As the final quarter of 2025 begins, it's a critical moment to look back at the preceding three quarters. Each year carries its own narrative, and 2025 was no exception. Markets trended downward early in the year owing to trade-talk-driven uncertainty, reaching a crescendo in volatility following the unexpected announcement of significant tariffs in April. Once these proposed tariffs were eased, markets climbed sharply, and by now, indices sit close to their historical peaks.

While the events of three quarters are unlikely to prompt sweeping strategic changes for those with a 10-year investment horizon, investors should use this time to evaluate whether their portfolios navigated 2025’s volatility as intended—assessing if both return and risk met their expectations. The performance of Research Affiliates’ model portfolios through this period offers a valuable case study.

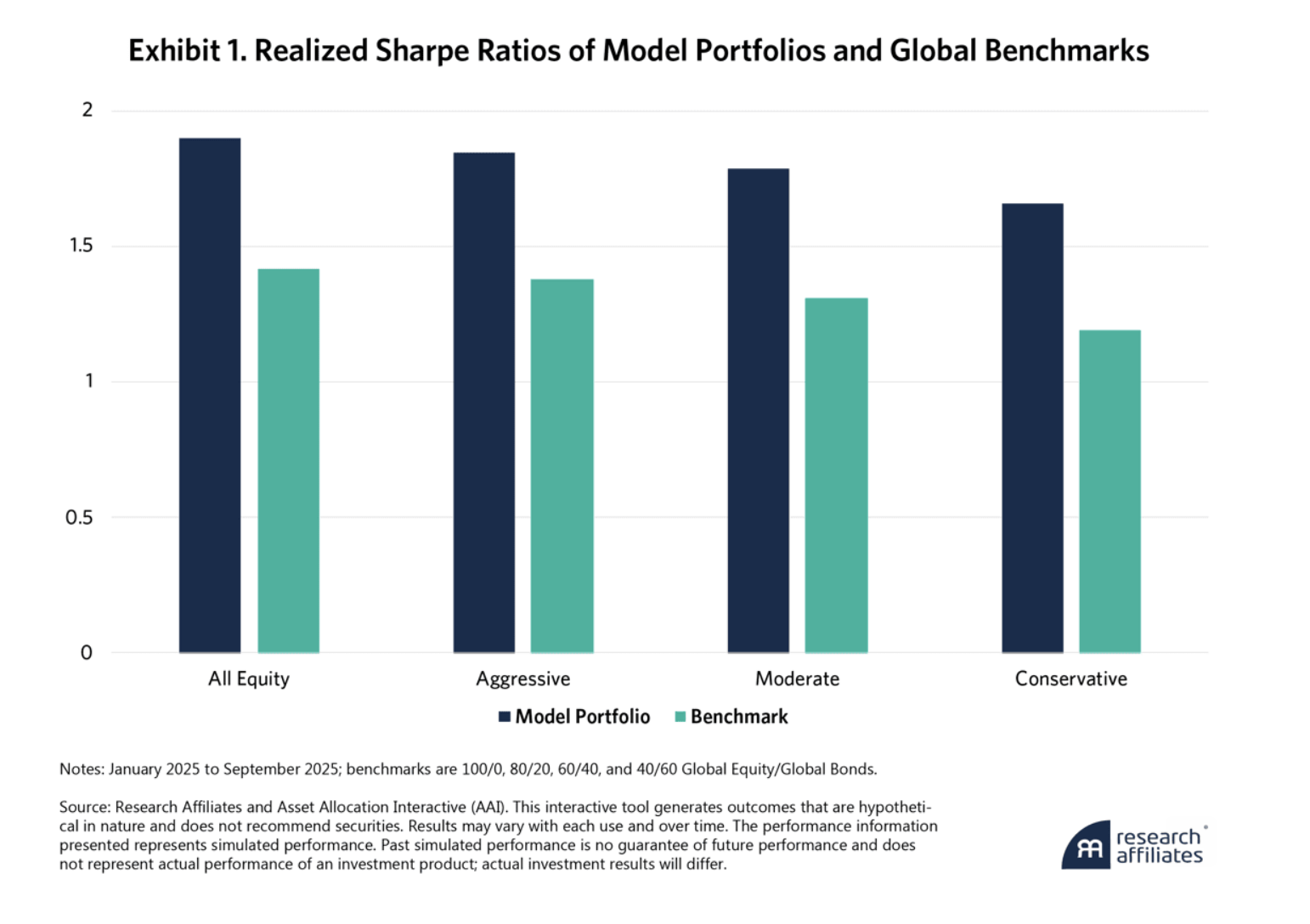

Exhibit 1 shows that the market environment thus far in 2025 has provided a tailwind to the model portfolios. On a risk-adjusted basis, all four models across the risk spectrum – conservative, moderate, aggressive, all equity – have outperformed their respective benchmarks.

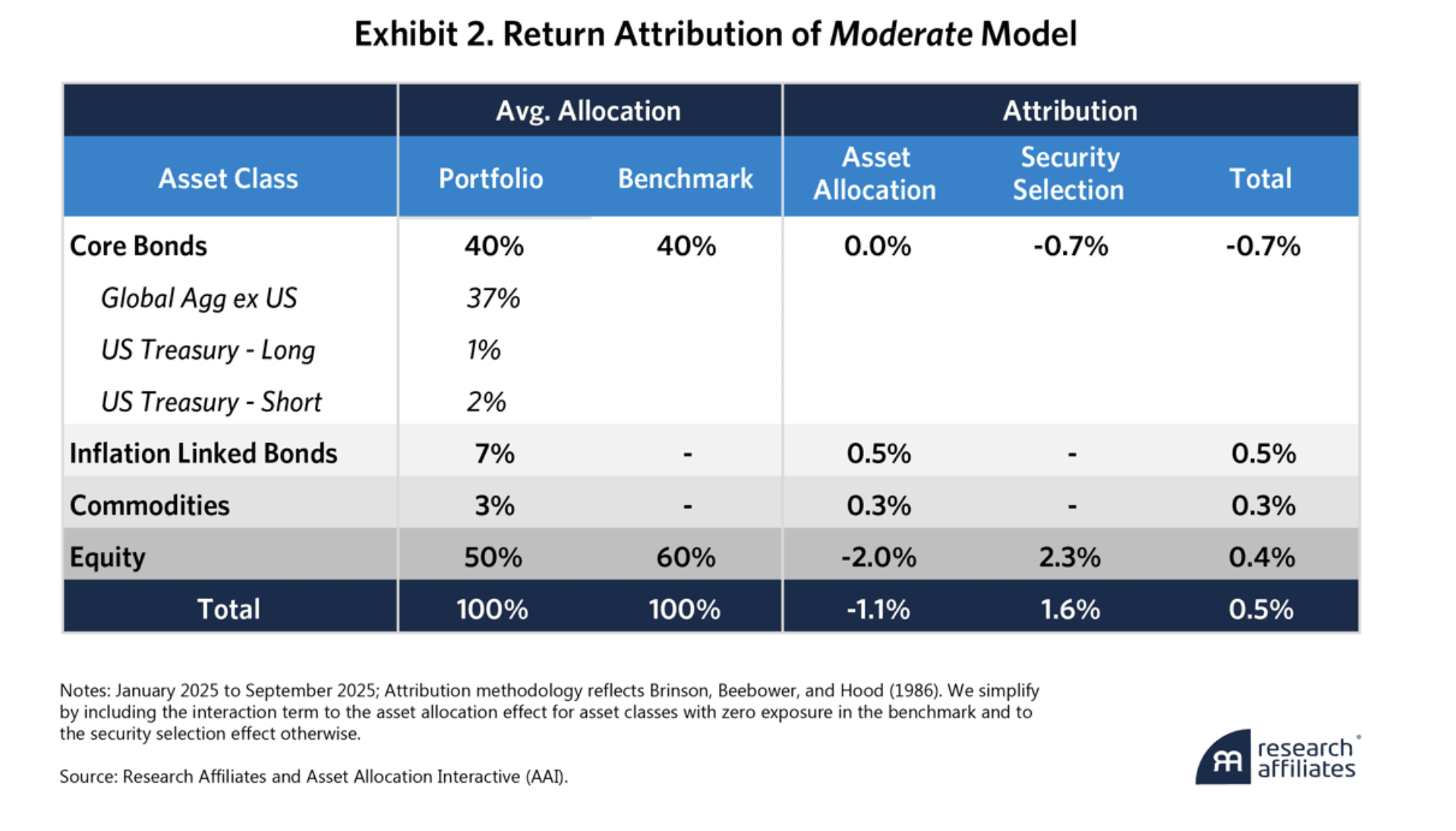

To understand the sources of outperformance, Exhibit 2 shows the return attribution of the Moderate model portfolio versus the global 60/40 benchmark portfolio. Compared to the benchmark, the model underweighted equities in favor of inflation-linked bonds and commodities. Under-allocating to equities had an adverse asset allocation effect given the strong stock rally, but the security selection effect more than offset this by allocating to outperforming equity markets versus the benchmark. While maintaining a comparable core bond allocation, the model portfolio overweighted global bonds relative to US bonds, which led to a negative security selection effect.