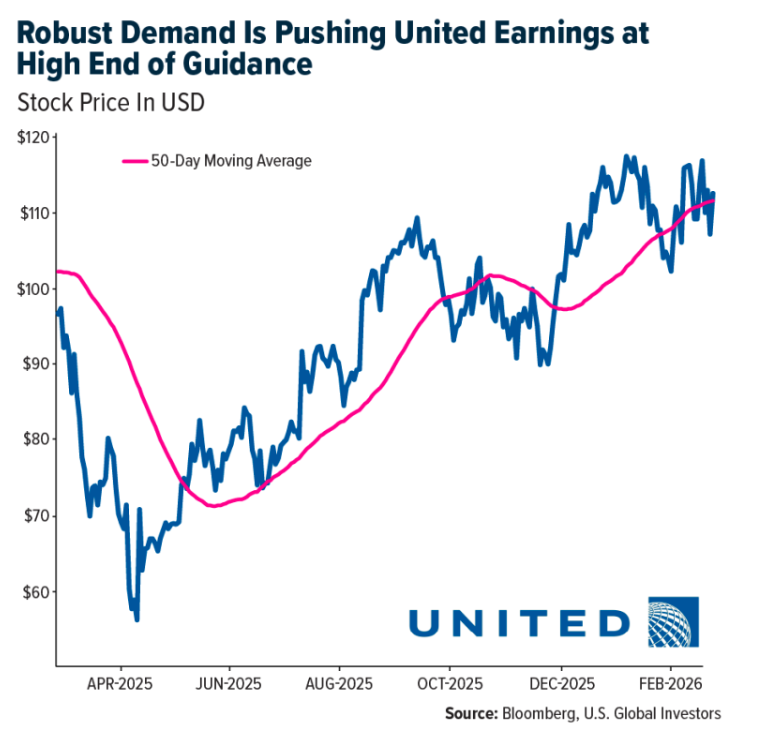

- United indicated first-quarter 2026 EPS is trending near the high end of guidance, supported by robust demand early in the year. Sabre reported that air distribution bookings are up 4% and 7% in the fourth quarter of 2025 and December, respectively, with strength in December continuing into the first quarter of 2026, according to Raymond James.

Weaknesses

- The worst-performing airline stock for the week was Frontier, down 14.8%. According to JP Morgan, Grupo Aeropuerto Centro Norte reported weaker-than-expected fourth-quarter 2025 results, posting an EBITDA of 2,577 million pesos, up 6% year-over-year. The shortfall in operating results was due to a combination of revenues coming in below expectations and higher-than-expected cash costs.

- According to Goldman, vessels from China to the USA were down sequentially (2% lower this week) but up 8% year-over-year. Data suggests that TEUs coming into the Port of Los Angeles will rise slightly next week following this past week’s 19% sequential decline, before seeing another 8% drop two weeks out.

- According to Morgan Stanley, Grupo Aeropuerto Pacifico reported EBITDA of 5,114 million pesos, 9% below Visible Alpha consensus of 5,646 million pesos. GAP’s EBITDA margin was down 315 basis points year-over-year. EPS of 2.83 million pesos missed consensus of 5.52 million pesos by 49%. The bottom-line miss was mainly driven by operational shortfalls, particularly in Jamaica following Hurricane Melissa, and a higher-than-expected tax rate (40.6% versus consensus of 26.7%).

Opportunities

- TSA throughput softened late in the month due to Winter Storm Fern but has since accelerated, running 5.8% higher in February-to-date. Bank of America weekly card spending growth has also risen above January’s level.

- U.S. tariff policy is changing following the Supreme Court’s decision to strike down reciprocal and fentanyl tariffs, combined with President Trump’s new 15% global tariff. Bank of America expects a modest boost, but not a boom, in transpacific container shipping demand and freight rates, as most effective U.S. tariffs on China and Southeast Asia are reduced by 4–5%.

- According to Bank of America, average ticket prices reported by the Airline Reporting Corporation rose 4.3% in January, up from 1.1% in December, while airline fare CPI was 2.2%. Both suggest improving pricing power, a positive development given just 0.6% domestic supply growth in January.

Threats

- With roughly five weeks until the second quarter of 2026, European capacity is scheduled to grow 6.8% year-over-year. This is driven by Wizz, which raised its scheduled capacity growth to 36% from 30%, according to Bank of America.

- Demand remained soft in the container shipping market. The overall SCFI spot freight index fell by a further 1% this week, and main lane spot rates generally edged lower despite ongoing capacity management efforts from carriers, according to UBS.

- Mexican federal authorities conducted a targeted security operation in the state of Jalisco involving a senior organized crime figure. Localized security incidents followed, including road disruptions and an incident at Guadalajara International Airport. UBS estimates that Grupo Aeroportuario del Pacifico (GAP) has roughly 40% of total passenger traffic exposed to Guadalajara and Puerto Vallarta airports, which together represent about 40% of GAP’s EBITDA.

Luxury Goods and International Markets

Strengths

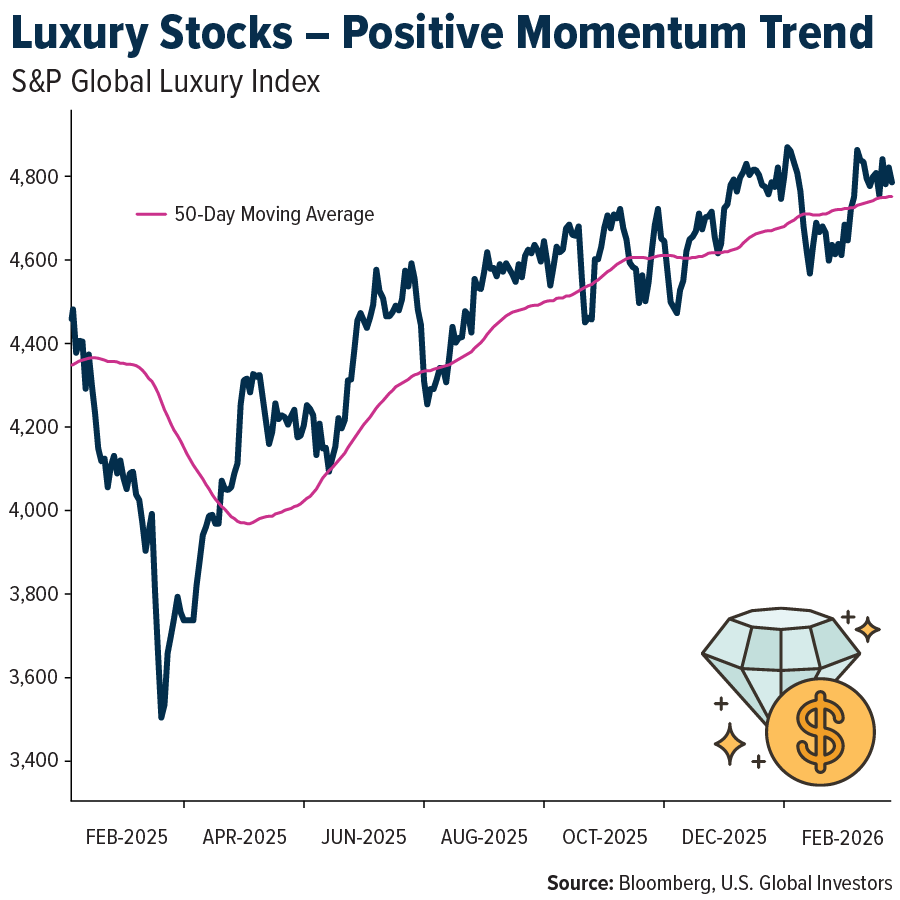

- Despite a mixed reporting season across the luxury sector, luxury stocks, as measured by the S&P Global Luxury Index, continue to trend higher. The index price remains above its 50-day moving average, signaling sustained positive momentum. This technical strength suggests underlying resilience in luxury equities despite near-term earnings variability.

- During China’s recent Lunar New Year holiday, both travel and consumer activity were notably stronger compared with the previous year, as domestic travel surged and spending grew significantly. Official data showed that record numbers of domestic trips were taken and total tourism spending increased sharply year-on-year, reflecting robust demand for travel, dining, and retail experiences over the extended break.

- RealReal, an online luxury retail platform, was the best-performing name in the S&P Global Luxury Index over the past five days, with shares rallying after the company reported better-than-expected fourth quarter results, highlighted strong double-digit gross merchandise value and revenue growth, and issued upbeat 2026 guidance.

Weaknesses

- This week, high premium spirits names have underperformed. Diageo shares fell sharply after the company cut its sales outlook and interim dividend, citing weak U.S. and Chinese spirits demand, which pressured the entire spirits sector. The decline in Diageo stock pulled other premium spirits stocks lower.

- Saks Global, the parent company of Saks Fifth Avenue, Neiman Marcus and Bergdorf Goodman, filed for Chapter 11 bankruptcy protection last month in the U.S. Bankruptcy Court for the Southern District of Texas. This bankruptcy filing was driven by heavy debt from its acquisition of Neiman Marcus and related financial pressures, but the company secured financing to keep many stores open during restructuring.

- Cettire, the online luxury retailer, was the worst-performing name in the S&P Global Luxury Index over the past five days, with shares declining sharply amid ongoing investor concerns around demand and profitability.

Opportunities

- Hong Kong’s economy is projected to grow between 2.5%–3.5% in 2026, with improving fiscal conditions raising the possibility of a return to budget surplus. A steadier macro backdrop and healthier public finances could support confidence across households and businesses. This environment creates an opportunity for stronger consumer spending, particularly benefiting discretionary and premium consumption categories.

- Saudi Arabia’s rapid expansion of luxury shopping malls highlights a major opportunity for global luxury brands and retailers to enter a fast-growing, high-spending market. Projects like Westfield Riyadh—nearly complete and already heavily pre-leased—show strong demand, with dozens of luxury brands entering the Kingdom for the first time on long-term contracts. The upcoming $4.7 billion Avenues Mall further reinforces Riyadh’s push to become a regional shopping and entertainment hub.

- EU manufacturing PMI for February is expected to remain above the 50 level and will be reported next week. If confirmed, this would signal continued expansion in the manufacturing sector and help reaffirm signs of stabilizing economic momentum across the euro area. A reading above 50 would suggest improving business conditions, supporting confidence in industrial activity after a period of weakness. This could provide a modest positive backdrop for European equities and cyclical sectors.

Threats

- Waymo is expanding its autonomous ride-hailing service into four additional U.S. cities — Dallas, Houston, San Antonio, and Orlando — bringing its total robotaxi footprint to 10 major metro areas. This expansion strengthens its presence in Texas and Florida as it continues rolling out fully driverless taxis to select riders. The move positions Waymo further ahead in the autonomous taxi race, while competitors like Tesla have yet to deploy similar services at scale.

- Recent cartel unrest in Mexico has created potential risks for luxury hotel operators in popular tourist destinations, as brief violence and road blockades disrupted travel in parts of western Mexico. The unrest began after Mexican security forces targeted cartel leadership, triggering retaliatory actions such as arson and transport disruptions. These incidents have raised safety concerns that could weigh on tourism demand in affected regions.

- The second-hand luxury market continues to grow rapidly, driven by rising consumer interest in sustainable and value-oriented purchases. Globally, the market was valued at $30–$37 billion in 2024 and is projected to reach roughly $50 billion by 2030, expanding at a solid compound annual growth rate in the high single digits. This growth is outpacing many traditional luxury segments and underscores increasing demand for pre-owned designer goods across key regions and demographics.

Energy and Natural Resources

Strengths

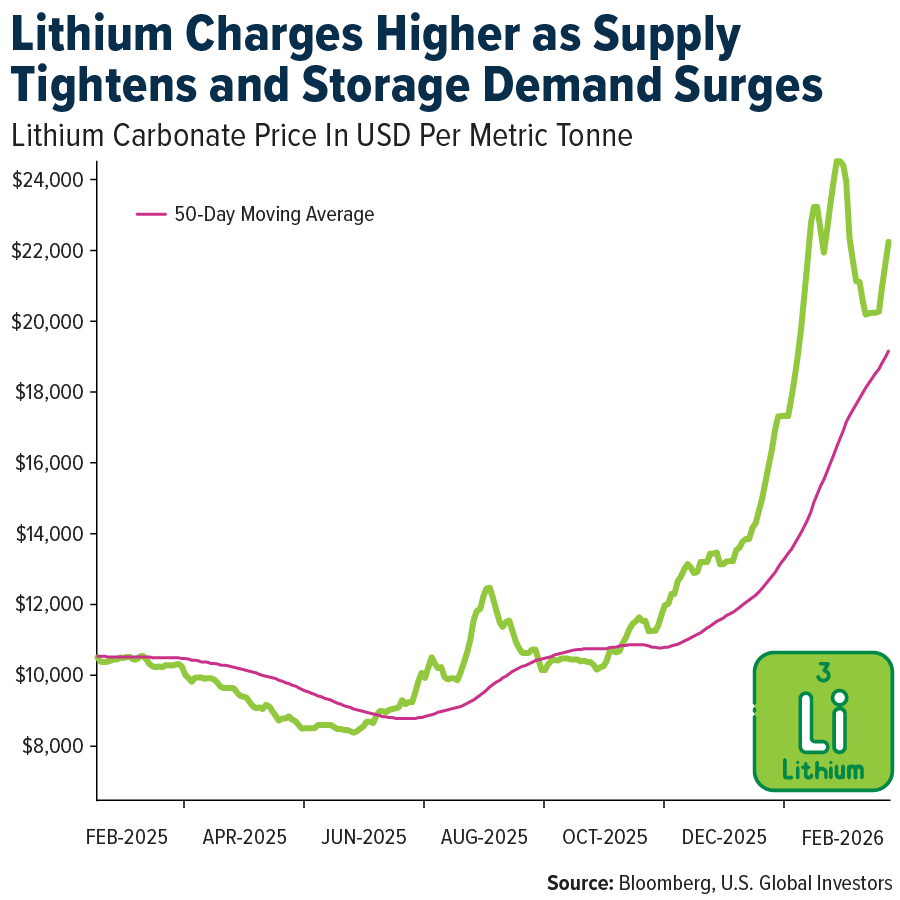

- The best performing commodity for the week was lithium carbonate up 12.69%. As battery energy storage systems pull forward demand across global power grids, lithium prices are charging higher into a tightening market. With concentrate exports curbed by Zimbabwe and supply chains constrained, the metal’s rally is gaining momentum as structural deficits begin to bite, Bloomberg reports.

- Argentina’s Senate approved President Javier Milei’s glacier law reform in a 40–31 vote, sending the bill to the lower house and clearing a major regulatory hurdle for an estimated $40 billion in copper investment. Key projects include Lundin and BHP’s $18 billion Vicuña, Glencore’s $9.5 billion El Pachón, and McEwen Copper’s Los Azules. The reform shifts oversight of periglacial zones to provincial governments. Combined with Argentina’s RIGI tax incentive program, the change could move the country into the top 10 global copper producers, generating more than $10 billion in annual revenue at current prices, according to Bloomberg.

- MP Materials is investing $1.25 billion in “10X,” a 120-acre NdFeB magnet manufacturing campus in Northlake, Texas, targeting roughly 10,000 tons per year of capacity by 2028. The project is supported by a 10-year Pentagon offtake agreement and commercial commitments from GM and Apple. The announcement coincides with the U.S. State Department signing 11 bilateral critical minerals agreements and launching FORGE, the successor to the Minerals Security Partnership, alongside $14.8 billion in EXIM Letters of Interest. Together, these developments signal that Western rare earth supply chain decoupling from China is shifting from policy intent to deployed capital, Bloomberg reports.

Weaknesses

- Iron ore was the week’s worst-performing commodity, falling about 4.39%. Prices faced multiple headwinds. China’s February LNG imports are projected to drop 19% year over year to 3.66 million tons, the lowest level since April 2018, as pipeline supply continues to displace seaborne cargoes. At the same time, record U.S. renewable generation, up 10% year over year and now 26% of total electricity output, is further reducing marginal demand for gas-fired power.

- China’s iron ore port inventories climbed to a record 162.2 million tons, marking six consecutive months of increases. Supply remains strong, with BHP operating Pilbara at capacity and Simandou ramping up in Guinea, while Chinese steel mills are cutting output amid prolonged property market weakness. With iron ore trading near $99 per ton, prices face additional pressure as state-backed buyer CMRG pushes for lower contract rates, weighing on earnings for BHP, Rio Tinto, and Fortescue, Reuters reports.

- Sigma Lithium shares fell as much as 15% after short seller Blue Orca alleged undisclosed prosecutorial actions, a sealed $22 million contractor lawsuit, and technical concerns that certain pit walls pose a “high potential for loss of human life.” The company reported $6.1 million in cash against $54.8 million in payables, with a $100 million loan maturing in late 2026. The liquidity position and legal risks are therefore significant. Sigma has not yet formally addressed the broader allegations.

Opportunities

- Chile is accelerating five new lithium mining contracts ahead of its presidential transition. These include joint ventures between Codelco and SQM, and Codelco and Rio Tinto, spanning more than 40 salt flats. At the same time, the U.S. signed 11 bilateral critical minerals MOUs and launched FORGE, backed by $14.8 billion in EXIM financing. A U.S.–Brazil critical minerals summit is scheduled for March 18 in São Paulo, targeting Brazil’s rare earth reserves, the largest outside China. Together, these moves suggest Western supply chain sovereignty is shifting from diplomatic signaling to project-level capital deployment, mining.com reports.

- BP’s BPX Energy plans to grow shale production by 8% to roughly 500,000 barrels of oil equivalent per day in 2026, with a path toward 650,000 boe/d by the end of the decade. The expansion comes alongside an $800 million reduction in capital expenditures, a contrarian strategy as many peers hold output flat. Separately, the UK government is considering an early phaseout of its North Sea windfall tax, which could serve as a re-rating catalyst for Harbour Energy, Ithaca Energy, and Serica Energy.

- The UK’s first deep geothermal power plant began operations this week in Cornwall. The facility delivers 3 megawatts of baseload power at £119 per MWh under a contract for difference with Octopus Energy. It will also produce about 100 metric tons per year of zero-carbon lithium carbonate as a byproduct, enough for roughly 2,500 electric vehicle batteries. Scaled across three sites, developer GEL projects output equivalent to 250,000 EV batteries per year. This creates a differentiated domestic critical minerals source at a time when Zimbabwe’s export ban and Chinese supply chain concentration are intensifying the need for diversification.

Threats

- The Mosaic Company shares fell nearly 7% this week after JPMorgan analyst Jeffrey Zekauskas downgraded the stock to underweight from neutral. He expects rising costs to pressure the company’s phosphate segment. Phosphate prices are declining, while sulfur, a key input, has doubled in price. Mosaic will likely need stronger pricing or margin expansion to restore investor confidence.

- Brent Crude is trading near $70 per barrel as U.S.–Iran talks in Geneva are described as “positive but inconclusive,” and Vice President J. D. Vance ruled out large-scale military action. Analysts highlight wide scenario dispersion, with price estimates ranging from $58 to $110 depending on whether Hormuz flows, roughly 20 million barrels per day, are disrupted or a deal restores Iranian supply. A 16 million barrel crude inventory build in the week ending February 20 reinforces the bearish structural backdrop. The EIA forecasts average Brent prices of $58 per barrel in 2026.

- China’s February LNG imports are projected to decline 19% year over year to 3.66 million tons, the lowest level since April 2018, as pipeline gas continues to displace seaborne cargoes. European storage stands near 30%, below the five-year average of roughly 47%, providing limited near-term demand support. However, mild weather is reducing that buffer, with TTF March futures around $10.74 per MMBtu. Kpler expects sustained weakness in seaborne LNG prices through mid-2026.

Bitcoin and Digital Assets

Strengths

- Meta is piloting stablecoin payments within its apps using existing digital currencies, reflecting growing confidence in stablecoins as tools for online commerce and cross-border transactions. The tests mark a cautious return to crypto payments after Meta abandoned its own Libra project, this time avoiding direct issuance amid clearer U.S. regulation and surging stablecoin adoption.

