Key Points

-

Carry is an important return driver for multi-asset futures and forwards. Simple trend signals have benefited from trading in line with, not against, the carry of an asset. In practice, this means avoiding long (short) positions in negative (positive) carry assets.

-

Carry’s benefit is neither universal over time nor consistent across markets; the decision to filter has many complexities. For example, in 2022, pure trend portfolios materially outperformed their carry-conditioned counterparts, which were blocked from shorting bonds, a very strong trend, for most of the year.

-

To understand if periods such as 2022 are a harbinger of things to come, we perform a deep dive into the dynamics of carry across assets and the implications for various conditioning approaches within a trend strategy.

-

We conclude by offering what we believe is a novel economic rationale relating trend and carry together through the mechanism of carry’s contribution to each asset’s returns. The more carry has contributed to a future’s or forward’s long-term return, the more critical it is to filter this market’s trend signal with carry, with conditioning’s effectiveness diminishing as the length of a trend strategy’s lookback increases.

Introduction

Trend following strategies buy (sell) rising (falling) assets and traditionally provide downside protection during equity market corrections. In 2022, for example, the Société Générale (SG) Trend Index rose 27.4% while the S&P 500 fell 18.1%.

In the last decade, carry filtering has enhanced returns for plain vanilla trend strategies. Molyboga, Qian, and He (2020) describe carry and trend as “a match made in heaven,” and Bhansali, Davis, Dorsten, and Rennison (2015) sum up the combined approach with the following pithy quote: “[B]e on the right side of the trend, and don’t pay too much while you are at it.” These two papers find that trend and carry strategies perform better when they follow trends in the time series and trade in the same direction as an asset’s carry (i.e., when trend and carry are jointly positive or negative). This implies that “filtering” trend on carry should improve returns when forming signals.

For those unfamiliar with these concepts, consider U.S. Treasuries as an illustrative example. Their yield curve mostly slopes upward; they appreciate as time passes and they roll down the curve. When bonds trend negatively, their prices fall. Thus, selling bonds based on this trend signal alone trades against the positive roll down provided by the yield curve.

But the simple and powerful “match made in heaven” conclusion masks the more complicated nature of trend and carry’s relationship; take the examples of gold and silver. Each of these instruments has been in contango, or negative carry, more than 98% of the time since 1989.1 Why? Because futures investors pay the short-term risk-free rate, but since these assets are cheap to hold, there is little compensation in the form of the convenience yield (relative to storage and insurance costs). Applying a naïve carry filter on trend to gold and silver would prohibit a trend strategy from going long either of these commodities. Here, it seems, trend and carry are in clear tension with one another.

In this article, we explore the nuances of conditioning trend on carry. We first demonstrate the benefits of trend and carry working in concert with one another in a much larger universe than both Bhansali, Davis, Dorsten, and Rennison (2015) and Molyboga, Qian, and He (2020). We then highlight some of the deficiencies of an otherwise simple but common approach to carry conditioning through the lens of several individual and groups of assets, identifying the drivers of filtering’s outperformance over pure trend. Finally, we offer a novel economic rationale that relates trend and carry together through carry’s contribution to each asset’s returns. Our hypotheses are two-fold: 1) the more carry contributes to an asset’s long-term returns, the more important it is to filter this market’s trend signal with carry; and 2) the longer a trend strategy’s lookback, the less effective carry conditioning becomes at the margin.

Definitions and Data

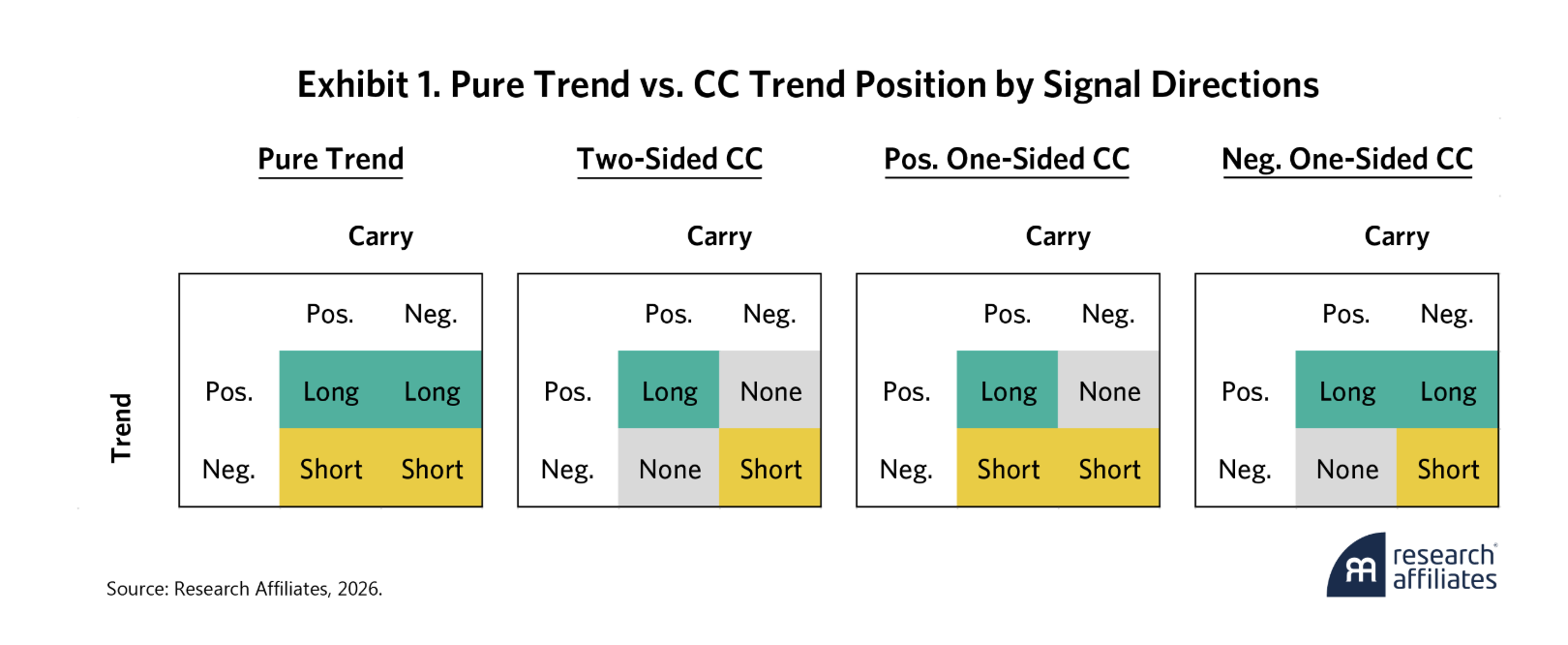

What does carry conditioning (CC) mean in the context of a trend following system? Conventional “Pure Trend” strategies take positions in an asset based on the sign and possibly the magnitude of that asset’s trailing return. Exhibit 1’s first table shows how Pure Trend establishes its positions. Now consider what happens when we condition on the sign of an asset’s carry. In the two-sided case, we only take positive (negative) trend positions when they are supported by positive (negative) carry. In the one-sided cases, we only require trend and carry to align on one side of the market (either longs or shorts), while leaving the other side unconstrained.

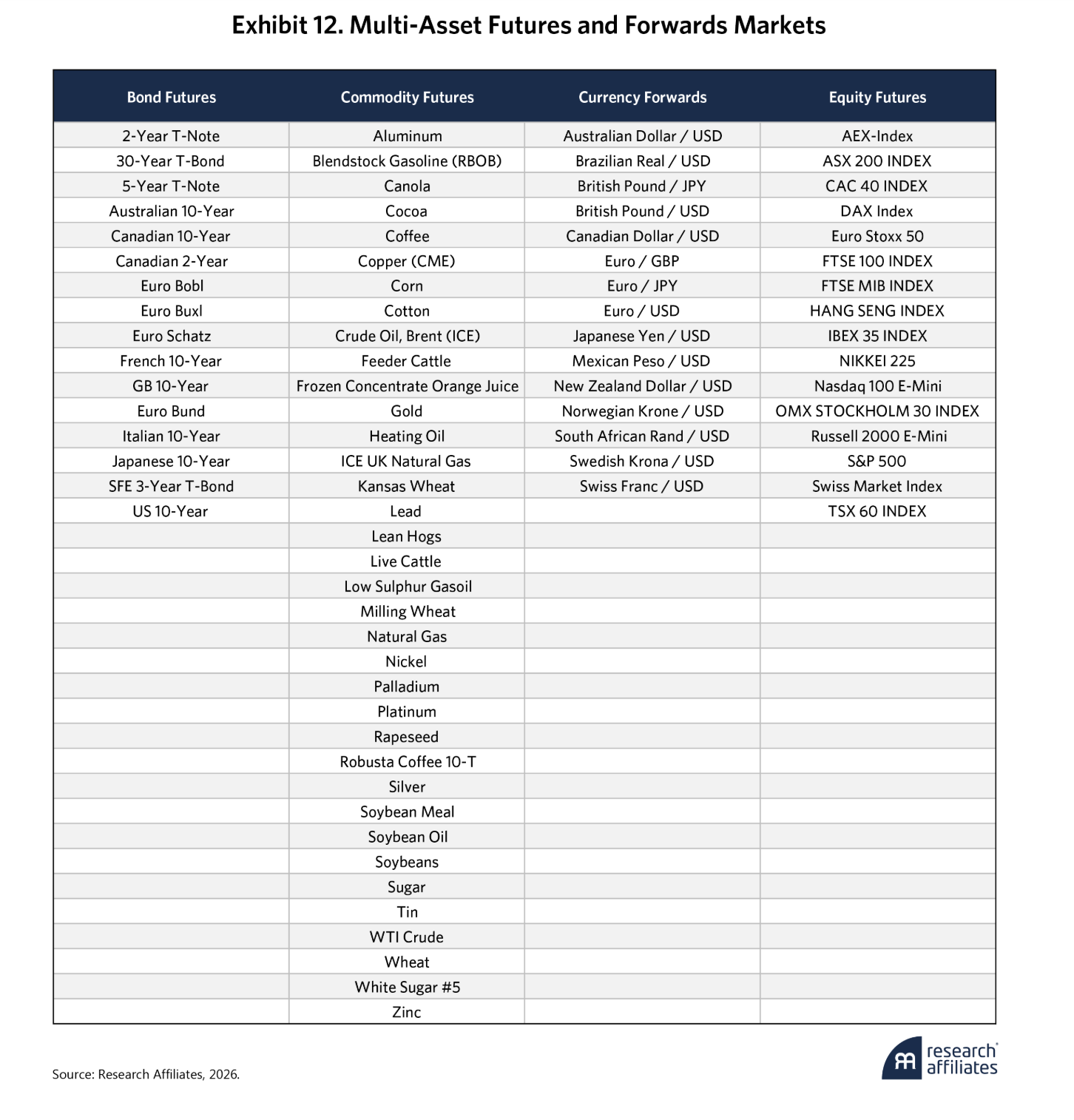

These definitions provide the foundation of our empirical analyses. Using daily data for liquid multi-asset futures and forwards from early 1989 through December 2025, we examine trend and carry characteristics across 83 contracts spanning four asset classes, specifically 16 bond futures, 36 commodity futures, 15 currency forwards, and 16 equity index futures; for additional details on the universe, please see Exhibit 12 in the Appendix.

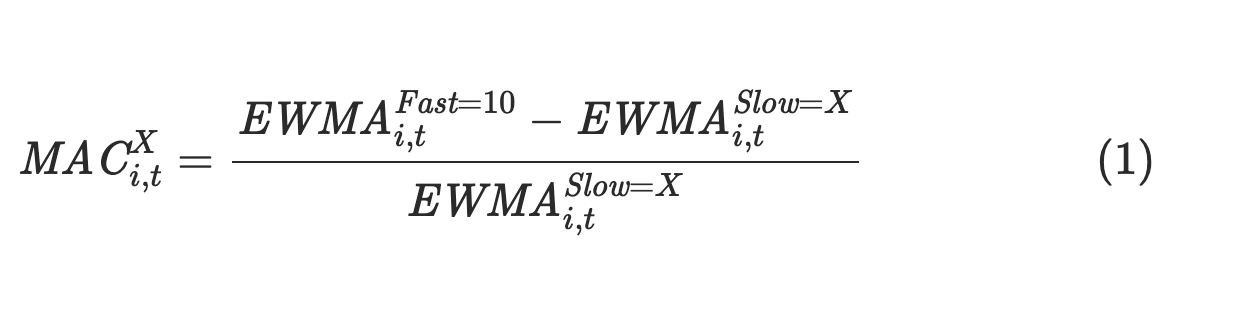

For trend signals, following Sepp and Lucic (2025), we construct various moving average crossovers (MACs) with a range of lookbacks. Other papers such as Brock, Lakonishok, and LeBaron (1992) and Levine and Pedersen (2016) also consider such signals, leaving us in good company. For robustness, we consider six versions of MAC signals, X1 to X6, all expressed as a percentage (i.e., fast moving average minus slow moving average all divided by slow moving average) and then scaled by their trailing one-year standard deviation.2 Specifically, we consider an expanding period with a fast 10-day half-life and slow half-lives between 25 (X1) and 150 (X6) days in 25-day increments. In Equation 1, the MAC signals are constructed on asset i at time t for version X (for example, X=75 days):

We define carry following Erb and Harvey (2006) and Koijen, Moskowitz, Pedersen, and Vrugt (2018). For the bond futures, it is calculated as duration-adjusted excess yield and rolldown. For the commodity futures, it is the roll between adjacent contracts (e.g., first and second). For the currency forwards, it is the interest rate differential. For the equity futures, it is futures rolldown to the spot price of the underlying indices.

Better Together? Trend and Carry’s Synergy

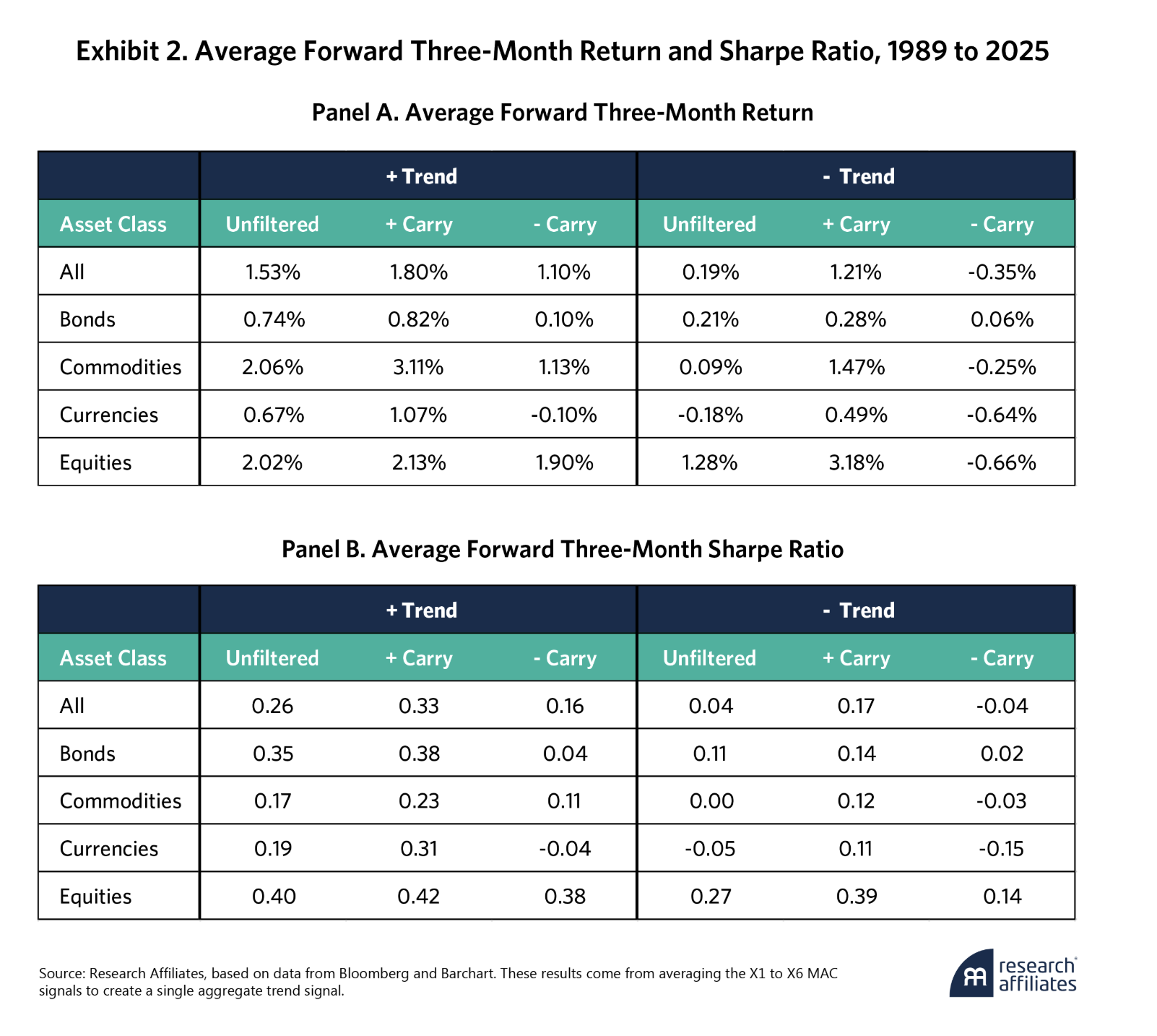

Exhibit 2 shows the average forward three-month3 return and Sharpe ratio by the sign of the trend and carry signals across our entire asset universe and each asset class.

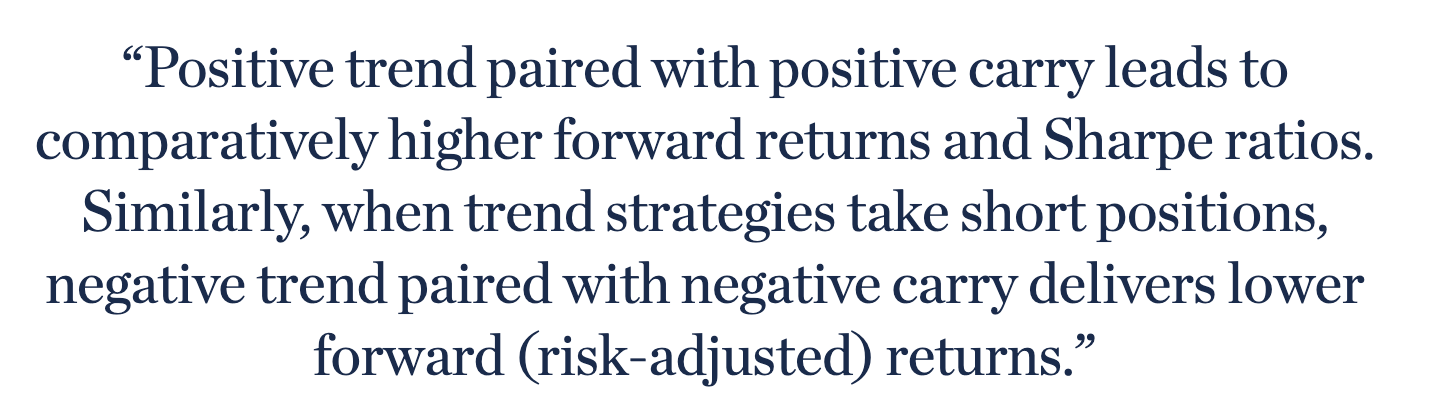

The results in Exhibit 2 emphasize Bhansali, Davis, Dorsten, and Rennison’s (2015) admonition to “be on the right side of the trend, and don’t pay too much while you are at it.” Positive trend signals paired with positive carry lead to comparatively higher forward returns and Sharpe ratios than positive trend alone. Similarly, in the negative trend case when trend strategies take short positions, negative trend paired with negative carry delivers lower forward (risk-adjusted) returns. This is exactly the benefit of conditioning on carry.

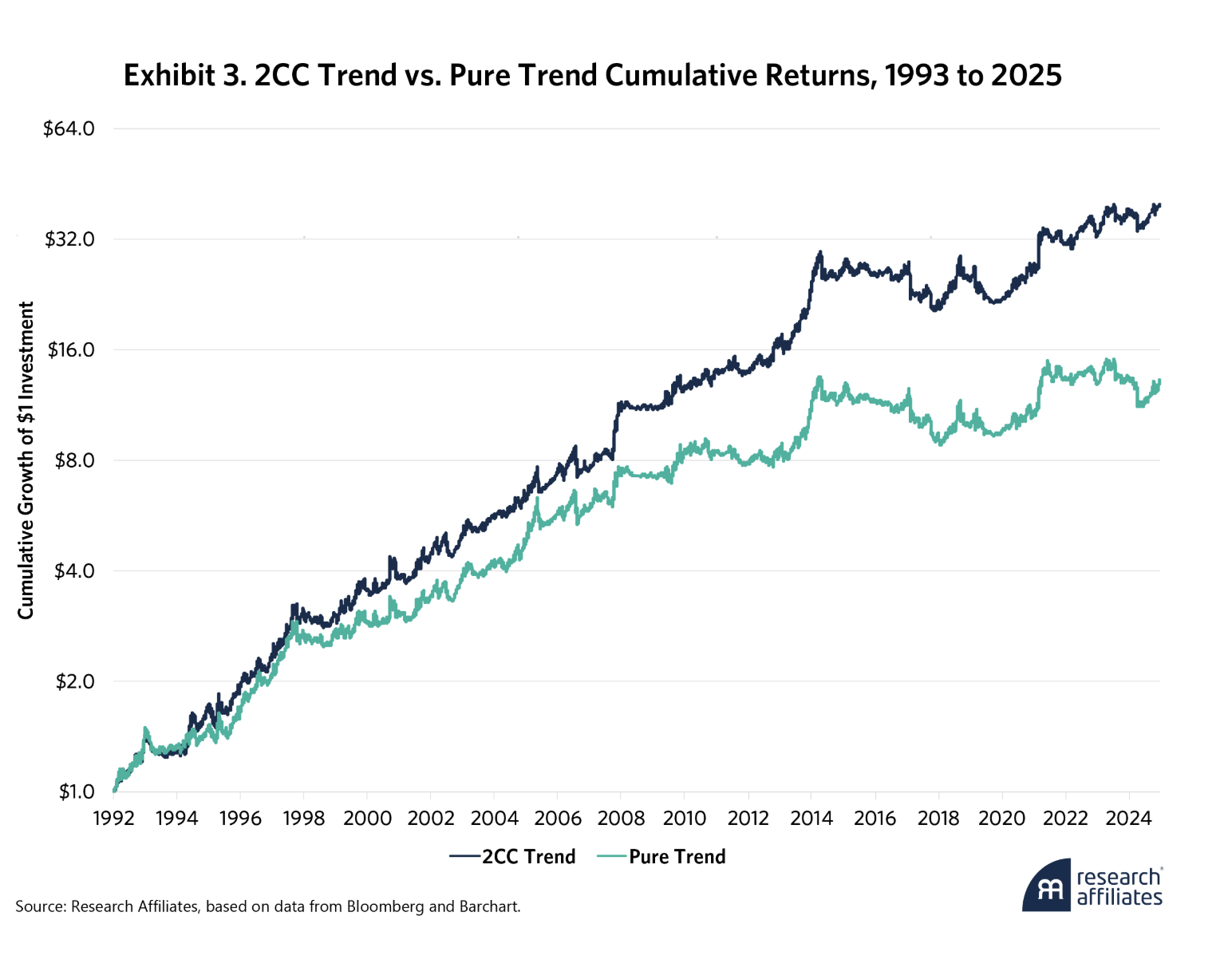

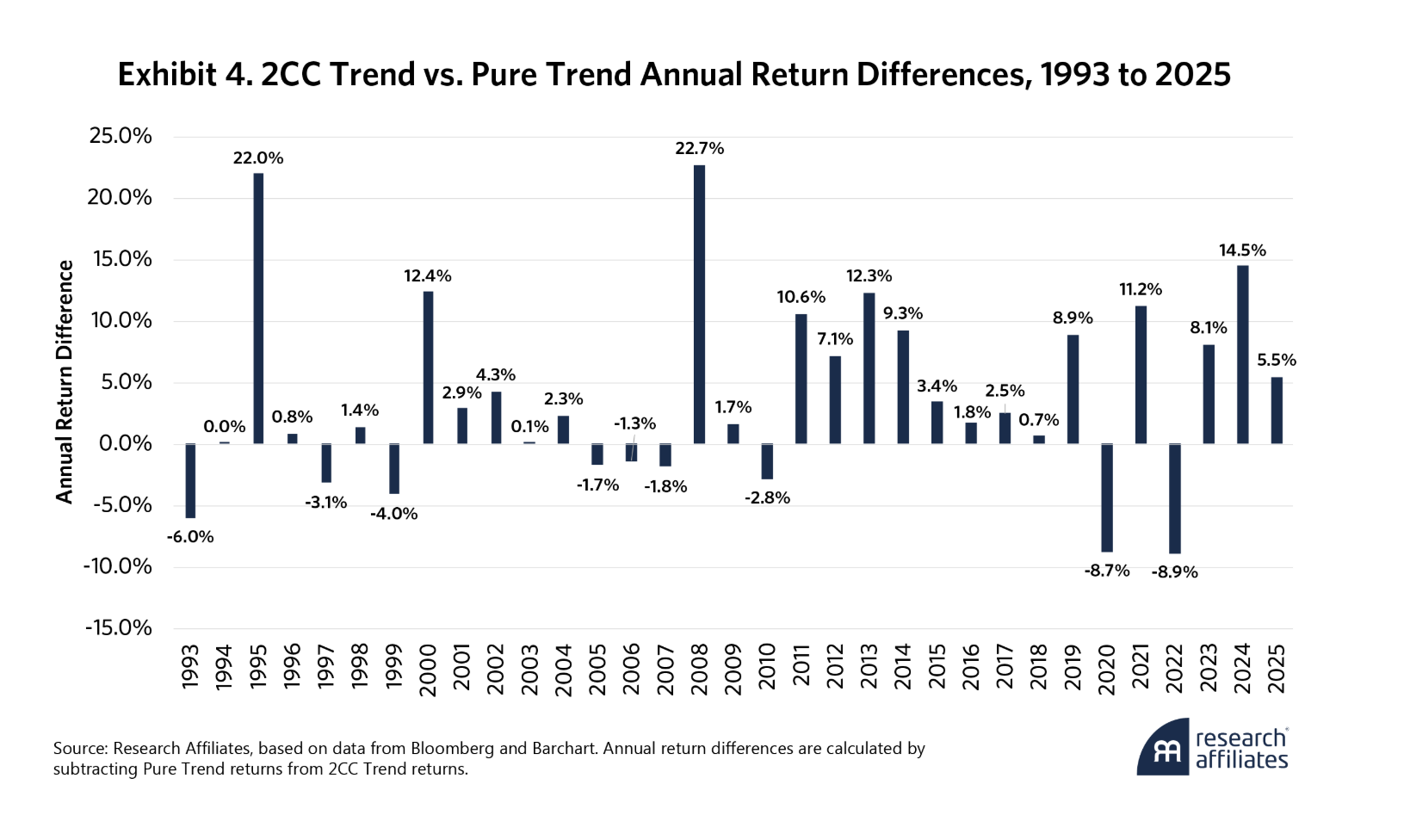

Of course, how these results manifest themselves in a portfolio context is the critical consideration. Our portfolios begin in January 1993, when at least five instruments are available in each asset class. The final trend strategies are equal risk averages of the MAC X1 to X6 portfolios targeting 10%–12% volatility. Exhibit 3 shows the cumulative returns for both Two-Sided CC (2CC Trend) and Pure Trend. Exhibit 4 compares their annual returns across all asset classes.

2CC Trend’s annualized tracking error relative to Pure Trend is about 5.5%; thus, we see that the 2CC Trend regularly outperforms the Pure Trend approach by one or two times its tracking error, with standout years in 1995 and 2008. In 2020 and 2022, however, this pattern reversed and 2CC Trend lagged Pure Trend by nearly two times its tracking error.

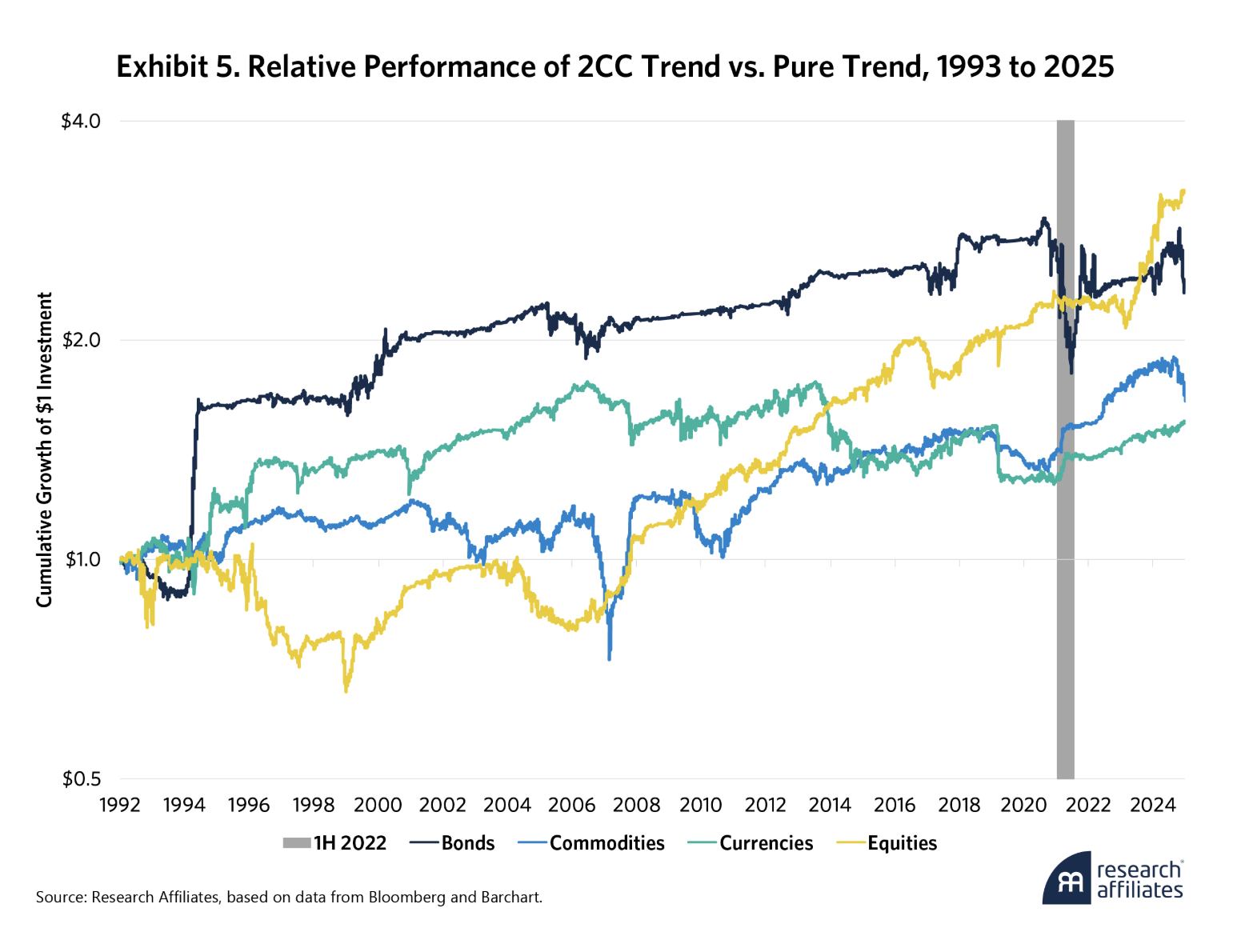

What happened? Early in 2022, very low short-term interest rates caused global yield curves to slope upward (positive carry). As the year progressed, inflation surged and longer duration yields began to rise; Pure Trend strategies shorted bonds and profited handsomely. But due to its negative carry filter, 2CC Trend was prohibited from shorting bonds – one of the strongest trend trades of the year – which was a major driver of its underperformance. Exhibit 5 shows how bonds disappointed in 2022, but also confirms 2CC Trend’s promising long-run track record versus Pure Trend across each asset class.

While it may be tempting to dismiss the headwind to 2CC Trend in 2022 as a one-off to otherwise favorable historical outperformance, we need to dive deeper to determine whether 2022 was indeed an isolated incident rather than a harbinger of things to come.

Just as bonds detracted from 2CC Trend’s relative performance in 2022, during the nine years in which 2CC Trend underperformed Pure Trend, bonds were a contributor to the underperformance in six of those, the most of any asset class. This highlights that the relationship of trend and carry in bonds has a meaningful impact on the entire strategy.

The year 2022 is important for another reason. Trend strategies are supposed to diversify against equity drawdowns. In the first half of 2022, the S&P 500 and Bloomberg U.S. Aggregate, the core of many portfolios, fell by 19.9% and 10.4%, respectively. Institutional or individual portfolios looking to access trend following’s “crisis alpha” through 2CC Trend would have been better served by adopting the Pure Trend approach.

As Masturzo (2025) points out, portfolio construction in trend following often involves a tradeoff between Sharpe ratio and skewness. To the extent that carry conditioning is one manifestation of that tradeoff, we need to better understand its role in building a trend following strategy.

It’s Complicated: Trend and Carry’s Relationship

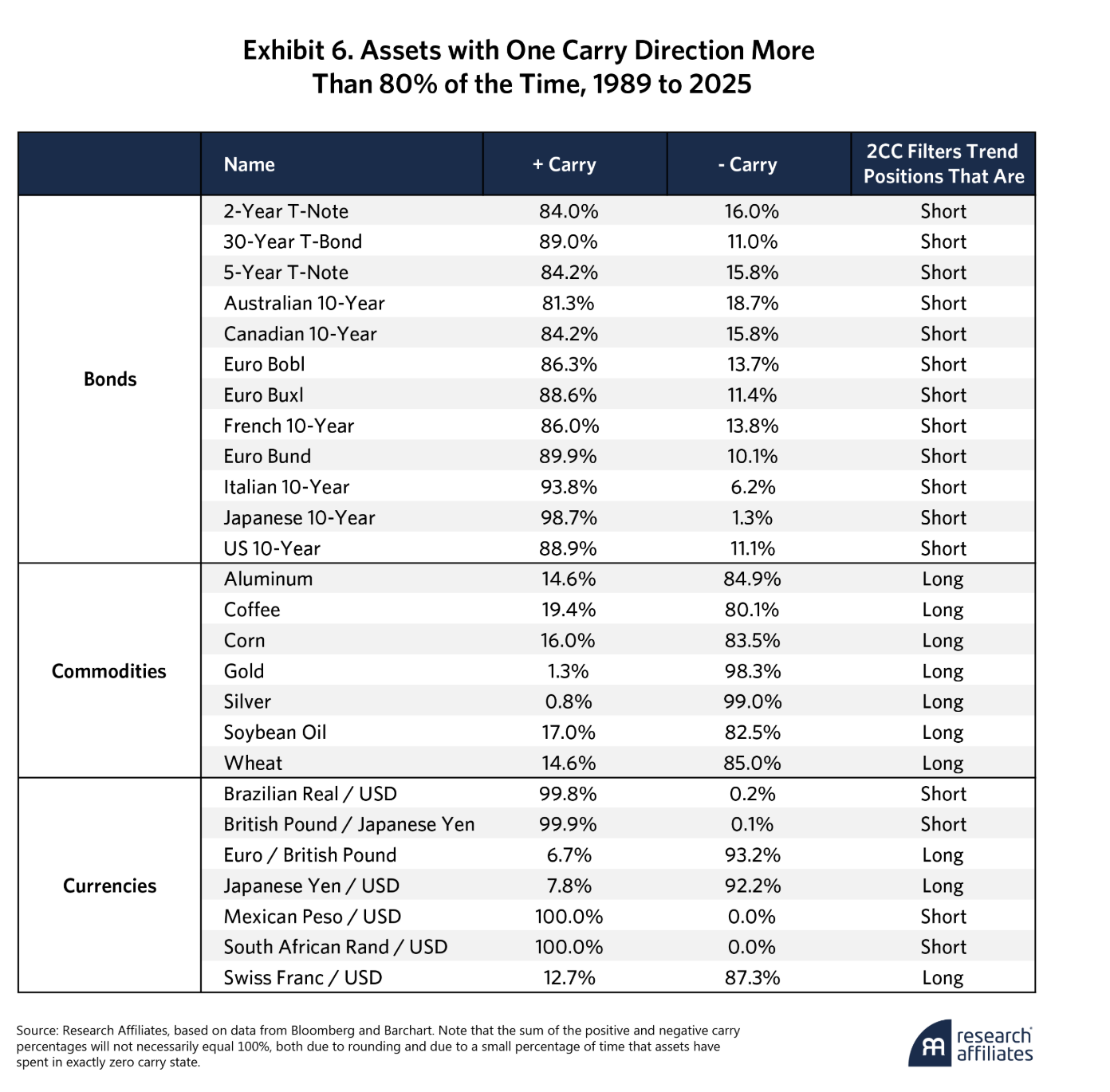

While 2CC Trend offers advantages over Pure Trend over time, the implications vary by asset class. As we noted, since precious metals mostly have negative carry, 2CC Trend cannot take long positions in those assets. Indeed, Exhibit 6 shows other similar assets, specifically 26, whose carry stances over the full sample have been concentrated at least 80% of the time in a single direction.

2CC Trend would have mostly missed the precious metals bull market that started in 2024. Moreover, while 2CC Trend restricted shorts as global interest rates fell for 40+ years, thereby boosting its performance in bonds,4 that pattern may or may not continue.

Currencies in Exhibit 6 can be further sub-divided into the emerging markets – the Brazilian real, Mexican peso, and South African rand – and the developed market crosses. The former collectively represent the classic currency carry trade, in which capital flows to countries with higher interest rates. In early 2025, when the classic carry trade faced challenges,5 2CC Trend offered no support since it filtered counter trades.

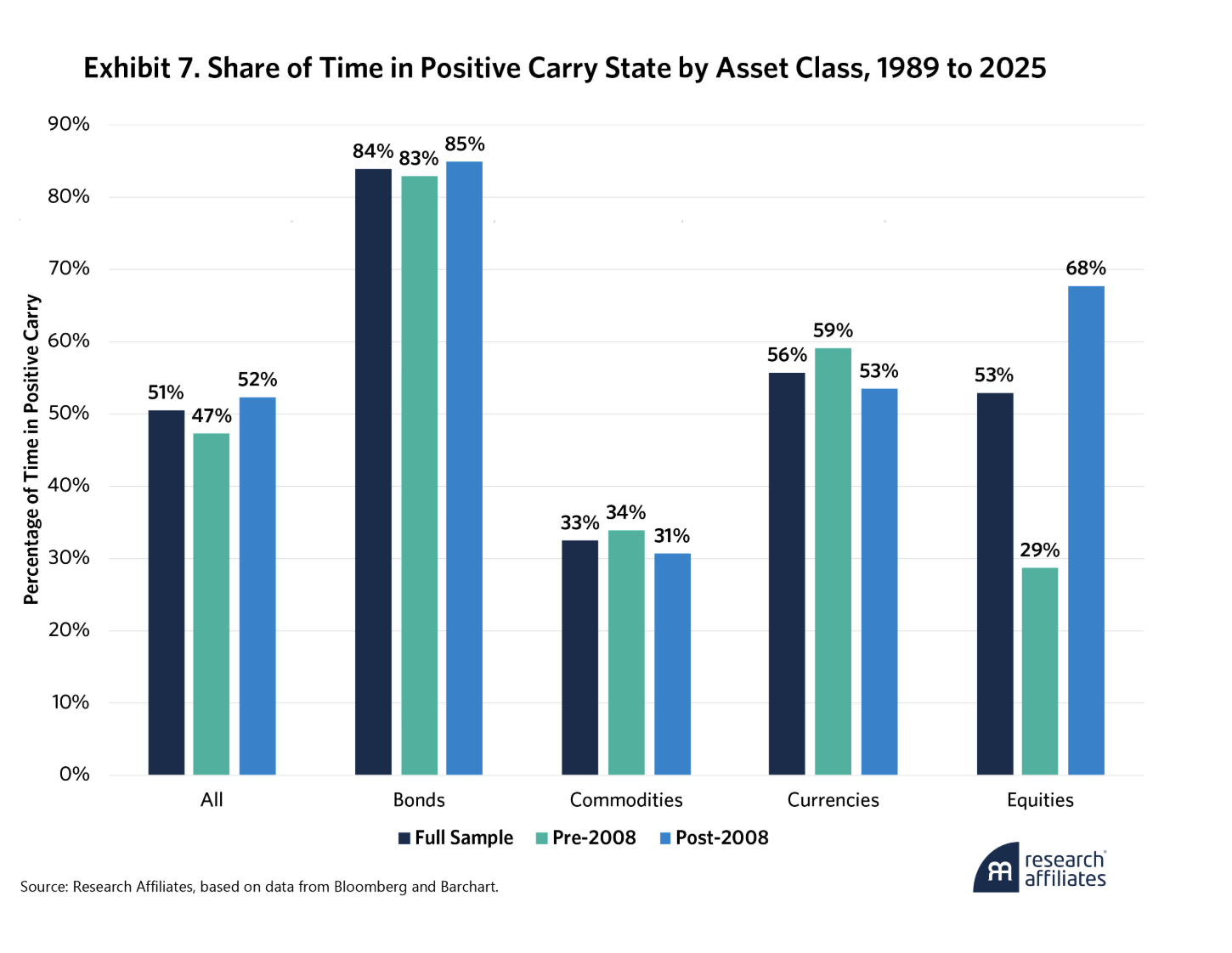

To better anticipate carry conditioning’s influence on Pure Trend, we examine carry’s evolution over time and across various assets. Exhibit 7 shows the average time asset classes spent in a positive carry state since 1989, as well as before and after the Global Financial Crisis (GFC).

The carry dynamics of equities changed more than those of the other asset classes pre- vs. post-GFC. In the post-2008 low-interest rate environment, relatively stable equity indices’ dividend yields largely eclipsed the risk-free rate. As a result, equities have been in a positive carry state more often since the GFC than during the higher interest rate environment that preceded it.

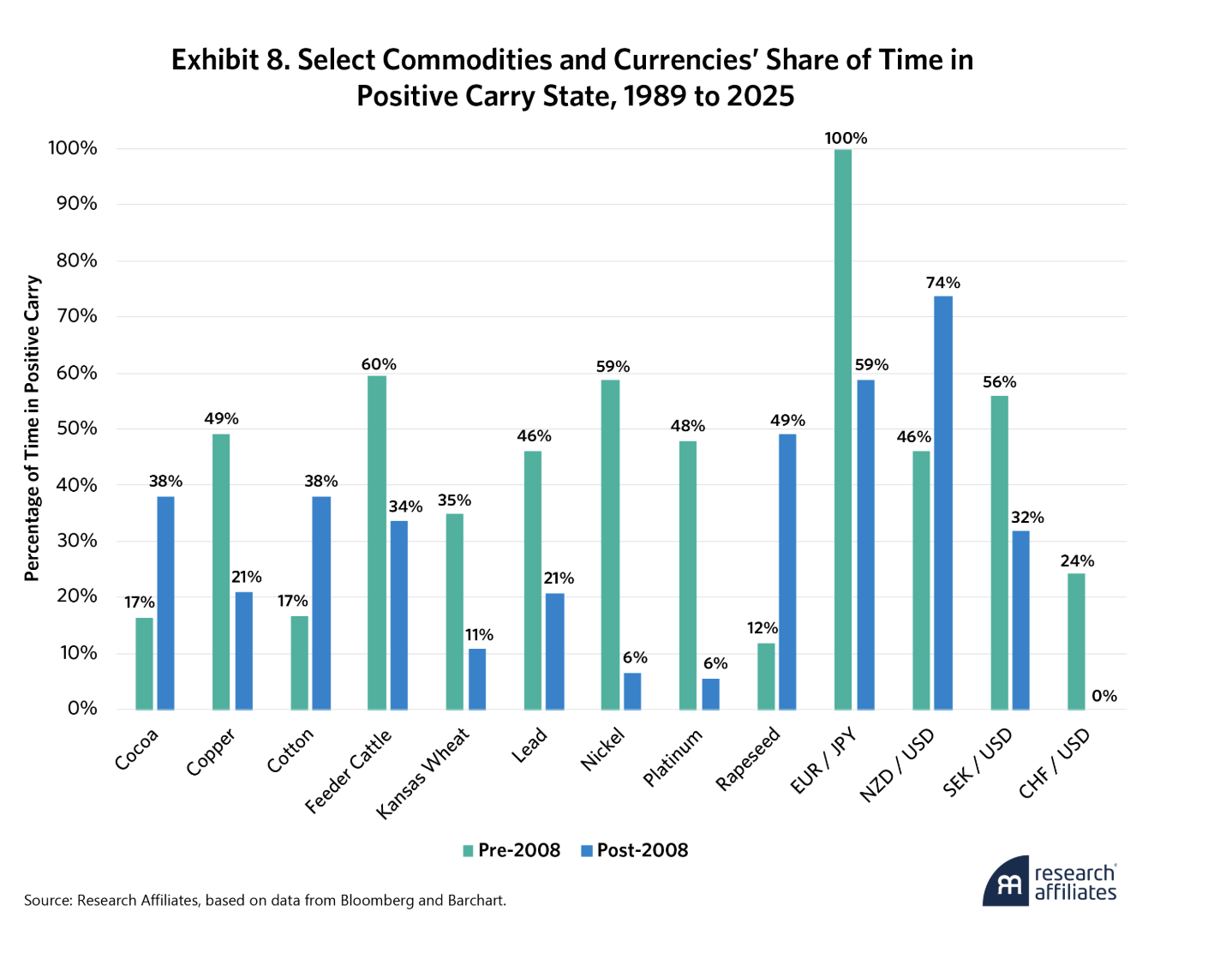

While obscured by the averages, the commodity futures and currency forwards have also undergone a large shift in several cases. Nine of 36 commodities and four of 15 currencies have seen the percentage of time spent in one direction change by at least 20% between the two periods, as shown in Exhibit 8.

The changing carry dynamics shown here for the currency forwards are of course strictly driven by interest rate differentials. Consider two representative examples: EUR/JPY and CHF/USD. Pre-2008, interest rates in Europe were higher than those in Japan persistently, averaging 5.7% for the German Bund, as one example, compared to 3.0%6 for 10-Year Japanese Government Bonds (JGBs).

After the GFC, interest rates in both Europe and Japan declined, but which was higher than the other at any given time was close to a coin toss. Extremely low interest rates also explain why the Swiss Franc has never experienced carry compared to the dollar post-2008, as interest rates in Switzerland have been materially lower than those in America.

The commodities narrative is more idiosyncratic; consider the cases of copper, lead, and nickel. As Omura and West (2015) document, storage costs for these markets increased by 91% on average from 2003 to 2013 on the London Metals Exchange. This explains the decline in the percentage of time these assets have spent post-2008 in a positive carry state compared to the pre-2008 period; the increasing storage costs overwhelmed the declining interest rate backdrop.

Carry Evolution’s Impact on Trend Strategies

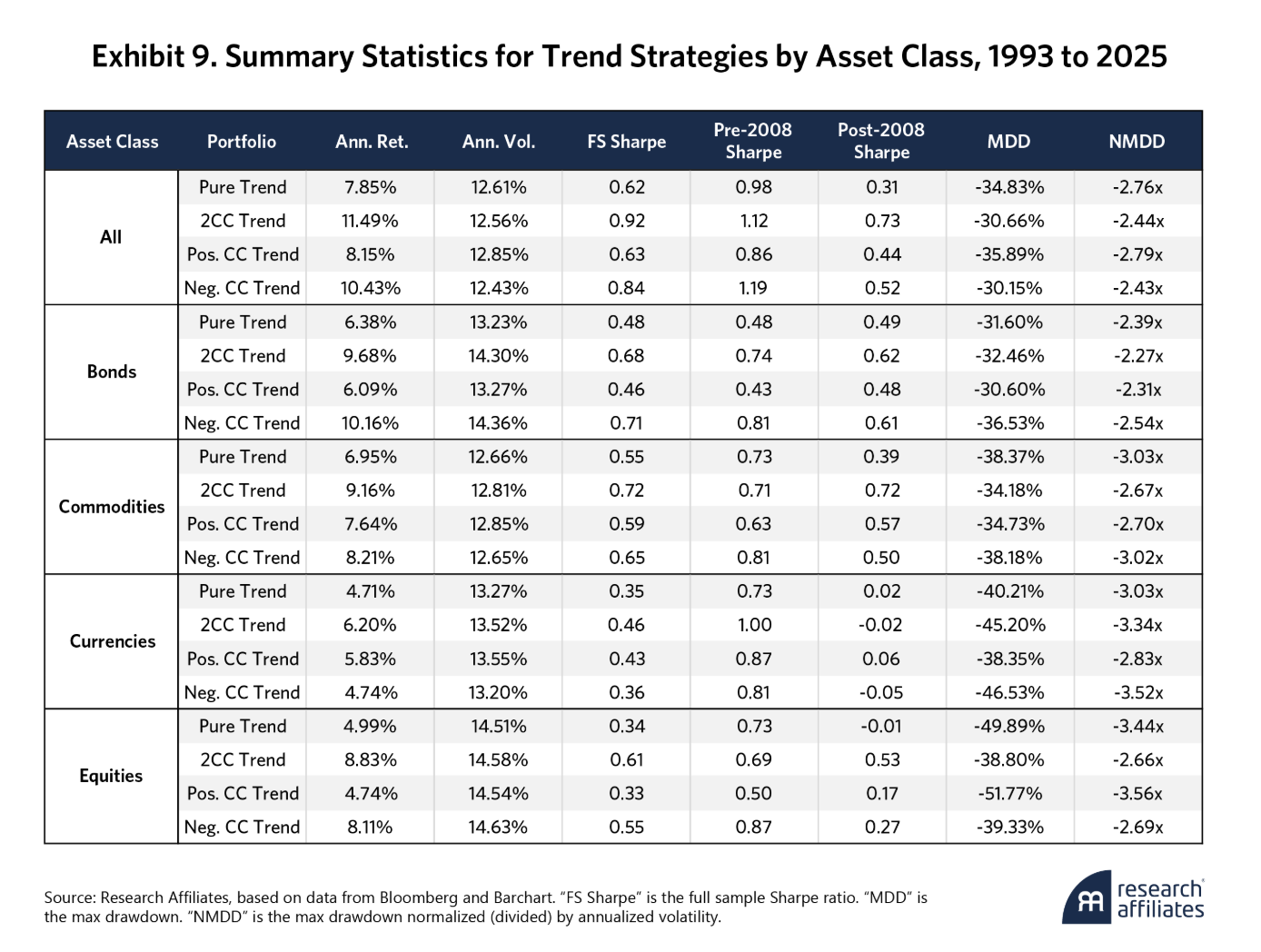

Whether these carry dynamics will continue in the future is an open question, but how these historical changes have affected trend strategies is an important consideration. Exhibit 9 shows summary statistics for trend following portfolios formed on each asset class, as well as with each type of carry-filtering system from Exhibit 1, and compares them with the Pure Trend approach.

Exhibit 9 shows how the carry dynamics in Exhibit 6, Exhibit 7, and Exhibit 8 have influenced 2CC Trend and Pure Trend asset class-by-asset class.

With their risk premium, equities mostly trend upwards, so betting against them has historically been a losing proposition. Thus, the one-sided negative carry filter, which is only short when carry is negative, was very effective. Indeed, even with the more-balanced pre-2008 equity carry posture, equities’ trend following Sharpe ratio rose from Pure Trend at 0.73 to Neg. CC Trend at 0.87. Post-2008, the effect is even more pronounced; while Pure Trend on equities stagnated for 17 years, Neg. CC Trend generated a 0.27 Sharpe ratio, which, while hardly outstanding, was certainly better than nothing! In all sub-periods, Neg. CC Trend outpaced Pos. CC Trend. This suggests trend and carry together boosted equities principally by blocking unproductive short trades.

Bonds tell a similar story. As bond futures mostly had positive carry, as Exhibit 6 and Exhibit 7 show, so filtering only positive trend signals on carry held no advantage over Pure Trend in any of the sub-periods. Instead, Neg. CC Trend performed best as avoiding shorts in a 40+ year bull market was a benefit provided by carry conditioning relative to Pure Trend.

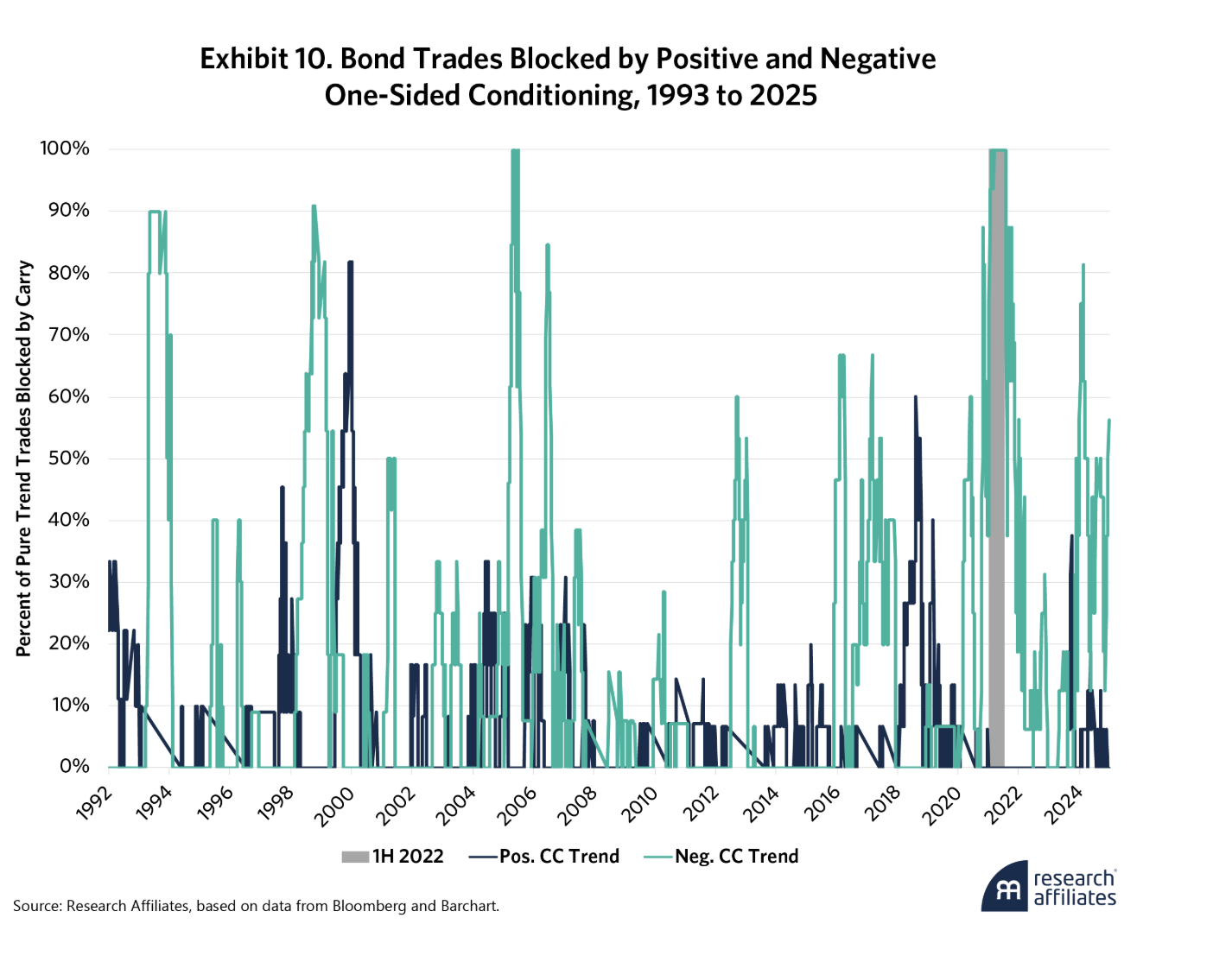

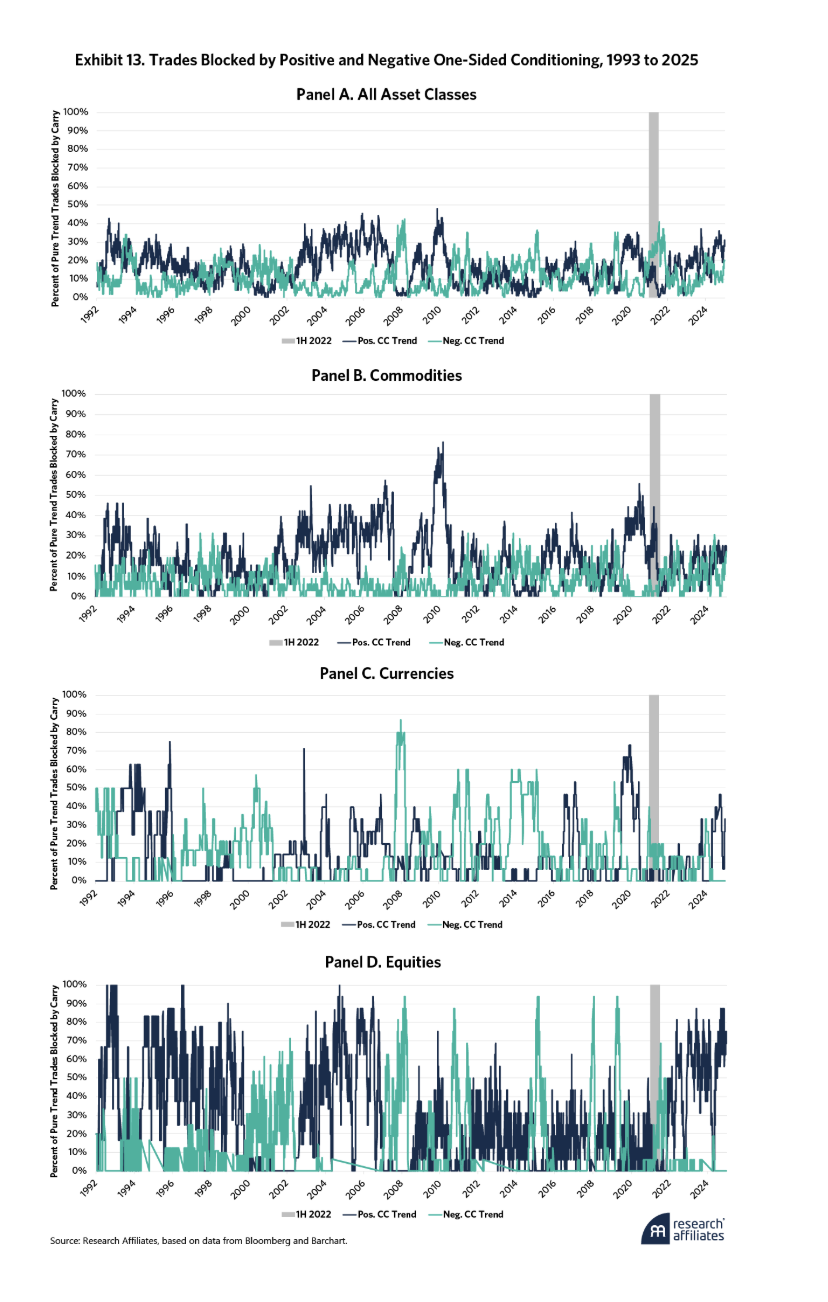

Exhibit 8’s granularity nonetheless masks the issues with bonds in 2022. How much did the filter affect bonds during the first half of 2022? Exhibit 10 shows the percentage of trades blocked by both positive and negative one-sided conditions; the spike in the first half of 2022 for Neg. CC Trend drove the underperformance. Exhibit 13 in the Appendix shows the percentage of trades blocked by the positive and negative filters for all asset classes.

Whatever the filter applied, currencies have not generated meaningful positive performance since 2008. Amid low and stable interest rates, the major crosses under consideration have shown little movement.7 Even when swimming with the carry current, trend following strategies do not fare well in mean-reverting markets.

For commodities, the idiosyncrasies of the contracts make summary judgments difficult. Nonetheless, filtering seems to have paid off regardless of the style. With a sample going back to 1877, Levine, Ooi, Richardson, and Sasseville (2018) show that the average total commodity return is much higher during periods of backwardation (i.e., positive carry) than of contango (i.e., negative carry). This provides further evidence that trading in the direction of the carry is important for fundamental reasons related to supply-demand dynamics.

Joining Trend and Carry at the Hip

The results in the last two sections demonstrate carry conditioning’s impact and emphasize two key takeaways: carry conditioning, especially one-sided conditioning in bonds and equities, has benefitted trend strategies, but various nuances can come into play when applying this filter and they need to be understood before selecting an approach.

Of course, a model that consolidates these findings can help confirm or reject the premise that carry conditioning will continue to benefit trend following strategies. For that, we need to return to our two hypotheses. First, the more carry contributes to an asset’s long-term returns, the more inclined investors should be to filter for it. For example, we know yield, and therefore carry, constitutes a large share of bond returns. Indeed, carry’s absolute value as a percentage of trailing one-year volatility in bond futures is 42.0% on average. That compares to 4.7% for commodities, 2.2% for currencies, and 3.3% for equities. Thus, carry conditioning should boost bonds more than other asset classes.

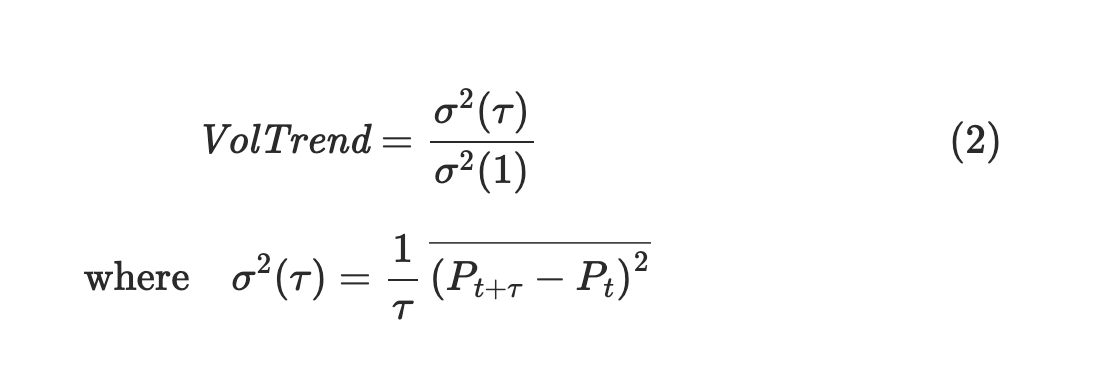

Our second hypothesis references Dao et al. (2017), who prove that trend following is explicitly a bet on long- over short-term volatility by developing a new measure, detailed in Equation 2, for the ratio of long- versus short-term variances. We call this “VolTrend.”

According to Dao et al. (2017), when VolTrend – the ratio of long- vs. short-term variance – exceeds 1, that asset is said to be “trendy,” or more formally, positively autocorrelated at the tau horizon. By contrast, when VolTrend is below 1, that asset is considered “mean-reverting,” or negatively autocorrelated at the tau horizon. When an asset’s VolTrend equals 1, the asset represents a non-autocorrelated random walk series.

If trend is a bet on long- versus short-term volatility, carry is as well. Intuitively, carry strategies perform best amid low short-term () volatility; absent near-term shocks, investors can simply collect the carry. This leads to our second hypothesis: carry conditioning’s benefits are negatively correlated to the length of a trend strategy’s lookback. The longer the lookback, the less effective the carry conditioning.

We test these hypotheses with two metrics. The first calculates how much carry contributes to an asset’s full sample return using the following formula in Equation 3:

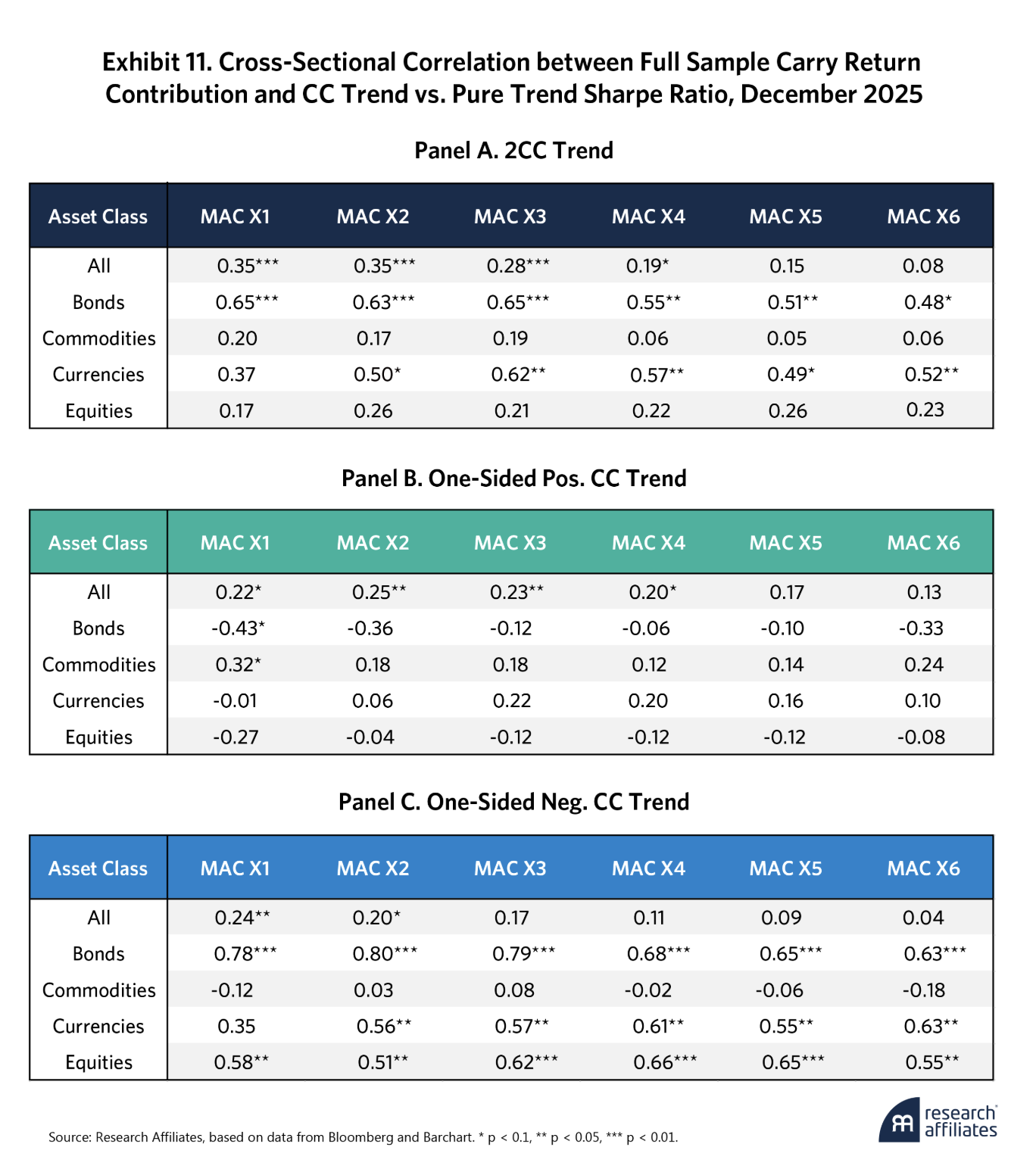

Next, we compare CC Trend and Pure Trend’s Sharpe ratio differential for each individual asset. Exhibit 11 shows the correlation of these two measures averaged across each asset class and trend horizon.

Exhibit 11 generally shows that there is a positive and at times significant correlation between carry’s return contribution and excess Sharpe ratios from conditioning on carry across all panels. The effect is strongest in bonds, especially for the two-sided and one-sided negative cases, followed by equities in the one-sided negative case. The outcome is more mixed for currencies and commodities, with filtering only additive pre-2008 in the former and post-2008 in the latter as we previously showed.

Trend and carry also have at least a marginally stronger relationship for shorter-term trend signals. CC Trend performs better for X1 than for the longer-term X6 across all asset classes and bonds in particular. For example, Panel A – the most comprehensive view – indicates a statistically significant correlation for MAC X1 to X3, but this correlation evaporates for the MAC X5 and X6 signals. The results are more mixed, however, for individual asset classes due to their smaller sample sizes.

Conclusion

Based on our findings, carry conditioning has undoubtedly enhanced returns for trend following strategies over the last few decades, with this relationship driven by the contribution of carry to an asset's return. The greater carry's contribution, the more critical it is to filter this market's trend signal with carry, with the benefits accruing mostly, albeit weakly, to shorter-term trend signals.

Nevertheless, whether to apply a naïve filtering mechanism requires keeping three factors in mind. First, interest rates have clearly influenced the average carry posture of many individual assets; that distinction is clearest pre- and post-GFC. Second, certain futures markets, such as gold and silver, have specific structural idiosyncrasies that preclude a simple uniform rule from being appropriate across all instruments. Third, conditioning on carry can cause trend portfolios to underperform at inconvenient times - during the first half of 2022, for example. In summary, carry conditioning is not a panacea; investors may therefore want to approach the filter decision from a first-principles, fundamental economic perspective.

Please read our disclosures concurrent with this publication: https://www.researchaffiliates.com/legal/disclosures#investment-adviser-disclosure-and-disclaimers.

Appendix

Exhibit 12 documents the 83 multi-asset futures and forwards we consider in this article.

Exhibit 13 shows the percentage of trades that the one-sided carry conditions blocked across all asset classes, as well as for commodities, currencies, and equities. Panel D covers equities and shows the sizeable influence of the low-interest rate environment. Prior to the Great Recession, the positive filter blocked numerous trades based on the generally negative carry posture of equities demonstrated in Exhibit 7. Through the 2010s, the percentage of trades blocked by the positive filter declined precipitously, only to rise again as global interest rates started to rise in late 2021 and early 2022. The negative filter, on the other hand, proved its value during the short and infrequent (albeit sharp) drawdowns of the 2010s; by blocking short trades, the filter boosted the trend portfolio since most of these drawdowns reversed and turned into upswings.

End Notes

1. As is standard for trend managers, we exclusively consider trading futures and forwards.

2. This approach maintains the long-run drift inherent in each asset’s trend signal. For example, given their exposure to the equity risk premium, equities tend to rise, so their normalized trend signals are positive on average. For robustness, we also considered de-meaning our MAC X1 to X6 signals to strip out long-term risk premia so that a trend following portfolio would not be biased toward asset classes and instruments that tend to go up (or down) over time. We do not report these results because they do not affect our conclusions.

3. This horizon matches the median trade length for a simple binary strategy on the trend signals in our panel over the full sample, which ranges from 48 (MAC X1) to 81 days (MAC X6).

4. Indeed, shorting Japanese bonds over this period was dubbed the “widowmaker” trade.

5. Please see “Carry Trade Destruction” for more details.

6. German Bund data available at https://fred.stlouisfed.org/series/IRLTLT01DEM156N, and 10-Year JGB data available at https://fred.stlouisfed.org/series/IRLTLT01JPM156N. We only considered the period from January 1989 onwards, to match the rest of our data.

7. Please see Babu et al. (2020) for additional details on trend following’s poor performance during this period.

References

Babu, Abhilash, Brendan Hoffman, Ari Levine, Yao Hua Ooi, Sarah Schroeder, and Erik Stamelos. 2020. “You Can’t Always Trend When You Want.” The Journal of Portfolio Management 46 (4), 52–68.

Bhansali, Vineer, Josh Davis, Matt Dorsten, and Graham Rennison. 2015. “Carry and Trend in Lots of Places.” The Journal of Portfolio Management 41 (4), 82–90.

Brock, William, Josef Lakonishok, and Blake LeBaron. 1992. “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” The Journal of Finance, 47 (5), 1731–1764.

Dao, Tung-Lam, Trung-Tu Nguyen, Cyril Deremble, Yves Lempérière, Jean-Philippe Bouchaud, and Marc Potters. 2017. “Tail Protection for Long Investors: Trend Convexity at Work.” Journal of Investment Strategies 7 (1), 61–84.

Erb, Claude B., and Campbell R. Harvey. 2006. “The Strategic and Tactical Value of Commodity Futures.” Financial Analysts Journal 62 (2), 69–97.

Koijen, Ralph S. J., Tobias J. Moskowitz, Lasse Heje Pedersen, and Evert B. Vrugt. 2018. “Carry.” Journal of Financial Economics 127 (2), 197–225.

Levine, Ari, and Lasse Heje Pedersen. 2016. “Which Trend Is Your Friend?” Financial Analysts Journal 72 (3), 51–66.

Levine, Ari, Yao Hua Ooi, Matthew Richardson, and Caroline Sasseville. 2018. “Commodities for the Long Run.” Financial Analysts Journal 74 (2), 55–68.

Masturzo, Jim. 2025. “Walking the Tightrope: Trend Following’s Tricky Tradeoffs.” Research Affiliates.

Molyboga, Marat, Junkai Qian, and Chaohua He, 2020. “Carry and Time-Series Momentum: A Match Made in Heaven.” The Journal of Alternative Investments 23 (2), 84–93.

Omura, Akihiro, and Jason West. 2015. “Convenience Yield and the Theory of Storage: Applying an Option-Based Approach.” The Australian Journal of Agricultural and Resource Economics 59 (3), 355–374.

Sepp, Artur. 2025. “The Science and Practice of Trend-Following Systems.” SSRN 3167787.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Research Affiliates

Read more commentaries by Research Affiliates