Hints of reforms to ease foreign-ownership limits in Saudi Arabia set off the sharpest rally for its equity market in years this autumn,1 reigniting investor curiosity. The prospect of lifting the 49% cap has already boosted sentiment and, if realized, could channel billions in passive inflows and deepen the Kingdom’s liquidity base.

While no formal policy has yet been enacted, the Capital Market Authority (CMA) has begun consulting on a draft framework that could allow greater direct foreign access to Saudi equities. The move reflects a broader shift: The Kingdom is actively positioning itself to integrate more fully with global capital markets.

For global investors, these indicators point to a market still in transition—but increasingly open, liquid and institutionally credible. In the one month since the reform news, Saudi Arabia’s equity market has outperformed that of other major oil-producing nations, up 1.1% compared to Canada, Brazil and China, which all showed relatively flat or negative returns for the period.2

Saudi Arabia’s new Investment Law, effective as of February 2025, has enshrined equal treatment for foreign and domestic investors and has streamlined registration, and—with CMA updates—is demonstrating clear intent to align with global capital-flow standards.

Meanwhile, the Kingdom’s Vision 2030 giga-projects—from NEOM and Qiddiya to Soudah Peaks—continue to drive diversification. Its Public Investment Fund (PIF), with assets around US$900 billion, anchors this transformation and attracts global capital. At the same time, investment in renewables and hydrogen underscores the shift toward energy diversification, offering index investors exposure beyond oil.

Cooperation and economic growth among Gulf nations also stand to be amplified by Saudi Arabia’s capital projects, Qatar’s gas expansion and Kuwait’s policy reforms, with consumption in Saudi markets particularly robust.

Within the Gulf Cooperation Council (GCC), Saudi Arabia remains the most dynamic equity market, yet we believe its approximately 4% weighting in the FTSE Emerging Markets Index understates its significance.3 As new listings, privatizations and ownership reforms expand the investable universe, Saudi Arabia’s influence on regional and global benchmarks could gradually rise.

Even under current limits, many large capitalization companies have foreign holdings under 15%.4 Easing or removing the foreign-ownership cap could unlock latent demand and prompt upward repricing. Regional cooperation and strong consumption trends add further tailwinds. While policy shifts remain a risk, we believe this ongoing liberalization—involving social reforms such as greater female workforce participation—continues to spur growth drivers in retail, real estate and services.

Fiscal and market backdrop

Saudi Arabia recorded a first quarter 2025 deficit of US$15.6 billion, reflecting accelerated Vision 2030 spending. The 2025 budget projects a full-year shortfall of roughly US$27 billion, about 2.3% of gross domestic product—modest by emerging-market standards.5 Additionally, credit ratings agency S&P Global raised its long-term rating to A+ from A with a stable outlook in March 2025.

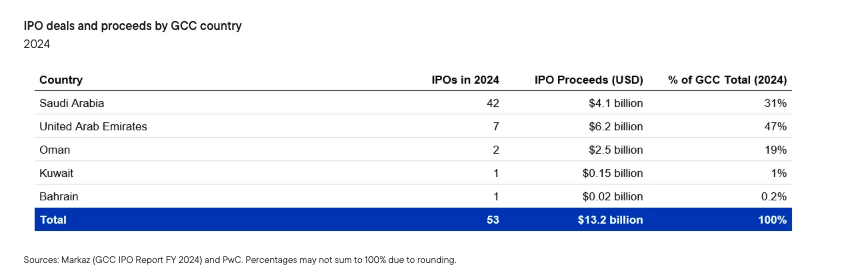

From the investor perspective, Saudi Arabia’s fiscal stance reinforces the broad reform narrative: state-led investment, healthy reserves and rising liquidity continue to underpin growth. Riyadh’s equity market activity has also accelerated, with a steady pipeline of initial public offerings (IPOs) and secondary offerings broadening the investable universe. Yet, its benchmark weighting still understates Saudi Arabia’s scale and structural potential.

As of mid-2025, however, foreign investors held about US$105 billion in Saudi equities—only a fraction of total market value—underscoring both limited participation and room for growth.6 During the first quarter of the year, oil revenues also fell roughly 18% year-on-year and fluctuations in global crude prices and OPEC+ production quotas directly affect fiscal balances, potentially more than policy adjustments can offset.7 Non-oil income rose about 2%, representing about 43% of government revenue for that quarter.8 These figures point to diversification progress, but also to concerning reliance on hydrocarbons and execution risk around major projects.

With a broader capital base and deepening corporate sector, Saudi Arabia is steadily gaining weight in emerging-market portfolios. Still, sentiment will hinge on oil prices, policy consistency and global liquidity. While risks persist, we believe the Kingdom’s market trajectory increasingly merits a fresh look from global investors.

Endnotes

1 Source: “Saudi bourse climbs back with third-quarter rally.” AGBI. October 2, 2025.

2 Source: Bloomberg. As of September 30, 2025-October 31, 2025. The FTSE RIC Capped Net Tax Indexes represent the performance of their respective countries’ Large- and mid-capitalization stocks. Securities are weighted based on their free-float-adjusted market capitalization and reviewed semiannually. Net Tax indicates that the index's performance is calculated after accounting for the net withholding tax on dividends received by a US Regulated Investment Company. Past performance is not an indicator or a guarantee of future performance. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

3 Source: Bloomberg. The FTSE Emerging Markets Index is a free-float adjusted market-capitalization weighted index that tracks the performance of large- and mid-cap companies in emerging market countries.

4 Source: “Saudi shares jump by most in 5 years on report of easing of foreign ownership rules.” Reuters. September 24, 2025.

5 Sources: “Saudi Arabia approves 2025 state budget, forecasts $27bn deficit.” Gulf Business. November 27, 2024. “Saudi Arabia posts $15.6bn budget deficit in Q1 with resilient non-oil growth.” Arab News. May 5, 2025.

6 Source: “Foreign investors own SR 394.58 bn in Saudi equities as of June 12, 2025.” Arab News. June 18, 2025.

7 Source: “Quarterly Budget Performance Report – Q1 2025.” Saudi Ministry of Finance.

8 Source: Ibid.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Franklin Templeton

Read more commentaries by Franklin Templeton