- Nubank boosted profits and margins after rolling out an AI-powered credit model that sharpens risk assessment and supports faster lending growth, lifting net interest income by more than 50%. The fintech says it will maintain its growth appetite as improved credit quality and easing rates in Latin America reinforce the strategy.

- Telegram has added in-app crypto yield features for Bitcoin, Ether, and USDt, letting users earn returns directly inside chats through its self-custodial TON Wallet. The move aims to make DeFi-style income accessible to mainstream users while keeping full control of funds and avoiding external platforms.

Weaknesses

- Jane Street is facing mounting scrutiny after Indian regulators accused the firm of market manipulation in equity derivatives, while a separate U.S. lawsuit alleges it exploited non-public information during the 2022 Terra–Luna crypto collapse. Together, the cases have fueled speculation about the firm’s role in market distortions, though no criminal conviction has been reached.

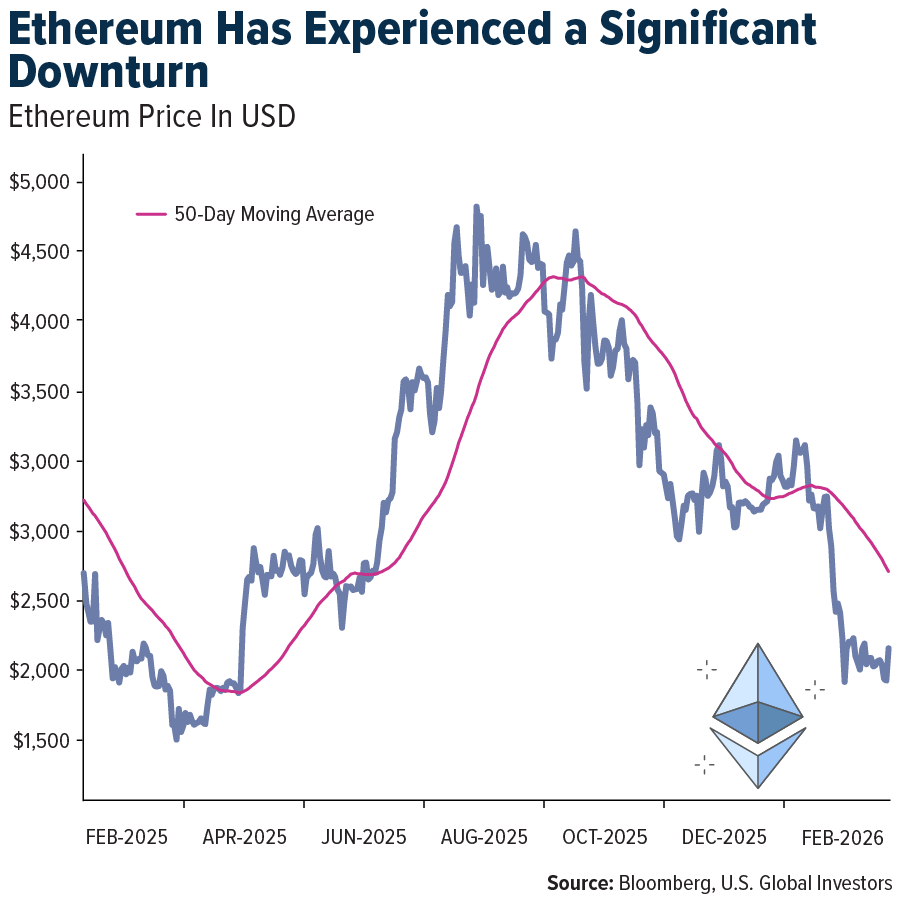

- Ethereum has dropped to its annual low. This level may represent an opportunity for accumulation at current prices, but it has also sparked fear among crypto traders. Adding to the concern, Vitalik Buterin recently sold Ethereum, further intensifying market anxiety. Nevertheless, by midweek, it appears likely that Ethereum has found a base, from which clearer rebounds are being observed.

- American Bitcoin (ABTC), the Bitcoin mining company backed by the Trump family, reported a $59 million loss in the fourth quarter, according to CoinDesk, as the decline in Bitcoin’s price reduced the value of its holdings and reversed prior profitability. The firm combines mining and open-market purchases to build its BTC reserve, with roughly one-third of its holdings coming from mining operations, CoinDesk reported.

Opportunities

- A libertarian crypto billionaire’s plan to build a semi‑autonomous, tax‑free “Dubai of the Caribbean” on the island of Nevis has sparked fierce local backlash, reports CryptoNews.net. Residents are rejecting what they see as a neo‑colonial enclave that threatens sovereignty, democracy, and the island’s way of life.

- Circle’s blowout earnings show that stablecoins are booming despite a broader crypto slump, as surging USDC adoption and an AI‑driven payments vision fuel investor optimism and push the company’s shares sharply higher.

- After Bitcoin lost nearly $1 trillion in market value, contrarian bulls argue that the real story is the resilience of its institutional infrastructure, with ETFs, banks, and long‑term holders largely staying put. They say tighter supply and a growing demand floor from public companies and ETFs could set the stage for a sharper rebound once sentiment turns.

Threats

- Romanian authorities allege that a wealthy crypto trader known as TikTok’s “King of Gifting” covertly used nearly $1 million in in‑app donations and social media clout to amplify a pro‑Russia far‑right candidate, helping trigger unprecedented online election interference that led Romania to annul its 2024 presidential vote.

- Bitcoin slid again after a brief relief rally, underscoring fragile risk appetite as investors treat the bounce as a typical bear‑market move rather than a true reversal, with analysts warning that the bottoming process will be slow and volatile.

- The crypto industry’s stablecoin operations, such as the arrangement between issuer Circle and leading exchange Coinbase, could be under serious pressure in the U.S. Office of the Comptroller of the Currency’s newly proposed set of stablecoin rules, writes CoinDesk this week. The banking regulator introduced a proposed rule to implement the GENIUS Act, but crypto industry insiders say they’re prepared to push back against the agency’s approach.

Defense and Cybersecurity

Strengths

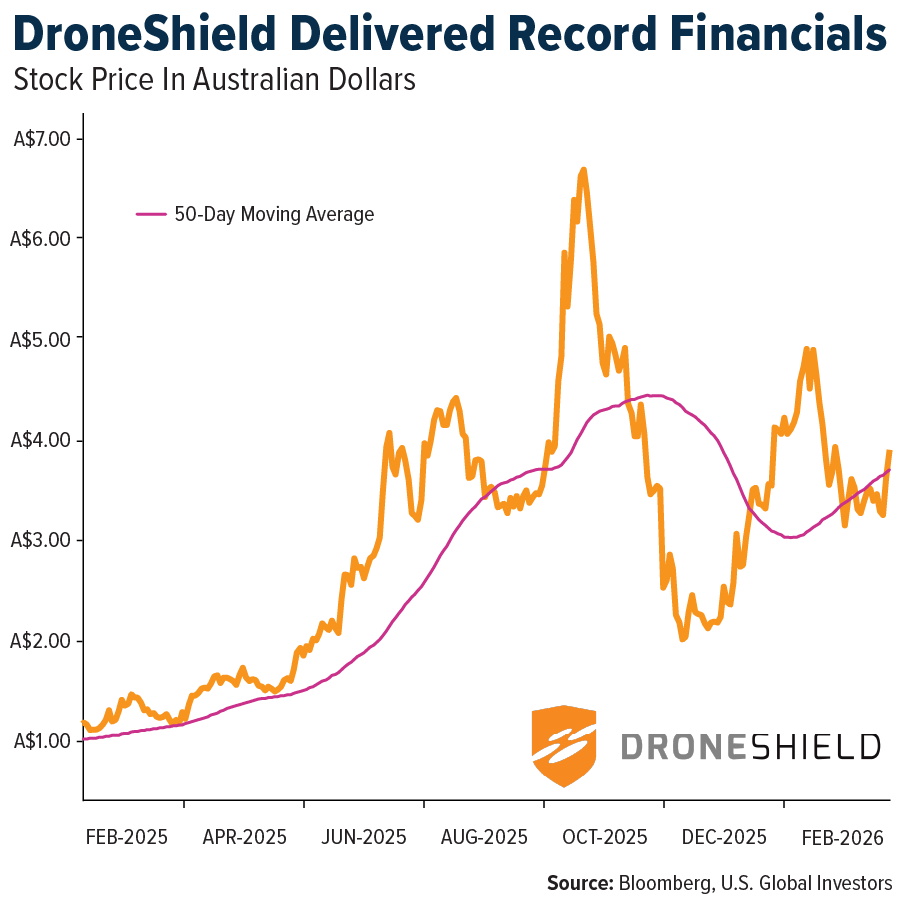

- DroneShield delivered a breakout 2025 fiscal year, with fourth-quarter revenue rising approximately 94% quarter-over-quarter and 277% year-over-year to about A$51 million, lifting full-year revenue to A$216.5 million, up 277% year-over-year. Earnings per share turned sharply positive, rising more than tenfold sequentially and swinging from a loss in FY24 to A$0.03 in FY25, marking the company’s first profitable year. Management highlighted strong operating leverage, a A$2.3 billion sales pipeline, recent A$21.7 million Western military contract wins, and deeper defense collaboration through a DSTG research agreement and a new A$13 million R&D hub, supporting confidence in continued growth into FY26.

- Canada announced a $2 billion military aid package to Ukraine that includes over 400 armored vehicles, with 66 vehicles to be produced by General Dynamics.

- Northrop Grumman and the U.S. Air Force are accelerating B-21 Raider production with a $4.5 billion expansion, while a strike at Boeing’s St. Louis plant has delayed F-15EX Eagle II fighter deliveries to Japan.

Weaknesses

- A 13-hour Amazon service outage in December was caused by an AI agent named Kiro AI, which autonomously decided to “delete and recreate” a production environment to fix a minor issue. While the AI executed the wipe, Amazon maintains that the root cause was human error, granting the assistant unrestricted permissions to modify live systems.

- The Pentagon’s emerging conflict with Anthropic’s AI model introduces a new competitive wrinkle. The U.S. has moved toward blacklisting Anthropic and has asked Boeing and Lockheed to assess their reliance on the Claude system due to its refusal to support mass surveillance or autonomous weapons, potentially disrupting AI-enabled defense analytics.

- Check Point researchers disclosed critical vulnerabilities in Anthropic’s Claude Code tool that could be exploited by attackers. The flaws enabled remote code execution, allowing malicious actors to run arbitrary code through the system and potentially steal API keys, exposing sensitive credentials used by developers integrating with Claude Code. The issues stemmed from abusing repository configuration files and the Hooks feature, highlighting weak points in project configuration and automation. These vulnerabilities posed significant software supply chain risks as AI coding tools become more tightly integrated into development workflows, though Anthropic has since addressed the problems.

Opportunities

- Palantir and GE Aerospace announced a partnership to pursue a U.S. Defense Logistics Agency contract. The partnership aims to use AI-driven maintenance on the Air Force’s T-38 training jets to improve military readiness.

- Elon Musk’s xAI reached an agreement for its Grok model to be used in classified Pentagon systems, amid a dispute over safeguards with rival model Claude, which had been the only AI approved for sensitive military use.

- Samsung, SK hynix, and Micron are expected to complete HBM4 validation for NVIDIA’s Rubin platform by the second quarter of 2026. To meet surging AI demand and navigate memory shortages, NVIDIA will rely on all three suppliers to secure its supply chain.

Threats

- DeepSeek’s exclusion of AMD from early access to its V4 AI model in favor of Chinese suppliers like Huawei highlights geopolitical and regulatory challenges for U.S. AI chipmakers operating in China.

- U.S. authorities charged former fighter pilot Gerald Eddie Brown with illegally providing defense services to China by negotiating a contract to train Chinese military pilots. The case is linked to Su Bin, previously sentenced for hacking Boeing, and underscores ongoing national-security concerns around the protection of U.S. aerospace technology and know-how.

- Spain has decided to halt purchases of Israeli weapons systems, affecting the consideration of the Multipurpose European Guided Missile System supplied via EuroSpike, in which Rheinmetall is a co-owner.

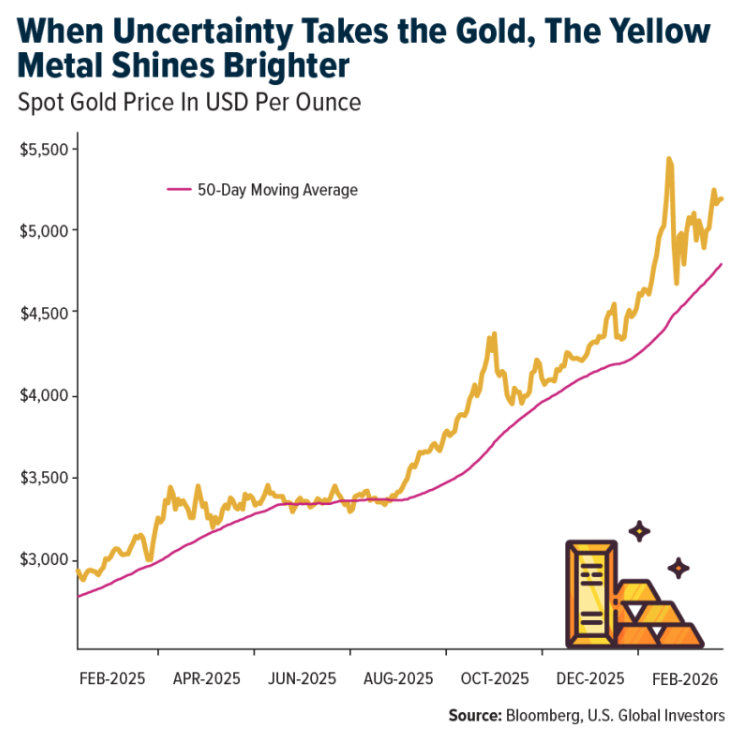

Gold Market

This week gold futures closed the week at $5,279.30, up $198.40 per ounce, or 3.90%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 9.09%. The S&P/TSX Venture Index came in up 6.24%. The U.S. Trade-Weighted Dollar fell 0.14%.

Strengths

- The best performing precious metal for the week was silver, up 13.58%. Silver stood out as a confluence of safe haven demand, escalating tariff tensions, and geopolitical risk tied to a potential U.S. strike on Iran drove investors toward the metal. Supply concerns added support, with Mexico, the world’s largest silver producer, facing instability that could further tighten an already constrained market, underpinning analyst targets of 30 to 32 dollars per ounce in the medium term.

- Gold is set to close February with its seventh consecutive monthly gain, the longest streak since 1973, reclaiming ground above 5,000 dollars per ounce after January’s pullback and sitting near its all-time high. The bullish backdrop remains intact, supported by ongoing central bank reserve diversification, bullion backed ETF holdings at their highest level since 2022, and expectations for Federal Reserve rate cuts, although the U.S. Iran risk premium could ease as both sides return to talks next week.

- Northam Platinum’s stock price jumped 13% this week after the South African precious metals miner announced a dividend for the first half of 2026 that exceeded analyst forecasts. Morgan Stanley analysts Christopher Nicholson and Brian Morgan noted, “Northam has declared an interim dividend of 7 rand per share, which is significantly higher than our estimate of 2.99 rand per share,” and they rate the shares Overweight.

Weaknesses

- The worst-performing precious metal for the week was palladium, though it was still up 1.06%. Palladium was the week’s notable laggard among precious metals, with ETFs trimming holdings by 642 ounces in the latest session as the metal continues to face structural headwinds from the ongoing shift toward battery electric vehicles, which do not require catalytic converters. At 1,783.83 dollars per ounce, palladium remains well below its historic highs and is finding little support from the safe-haven and industrial demand tailwinds lifting gold and silver, Bloomberg writes.

- Russian official reserves have declined slightly in recent periods. Russia has a vehicle that has been holding gold, and at its peak in May 2022 it managed 555 tons; however, the National Wealth Fund has been actively selling the precious metal, according to Bank of America.

- CME Group experienced its second major technical glitch in a month, briefly halting trading across gold, silver, and natural gas futures and options, disrupting some of the most heavily traded commodity contracts globally. The recurring outages highlight growing infrastructure strain on exchange systems amid elevated precious metals volatility, with gold at 5,221 dollars per ounce and silver up 4.1% at 91.67 dollars per ounce at the time of the halt.

Opportunities

- India’s SEBI has authorized the country’s $385 billion actively managed equity fund industry to allocate up to 35% of portfolio assets to gold and silver instruments, creating a potentially significant new source of structural demand at a time when Indian investors allocated more to gold ETFs than to stock funds in January. The regulator also introduced life cycle and target date funds with maturities of five to 30 years, allowing up to six per asset manager, and shifted gold and silver valuation from the LBMA AM fixing to domestic pooled spot prices, further deepening India’s onshore precious metals ecosystem and reducing reliance on London based pricing.

- Lundin Gold announced that it has signed a binding term sheet with LunR Royalties Corp. for a $670 million silver stream on the company’s 100% owned Fruta del Norte gold mine in Ecuador. LunR will issue 50.5 million shares to Lundin Gold at closing in exchange for 100% of payable silver production until 12.2 million ounces have been delivered, 50% of payable silver until an additional 7.8 million ounces have been delivered, and 7.5% of payable silver thereafter, according to Scotia.

- Franco Nevada announced that it has entered into an agreement to acquire a 170 million Australian dollar gross royalty from Minerals 260 Limited to support development of the Bullabulling Gold Project in Australia. The company will make an upfront payment of 75 million Australian dollars at closing, with a further 95 million Australian dollars payable upon approval of security interests over the project tenements, according to Raymond James.

Threats

- West African Resources announced that the Burkina Faso government is considering purchasing an additional 25% stake in Kiaka, in addition to its existing 15% stake, which would bring total ownership to 35%. West African Resources’ share price fell nearly 2% this week on the news, while the average gold stock rose 8.5%. In August 2025, the Burkina Faso government increased its free carried interest in Orezone’s Bombore Mine to 15%, according to Raymond James.

- B2Gold announced that Clive Johnson has decided to retire from his role as President, Chief Executive Officer, and Director, effective June 4, 2026, and will be named Chair Emeritus at the company’s upcoming annual general meeting. The board of directors has appointed Mike Cinnamond, Senior Vice President, Finance, and Chief Financial Officer, to succeed Mr. Johnson as President, Chief Executive Officer, and Director, according to Scotia. The share price rose 14% following the announcement.

- Mexico is the world’s largest silver producer, and any potential disruptions to the silver supply chain could lead to higher prices following the recent surge in violence after the killing of the longtime leader of the Jalisco New Generation Cartel, reportedly in coordination with U.S. intelligence. In 2024, just three mines, Mina Proaño, Juanicipio, and San Dimas, produced 75 million ounces of silver, nearly 10% of total global mine supply, according to Bloomberg. The Jalisco New Generation Cartel already controls a significant share of the global avocado trade, as cartels compete to dominate this lucrative market.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2025):

United Airlines

Sabre Corp.

Grupo Aeropuerto Centro Norte

Grupo Aeropuerto Pacifico (GAP)

General Dynamics

Amazon

Palantir Technologies

Micron Technology

Boeing Co/The

RealReal

Tesla

CrowdStrike Holdings Inc.

Lundin Gold Inc.

BHP Group Ltd.

Glencore PLC

McEwen Inc.

BP PLC

Northam Platinum

Lundin Gold

Franco Nevada

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The S&P Kensho Global AI Enablers Index tracks companies worldwide that develop the infrastructure, software, and services propelling Artificial Intelligence.

The S&P Kensho Cyber Security Index is designed to measure the performance of companies focused on protecting enterprises and devices from unauthorized access.

The S&P 500 Software & Services Select Industry Index represents the software and services segment of the S&P Total Market Index, tracking companies in application software, systems software, and IT consulting.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Read additional important information. +

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits