Private markets were historically for institutional and ultra-high-net-worth investors. Today, that exclusivity is breaking down, as many retail investors realize the value behind private markets and advisors look for additional diversification tools. Outside of other structures like interval funds and feeder funds, ETFs remain a convenient and familiar choice.

What’s Driving the Push for Democratization?

Public markets have become more concentrated (just think about the technology tilt of broad equity indexes — the GICS technology is over 1/3 of the S&P 500), which makes owning the market feel less comprehensive than it used to. Private markets can offer exposure to diverse opportunities and the potential for excess returns. A key feature is the illiquidity premium. Illiquidity is not necessarily a bad thing if you have a tolerance for long-term time horizons. Markets often reward investors for locking up capital over long-term time horizons rather than panic selling before investment themes materialize.

The ETF Wrapper Is Still Crucial to Understand

Private markets aren’t just private versions of stocks and bonds. They come with different mechanics and valuation methods. Democratization is an attempt to translate those mechanics into something more accessible while still making sense for the wrapper.

That’s why the most common structures have been semi-liquid registered structures like interval funds rather than ETFs. Interval funds are designed to hold more illiquid assets. In exchange, they do not offer daily liquidity (instead, repurchases happen at preset intervals and in limited quantities). And that’s also why one of the biggest questions now is: How far can you push private assets into vehicles that investors expect to behave like ETFs?

Still, you can’t ignore ETFs as an important part of this industry. After all, many investors and advisors are more familiar and comfortable with the ETF structure. Several ETFs have taken indirect routes through equity investments of private managers or through ETFs of BDCs. Meanwhile, a milestone launch of the SPDR SSGA Apollo IG Public & Private Credit ETF (PRIV) in February 2025, due to the higher limit of private market securities, was made possible through a relationship with Apollo.

What Next? Opportunities for Investors (and for ETFs)

We’re still in the early innings of private credit, and many investors may still be exploring allocations in small percentages. This isn’t necessarily wrong, but I believe private market investment will become more strategic and longer-term.

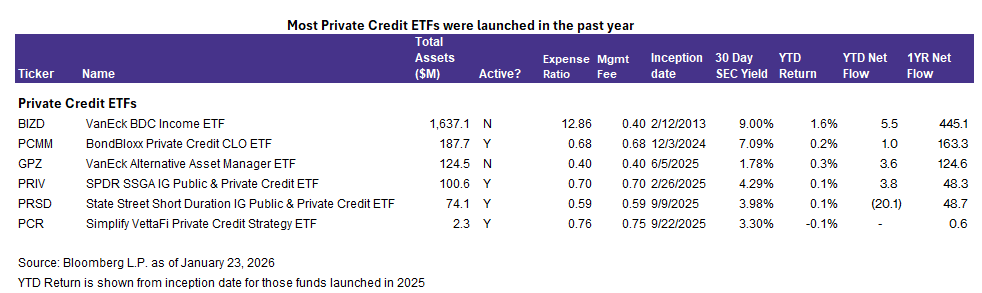

Early demand across the ETF wrapper has been uneven but still significant, showing us a slow-yet-growing adoption curve. The amount of private market ETFs has surged over the past few years as many investors look for new ways to access the strategy. Several strategies exist. They include: 1) accessing through a funds-of-funds structure with closed-end funds and BDCs; 2) accessing through investing in publicly listed private managers; and 3) using specialized strategies. Note that this list is of private credit ETFs only. It isn’t entirely comprehensive, since there are several other ETFs that follow the first strategy of holding BDCs and CEFs. I don’t include those in my list.

- The VanEck BDC Income ETF (BIZD) invests in an index of business development companies that lend to small and midsize private companies. While BIZD seems to have a massive fee (12.86%), the acquired fund fees and expenses (AFFE) are 12.44%. Investors do not pay these fees directly as an extra line item. Rather, they are already deducted from expenses. Its management fee is 40 basis points, which is about in line with its peers.

- The SPDR SSGA IG Public & Private Credit ETF (PRIV) includes private credit (alongside public), using liquidity arrangements intended to support creations/redemptions while complying with liquidity rules. Its most unique feature is access to Apollo-sourced private credit, with an explicit daily firm-bid/repurchase arrangement on those holdings, designed to help manage liquidity within a ’40 Act ETF. The State Street Short Duration IG Public & Private Credit ETF (PRSD) follows a similar strategy but focuses on short duration of one to three years.

- The BondBloxx Private Credit CLO ETF (PCMM) is an actively managed ETF that invests in private credit collateralized loan obligations (CLOs). The majority of each CLO consist of a pool of loans to private companies. The fund’s structure brings ETF benefits — transparency and cost efficiency — around an otherwise-hard-to-access asset class, with Macquarie Asset Management as subadvisor. Macquarie’s credit division brings additional expertise and investment experience to this fund.

- The VanEck Alternative Asset Manager ETF (GPZ) tracks an index of alternative asset managers across private equity, venture capital, private credit, private real estate, and private infrastructure. This picks-and-shovels approach to private credit (and other private markets) simplifies holdings down to traditional equities of managers like Apollo Global Management (APO), Ares Management Corp (ARES), and Blackstone Inc (BX).

- The Simplify VettaFi Private Credit Strategy ETF (PCR) is the newest of the group. PCR brings a specialized strategy to the traditional fund-of-funds approach. It provides exposure to publicly traded BDCs and CEFs that hold private credit (i.e., the BDC or CEF holds over 50% of its portfolio in private credit) through swaps alongside a credit hedge strategy to mitigate adverse credit events. Because PCR seeks exposure primarily through swaps, its expense ratio (76 basis points) is more aligned with derivatives-based funds. It’s also considerably lower than many true ETFs of CEFs. Those have fees in the 200–300 basis points range (that includes AFFE, however). For more details on PCR, see my research coverage of its launch here.

Bottom Line

Private markets access is moving from a niche idea to a mainstream portfolio conversation, especially as investors and advisors look for differentiated building blocks outside of the 60/40 portfolio. ETFs can be an efficient democratization vehicle. However, they also force us to consider expectations of pure-play exposure, daily liquidity, and transparent pricing.

For more news, information, and analysis visit the Thematic Investing Content Hub.

Originally published on ETF Trends

VettaFi LLC (“VettaFi”) is the index provider for PCR, for which it receives an index licensing fee. However, PCR is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of PCR

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi