Artificial intelligence technology is starting to drive profound change for the economy, including in business capital and labor investment decisions. As we discuss in our latest Cyclical Outlook, “Tariffs, Technology, and Transition,” tariffs appear to be accelerating AI implementation as firms race to find new business opportunities amid shifting supply chains, and to offset higher costs through labor-shedding productivity gains.

Yet many people are wondering how much of the future value of AI (for companies, individuals, and the broader economy) is already priced into the current valuations.

This technology is moving quickly, with most businesses only in the early stages of understanding its capabilities. Whether and how fast AI can unlock new, transformative, lucrative idea generation or unleash a force in the U.S. economy similar to the “China shock” – the period in the early 2000s when outsourcing shrunk the U.S. manufacturing base and structurally changed the U.S. labor market – is yet to be seen. However, industry valuations and capital expenditures seem to be premised on a belief that AI will deliver both.

The Second Machine Age: testing theory with practice

Until recently, the idea that AI held the power to drastically transform business operations, productivity, and the labor market was largely theoretical. It’s been over a decade since Erik Brynjolfsson and Andrew McAfee published “The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies,” which predicted task automation would enable machines to learn, reason, and create, resulting in a “great divergence” – increased displacement of white-collar jobs, widening inequality, and winner-take-all (or most) dynamics.

With the release of large language model (LLM)-based tools, including ChatGPT (released in 2022), and dramatic model improvements and widespread user adoption since, we are only now starting to see the real effects of this technology on the economy. What was theory is now turning into practice.

This year, a defining feature of the AI boom is the industry’s race to build enormous computing capacity to train these models and support an increasing number of monthly active users (MAUs). The assumption is that AI will attract billions of users (including paying subscribers) or generate significant value through non-human usage – agents, bots, enterprise bundling, and other forms of automated interaction.

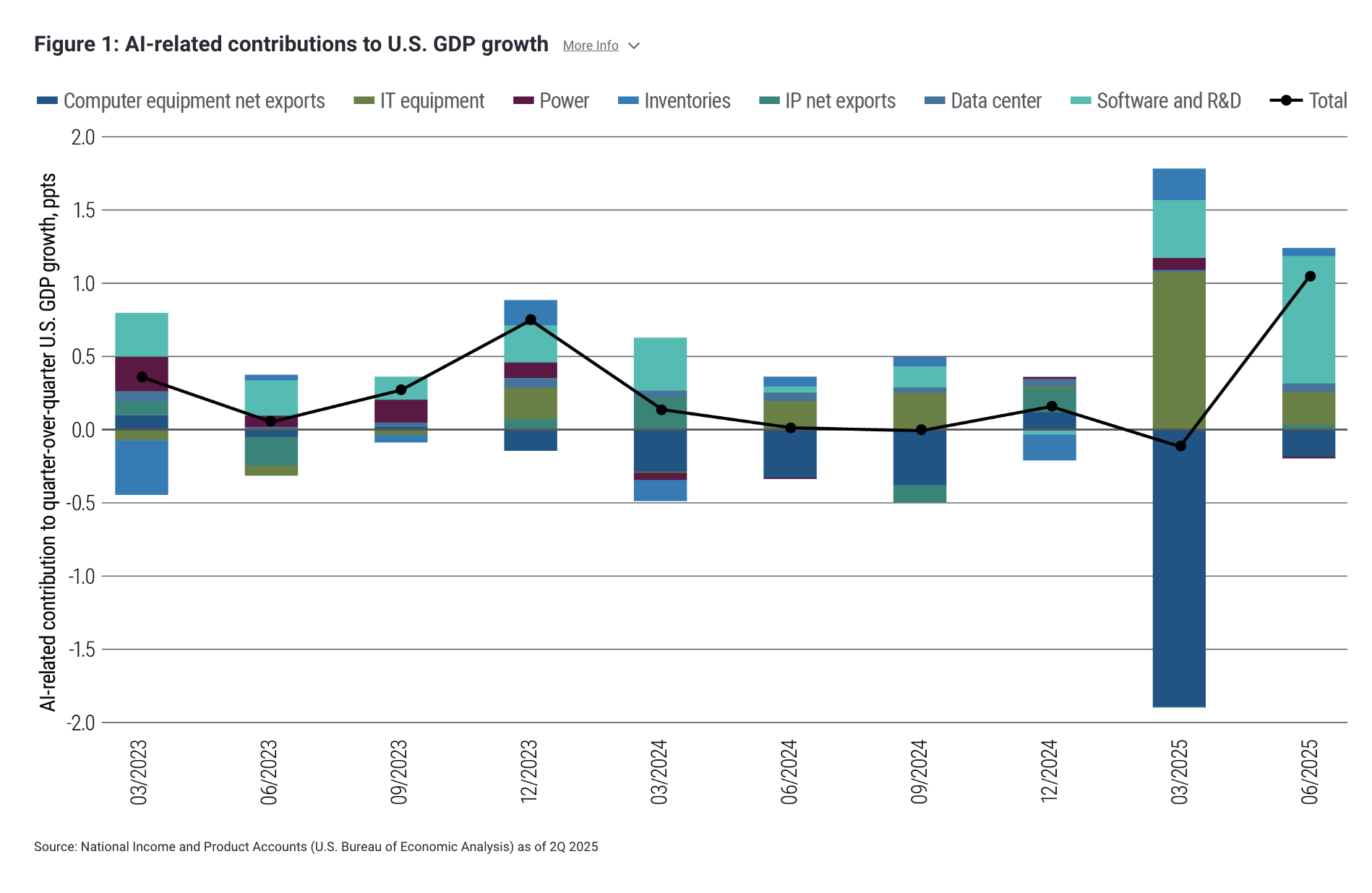

Data from the U.S. National Income and Product Accounts (NIPA) – published by the Bureau of Economic Analysis (BEA) and the basis of gross national product statistics – show that imports of computer servers and chips/GPUs have increased by $180 billion since 2023, while data center structure outlays have risen by approximately $16 billion. This roughly matches reported capital expenditures of the largest AI-related companies – the so-called hyperscalers. Capital expenditures on software, research, and development have accelerated at the same time.

Overall, AI-related investment appears to have added 1 percentage point (ppt) to economy-wide U.S. investment growth in 2025. U.S. investment trends were stagnant to contractionary otherwise. AI could have added that much to topline real GDP growth as well if the servers and infrastructure-related components weren’t imported.

Overall, we estimate that AI-related activity contributed roughly 0.5 ppts to GDP growth in the first half of 2025 (see Figure 1) – a large impulse for any one industry, and reminiscent of the 1990s fiber-optic investment boom at the advent of the internet.

Not only has the pace of investments accelerated this year, but guidance from companies suggests much more investment is yet to come. Over the next five years, total estimated investments associated with AI range in the trillions of dollars.

Building for billions of monthly active users

The rapid pace of deployment, flurry of financing deals, and sheer size of the future investment guidance has led investors to ask the question: At what point would computing capacity growth outstrip demand, resulting in elevated competition between top firms, rapid price cuts, and equity repricing?

To contextualize this question, it’s useful to translate the current dollar spending into monthly active user capacity. Using some baseline assumptions based on industry estimates – $200 billion in server capex, $350,000 per server, throughput of 2,000 tokens/sec, 50% utilization, and typical consumer usage – we calculate that current investment alone is aimed at reaching a capacity of 4.9 billion MAUs. Slight adjustments to these assumptions (i.e., faster server throughput, or more computationally intense usage) implies $200 billion in server investment can provide capacity for a range of 2 billion to 8 billion MAUs.

That’s a lot of capacity. For context, the U.S. population is about 340 million, while the world’s population is 8 billion. So the industry is either investing on the assumption that over half the world’s population will use LLMs hosted on U.S.-based servers, or that non-human users (bots, agents, enterprise software bundling) will constitute a large share of MAU demand.

Optimism appears evident in AI-related net present value

Taking the hypothetical math a step further, if each MAU generates $20/month (consumers can access some AI chatbots for free but may pay a subscription for more or faster usage, while businesses typically pay more or bundle AI with other software), 4.9 billion MAUs would yield industry revenue of approximately $1.2 trillion per year – about 4% of nominal GDP today.

Whether businesses are willing to pay $1.2 trillion annually to the AI industry depends on the value AI generates. Based on NIPA data, if labor savings were the sole benefit of AI – i.e., if AI enabled $1.2 trillion per year in economic output to shift from labor compensation to capital owners – it would require a 4-ppt decline in labor compensation’s share of aggregate gross national income to warrant these valuations.

That’s similar to the 5-ppt labor compensation share decline during the China shock from 2000 to 2010 – the period when outsourcing reduced the U.S. manufacturing base and fundamentally shifted the economy toward lower-paying services jobs. This echoes the decade-old message from Brynjolfsson and McAfee, who argued that technology’s labor displacement would occur on a scale never before seen.

We think this simple math points to a bigger assumption embedded in market valuations: that a large part of AI’s value will likely be in its ability to generate new ideas, products, and technologies (not just to make old industry more efficient), and that the AI industry will be able to capture at least some of that value.

Financing the AI boom

Aside from our simple math to put AI capacity investment in perspective, there are real questions around financing. $200 billion can generate a lot of user capacity. However, with rapid innovation, and fast depreciation of equipment, elevated replacement investment will also be needed.

Tech companies are exploring various ways to fund these ongoing investments (despite only limited reported revenue generation from LLMs so far), including banks, public and private credit, and private equity. But will these sources, especially banks, remain willing to support AI initiatives at the scale tech firms desire? And how much of the dream of greater efficiency and new ideas is dependent on additional financing?

The tech industry also currently enjoys relatively favorable treatment from the U.S. government. Servers, chips, and components are carved out from tariffs, and with upfront capital expensing on everything – including structures – hyperscalers likely won’t pay much in taxes for the foreseeable future. However, that could change in the future. Regulatory scrutiny could also increase: As the industry’s footprint grows, so does the likelihood of more rigorous oversight and potential policy shifts.

Energy constraints: the marginal cost of AI

The energy needed to fuel the AI boom has long been a central concern. The marginal cost for AI services is increasingly tied to energy consumption. Key questions include whether energy capacity can keep pace with AI’s growth, or whether AI will innovate its way around these constraints. For example, will models become more efficient and less resource-intensive?

Takeaways: AI investment hinges on pivotal new ideas beyond productivity gains

AI is a transformational general-purpose technology, and it will fundamentally change the way people work and live and the way companies find and invest in new ideas. Companies that are currently at the center of this new industrial revolution are speeding ahead with investments despite unanswered questions about the pace of advancements, the computing capacity needed to realize them, and AI industries’ ability to capture the value the technology is creating.

Which companies ultimately end up capturing the immense potential value is also uncertain, and winners and losers can change over a new technology’s adoption cycle. As AI evolves, new disrupters will likely emerge, while current market leaders may not be able to translate rapid growth to sustained earnings.

Weighing the incredible potential of AI against the risks, costs, and current valuations suggests that a lot is riding on AI’s ability to deliver. It will take transformative big ideas – lucrative new products, new forms of value creation – to justify the scale of capital expenditures and the optimism embedded in industry valuations.

As the potential for energy constraints, financing challenges, and regulatory scrutiny mounts, the question is not just how much investment is too much, but whether the industry can deliver on its promise of transformative innovation, and capture that value for its shareholders.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2025-1112-4984966

© PIMCO

Read more commentaries by PIMCO