What Zohran Mamdani’s Victory Tells Us About the State of Capitalism in America

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe problem with socialism is that you eventually run out of other people’s money.

~Margaret Thatcher

For more than a century, New York City has stood as the beating heart of global capitalism. That’s why this month’s election of Zohran Mamdani, a self-described Democratic Socialist, as the city’s next mayor has sent shockwaves through America’s business and investing community.

Mamdani, 34, will be the youngest NYC mayor in over a century and the first Muslim to hold the office. Despite having virtually no name recognition as recently as the beginning of the year, he handily defeated none other than former New York governor Andrew Cuomo, a member of the Cuomo political dynasty who was endorsed by President Donald Trump (though one can argue this hurt him more than helped him).

Tapping Into the Youth Vote

Populism has long been associated with the right—think the Trump/MAGA movement in the U.S. and Brexit in the U.K.

But now, a different kind of populism appears to be cropping up from the left. Mamdani’s progressive messaging—rent freezes, small-business support, a $30 minimum wage—clearly resonated with young, working-class voters. According to exit polls, an unbelievable 78% of New Yorkers under 30 pulled the lever for him, compared to only 18% for Cuomo.

Kevin O’Leary, aka Mr. Wonderful, places a lot of the glory (or blame, depending on your point of view) at the altar of the almighty algorithm, writing on LinkedIn that the mayor-elect “did a fantastic job of understanding social media.”

I couldn’t agree more. Older voters may roll their eyes at memes and “viral” TikTok videos, but in today’s attention economy, the algorithm has steadily grown in importance to become the be-all and end-all. That’s precisely what compelled Elon Musk to buy Twitter in October 2022, a strategy that I believe helped Trump get reelected.

Many young people have voiced mistrust in institutions, which has not only prompted them to seek candidates who are outside the norm but also decentralized assets such as Bitcoin and stablecoins.

Progressive Policies Weigh on Business

On the surface, much of Mamdani’s policy agenda sounds like a wish list for Main Street. He’s promised to cut city fines and fees for small businesses in half, including the $1,000 registration cost, and to streamline permits and digitize applications.

It’s his more progressive pledges—A $30-an-hour minimum wage by 2030! Free buses and childcare!—that have many corporations and taxpayers worried. Payroll is already the largest expense for most small businesses, typically costing them between 15% and 30% of gross revenue.

Freezing rents and nationalizing utilities might play well on social media, but these policies, while well-meaning, could have a chilling effect on private investment, construction and more.

As BCA Research put it, “Mamdani will struggle to run NYC and implement his agenda of free stuff.”

Escape from New York

Large employers are starting to get nervous. JPMorgan Chase, Goldman Sachs and Citigroup have already moved thousands of workers out of New York to Texas and Florida, where taxes are lower and regulations lighter. I suspect we’ll see more of this as Mamdani’s policies take effect.

Due mainly to taxpayers fleeing high-tax states, the Lone Star State and Sunshine State have gained a combined $250 billion in net adjusted gross income (AGI) in the past decade alone; over the same period, the Empire State has lost $111 billion, according to the National Taxpayers Union Foundation (NTUF).

Meanwhile, the Tax Foundation’s 2026 State Competitiveness Index ranks New York dead last for business taxes. With top marginal income tax rates approaching 15% when city taxes are included, high earners and corporations have yet another incentive to move elsewhere.

If the trend continues, Mamdani may preside over a smaller, poorer tax base even as he promises more spending. The top 1% of New Yorkers pay roughly 40% of the city’s income taxes, meaning even if a fraction of them leave, the fiscal consequences could be severe.

Capitalism in Decline?

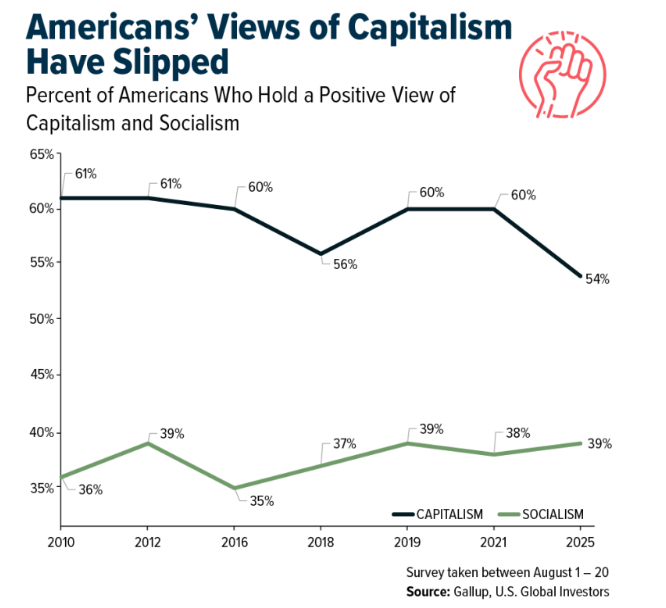

To understand Mamdani’s rise, it’s important to look at young people’s changing views of capitalism and socialism.

A recent Gallup poll found that only 54% of Americans view capitalism favorably, down from 60% a few years ago. Among Democrats, the numbers flip entirely, with more holding a positive view of socialism than capitalism, by 24 points.

That probably sounds shocking to many readers, but venture capitalist Peter Thiel put it all into context in a 2020 email that resurfaced after Mamdani’s victory: “When one has too much student debt or if housing is too unaffordable, then one will have negative capital for a long time… and if one has no stake in the capitalist system, then one may well turn against it.”

A Red-Letter Quarter for Gold Funds

For investors, I believe it’s important to keep in mind that government policy is a precursor to change. If businesses and capital continue migrating to low-tax, pro-growth states like Florida, Texas and Tennessee, investors may find opportunities in real estate, infrastructure and municipal bonds.

At the same time, sectors aligned with Mamdani’s Democratic Socialist policies—green energy, affordable housing, public transit—could see new funding streams, even if the broader business climate cools.

I’m confident that markets will adapt. In the meantime, I think it’s particularly prudent to maintain exposure to hard assets such as gold and silver, which investors have historically sought in uncertain times.

Today, that’s no exception. According to Lipper data, gold mining funds in the U.S. saw remarkable flows in the third quarter, collecting some $5.4 billion. That’s the most in a single quarter since December 2009.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.21%. The S&P 500 Stock Index fell 1.63%, while the Nasdaq Composite fell 3.04%. The Russell 2000 small capitalization index lost 1.88% this week.

- The Hang Seng Composite gained 0.82% this week; while Taiwan was down 2.06% and the KOSPI fell 3.74%.

- The 10-year Treasury bond yield rose 1 basis point to 4.094%.

Airlines and Shipping

Strengths

- UPS and Kuehne + Nagel are strengthening their global positions through targeted acquisitions. UPS expanded into high-margin medical logistics by acquiring Andlauer Healthcare Group, while Kuehne + Nagel deepened its aerospace footprint with the purchase of Ireland-based Eastway Global Forwarding. These moves consolidate leadership in specialized logistics segments, increasing vertical integration and resilience against cyclical freight fluctuations.

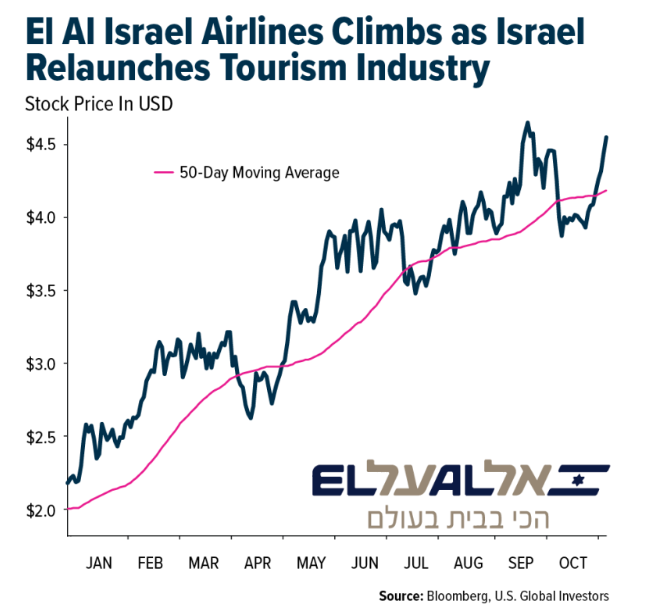

- Following the ceasefire and the lifting of travel advisories, Israel is relaunching its tourism industry with renewed optimism, marked by its return to the world travel market in London for the first time since the start of the Gaza War. The Ministry of Tourism aims to rebuild global confidence and boost arrivals particularly from the U.K. through strategic partnerships and marketing that highlight Israel’s beauty, resilience and cultural connection.

- The best-performing airline stock for the week EL Al Israel, up 11.66%. As mentioned above, Israel is relaunching its tourism industry, and the stock is seeing renewed optimism, leading to positive sentiment.

Weaknesses

- The deadly crash of a 34-year-old UPS MD-11 cargo plane near Louisville, Kentucky, has shaken the global aviation sector and raised questions about the safety of aging freighter fleets. Investigators confirmed the left engine detached mid-air before impact, killing at least 12 people, including civilians on the ground. The aircraft had undergone heavy maintenance just weeks earlier, reigniting debate over the operational risks of extending the service life of older converted jets still widely used in cargo operations.

- Ocean freight remains a structural weak spot. Expeditors reported a 3% decline in ocean volumes and falling rates due to overcapacity and weaker import demand, with analysts expecting continued pressure through 2026 until global capacity realigns with slower trade growth.

- The worst-performing airline stock for the week was Qantas Airways, down 6.76%, as the stock slid to a six-month low following the airline trimming its revenue outlook.

Opportunities

- President Trump’s plan to replace the U.S. air traffic control system within six weeks could open significant new government contract opportunities for defense, aerospace and technology firms. This modernization effort may accelerate digitalization in air infrastructure and create a multi-year investment cycle across both civil and defense aviation sectors.

- The return of Austrian Airlines and Lufthansa flights to Tehran, along with Israel’s tourism revival following the ceasefire, signals a reawakening of air travel across the Middle East and Mediterranean. These developments could restore critical routes and spur a rebound in international demand through 2026.

- DHL and Maersk continue to set new sustainability benchmarks in Asia. DHL opened its first fully solar-powered warehouse in Thailand, while Maersk launched its largest Asia-Pacific distribution center in Malaysia, expanding local warehouse capacity by more than 30%. Both projects reflect a structural shift toward low-carbon, energy-efficient logistics and reinforce Asia’s position as a global supply chain hub.

Threats

- American Airlines reported a $114 million quarterly loss and announced layoffs across multiple departments, revealing ongoing inefficiencies and rising cost pressures in the U.S. legacy carrier segment. The company’s inability to translate record revenue into profit illustrates the structural challenges of the traditional hub-and-spoke model.

- The ongoing government shutdown has triggered phased flight reductions, starting with 4% of flights cut at 40 major airports between Friday and Sunday and potentially reaching 10% next week, according to Raymond James. The FAA is prioritizing protection of international and long-haul routes, but the disruption highlights the industry’s vulnerability to federal labor shortages. Analysts note the earnings impact should remain modest unless the shutdown extends into the Thanksgiving travel period.

- Rising taxes, airport fees and inflation in France and the Netherlands are eroding the profitability of Air France-KLM and forcing the group to reassess KLM’s operating model. The surge in costs at Amsterdam Schiphol Airport, now up 41% year-over-year, reflects a broader cost crisis that could undermine European competitiveness.

Luxury Goods and International Markets

Strengths

- Mercedes shares hit a 52-week high this week, boosted by strong electric vehicle sales and a share buyback program that improved investor confidence. Positive analyst ratings and solid financial results also helped lift the stock price.

- Tapestry reported strong results this week for the first quarter of fiscal 2026. The company posted revenue of $1.7 billion, a 13% increase from the same period last year, driven by double-digit growth at its Coach brand. Earnings per share rose to $1.38, beating analyst expectations. Tapestry also raised its full-year earnings guidance, signaling confidence in continued growth. The company added 2.2 million new customers globally, with Gen Z making up about 35% of the new customer base.

- Somnigroup International, the world’s largest bedding company, led the S&P Global Luxury Index with a 14% gain this week. The rise was driven by strong third-quarter results, including a 63% increase in net sales fueled by the Mattress Firm acquisition and international growth. The company raised its full-year earnings guidance, boosting investor confidence and lifting the stock.

Weaknesses

- Barclays has downgraded Hermes International from Overweight to Hold, citing fewer short-term catalysts to drive the shares despite the brand’s strong reputation. The bank lowered its price target, expecting Hermes’ revenue outperformance to narrow in 2026 as the broader luxury sector rebounds.

- Norwegian Cruise Line shares have fallen this week despite the company reporting an earnings per share (EPS) beat for the third quarter. The stock declined amid investor concerns over revenue misses and cautious outlooks, reflecting mixed sentiment despite the positive EPS surprise.

- Cettire Cettire, an Australian online retailer of luxury goods, was the worst-performing stock in the S&P Global Luxury Index this week, falling 22.4%. Year-to-date, shares are down more than 60%, pressured by ongoing concerns about weak sales growth, declining active customers, and continued challenges in the U.S. market highlighted in recent trading updates.

Opportunities

- The recent meeting in Malaysia marked a positive step toward easing the tariff war between the U.S. and China. Following the talks, China agreed to reduce tariffs on several agricultural products imported from the U.S., signaling a move toward more constructive trade relations. There is growing optimism that the trade war between the U.S. and China is easing, at least for the time being.

- Marriott reported a revenue beat for the third quarter, driven by a particularly strong performance in the luxury category. The luxury segment was the strongest performer, significantly outpacing other areas, while international markets showed moderate growth of 2.6%. In contrast, the U.S. and Canada experienced the weakest performance. Marriot is expanding its luxury portfolio, with over 260 luxury hotels and resorts in development and more than 30 properties expected to open in 2025.

- Ferrari has reported stronger-than-expected third quarter results, with net revenues rising 7.4% year-over-year to €1.77 billion and operating profit increasing 7.6% to €503 million. The company also revised its full-year guidance upward, projecting net revenues of at least €7.1 billion. This positive outlook presents an opportunity for Ferrari’s share price to recover after experiencing a sharp drop last month.

Threats

- The current U.S. government shutdown has become the longest in American history. This threatens consumer confidence and disrupts daily life across the country. Thousands of federal employees have missed paychecks, critical services remain halted and essential sectors like air travel face significant staffing shortages, raising concerns about further chaos if the shutdown continues.

- Goldman Sachs and Morgan Stanley have both issued warnings that the stock market could face a correction of 10% to 20% within the next 12 to 24 months. Speaking at the Global Financial Leaders’ Investment Summit, Goldman Sachs CEO David Solomon noted that such pullbacks are a normal part of market cycles and advised investors to stay focused on long-term goals. Meanwhile, Morgan Stanley CEO Ted Pick described corrections of 10% to 15% as “healthy” market behavior. Both firms highlighted concerns over stretched valuations.

- China’s recent change in tax policy on gold purchases, effective November 1, 2025, has ended a long-standing value-added tax (VAT) credit benefit for gold buyers, including jewelry retailers. This removal of tax incentives increases the cost of procuring gold by about 7 percentage points in VAT, pressuring Chinese jewelry retailers like Laopu Gold and Chow Tai Fook. This government action may lead to price increases that could dampen consumer demand.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was natural gas, up 4.75%, but crude oil actually slid 1.85%, likely on weaker economic headlines. Natural gas, in contrast, continued its second strong weekly gain with a surge in LNG export demand driving the price.

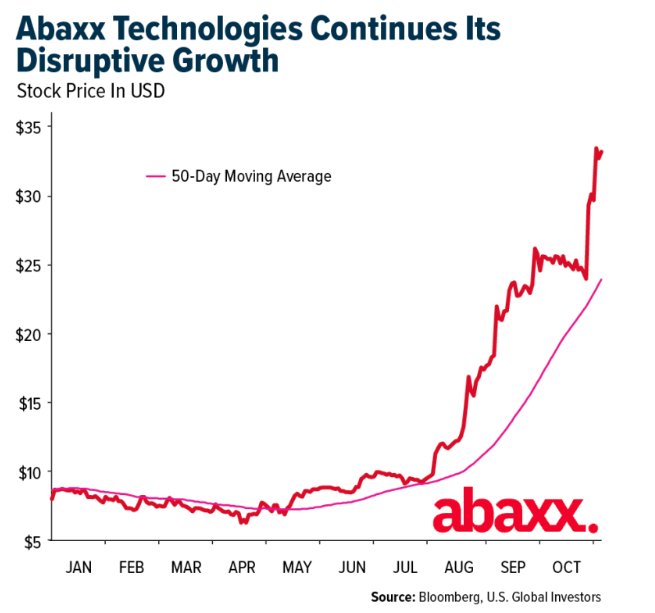

- Abaxx Technologies, now officially added to the MSCI Canada Index effective November 5, 2025, is rapidly emerging as a next-generation exchange and clearinghouse for physically delivered LNG, carbon, and precious metal contracts built on instant T+0 digital settlement infrastructure. The company’s upcoming earnings report next week is expected to reveal the average contract value traded for the first time, a key metric that could offer investors deeper insight into liquidity growth and institutional adoption across its newly launched markets.

- Aluminum prices climbed to their highest level since November 2024 on the Shanghai Futures Exchange as strong demand from China’s new energy vehicle and solar sectors tightened market conditions. Shares of major aluminum producers, including Chalco and Shandong Nanshan Aluminum, surged by the daily 10% limit amid optimism over sustained supply shortages and robust domestic consumption.

Weaknesses

- The worst performing commodity for the week was uranium, which was down 6.08%. Uranium prices sold off as investors grew wary that accelerating mine restarts and new projects could create a temporary oversupply before the next wave of nuclear power plants comes online. Despite policy tailwinds like the U.S. adding uranium to its Critical Minerals List, the market remains shaky as demand growth is still contingent on reactors that are years away from completion.

- U.S. manufacturing activity contracted for an eighth consecutive month in October, with the ISM Index slipping to 48.7 as weak production and hiring persisted amid trade uncertainty. While inflation pressures eased, with input costs falling to their lowest since early 2025, factories continue to face sluggish demand and cautious sentiment, particularly across textiles, apparel and furniture industries.

- UK construction activity contracted at its fastest pace since the pandemic, with the October PMI dropping to 44.1, underscoring deep weakness in housing and infrastructure projects despite Labour’s push to spur investment. Residential and civil engineering work both slumped sharply, though optimism improved slightly on expectations that the Bank of England may cut rates in December.

Opportunities

- Tanzania has reopened its border with Zambia, restoring the vital trade corridor for copper and cobalt exports from Zambia and the Democratic Republic of Congo after post-election unrest halted shipments last week. Authorities are now clearing roughly 250 trucks per day in each direction through the Dar es Salaam route, a key hub for African mineral exports to China and regional fuel imports.

- Sweden’s parliament voted to lift its 2018 ban on uranium mining, classifying uranium as a “concession mineral” vital to national interests as the country expands its nuclear power capacity. The new legislation, set to take effect January 1, will also ease permitting rules for activities involving small amounts of uranium.

- After nearly three decades of delays, Guinea’s massive Simandou iron ore project—valued at $23 billion—has finally begun transporting ore, marking a new era for one of the world’s richest untapped mineral deposits. The development, dominated by Chinese firms alongside Rio Tinto, is set to reshape global iron ore markets, bolster Guinea’s economy, and give Beijing unprecedented leverage over pricing in a commodity critical to steelmaking.

Threats

- A wave of corporate layoffs across major U.S. companies — from Starbucks and Target to Amazon and Paramount — is raising concerns that job cuts are shifting from isolated cases to a broader trend amid slowing demand and rising automation. Economists note that while overall jobless claims remain stable, the scale and pace of cuts suggest businesses are shedding labor to protect margins, signaling a potential cooling in the labor market.

- Rising utility bills and data center energy demand have become a major political issue in the U.S., influencing recent elections in New Jersey, Virginia, and Georgia, where voters backed candidates pledging to rein in electricity costs. Analysts say soaring power prices have turned into a household-level concern, reshaping energy policy debates ahead of next year’s congressional elections.

- China is accelerating its $468 billion push for energy self-sufficiency, with PetroChina, Sinopec, and Cnooc ramping up domestic oil and gas production to record levels amid rising geopolitical tensions and U.S. trade pressure. Offshore output from the Bohai Sea now accounts for about 10% of national production, underscoring Beijing’s drive to secure its “rice bowl of energy” and reduce dependence on foreign supplies as demand growth slows.

Bitcoin and Digital Assets

Strengths

- Bitcoin is showing renewed structural strength as institutional and corporate adoption deepens. JPMorgan’s valuation model now places its fair value near $170,000, and major banks are expanding its use as collateral. This shift marks Bitcoin’s transition from a speculative asset to a recognized macro hedge and liquidity instrument within global finance.

- Michael Saylor’s Strategy Inc. successfully raised €620 million in Europe through its new 10% “Stream” preferred shares, demonstrating that even amid market volatility, investor appetite for crypto-linked instruments remains strong and globally diversified.

- Google’s integration of prediction market data from Polymarket and Kalshi into Search and Google Finance underscores how major tech firms are normalizing blockchain-based data in mainstream financial tools, strengthening crypto’s informational legitimacy.

Weaknesses

- Investor sentiment in digital assets remains fragile as broad market selloffs, regulatory uncertainty and leadership inconsistency across the sector continue to undermine confidence and long-term positioning.

- Enforcement actions, such as the five-year prison sentence for Samourai Wallet’s developer, highlight the ongoing legal risks facing privacy-oriented crypto projects and the thin line between innovation and regulatory violation.

- Balancer suffered a major security breach, with hackers draining roughly $128 million in digital assets, according to Cyvers. This marks a hit to a protocol that previously managed more than $700 million in total value. Security firms say the exploit stems from compromised access controls allowing direct balance manipulation, while Balancer’s engineering teams work to regain control and stem the ongoing drain.

Opportunities

- Regulated Bitcoin and stablecoin products are maturing across major economies, from Japan’s stablecoin trials to Anchorage’s institutional DeFi custody, expanding compliant gateways for traditional investors to enter crypto finance.

- AI-driven and tokenized data services, as seen with Google’s revamped finance platform, could accelerate the convergence of predictive analytics, digital assets and real-world financial applications.

- A potential resolution to the government shutdown could spark a short-term rally across risk assets, with analysts projecting Bitcoin gains of 5% or more within 48 hours of a deal.

Threats

- International oversight of crypto assets remains fragmented, with the Financial Stability Board warning of significant regulatory gaps that could create systemic risks and delay global integration.

- European authorities dismantled a massive cryptocurrency money laundering ring that generated $688 million in illicit proceeds, arresting nine suspects across Belgium, Cyprus, France, Germany and Spain. The operation seized over $1.7 million in assets, highlighting Europol’s push for advanced cross-border tools and collaboration to combat increasingly sophisticated crypto crimes.

- Cathie Wood said stablecoins are increasingly taking over functions once expected of Bitcoin, such as payments and savings, especially in emerging markets. As a result, ARK Invest trimmed about $300,000 from its long-term Bitcoin bull case, though Wood emphasized that Bitcoin remains the core “digital gold” of a new monetary system.

Defense and Cybersecurity

Strengths

- Nvidia is ramping up investments in Germany as it partners with Deutsche Telekom to launch a €1 billion sovereign AI cloud project, aiming to make Germany one of the world’s leading AI markets. This strengthens Nvidia’s footprint in Europe and supports the region’s technological independence in AI infrastructure.

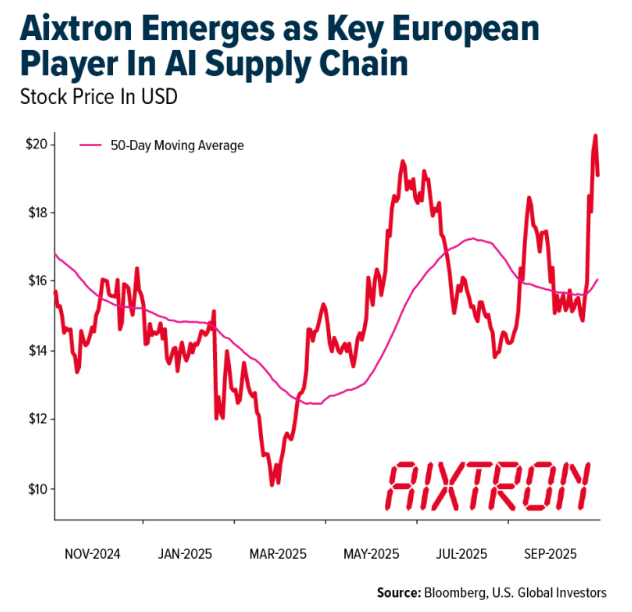

- Aixtron is emerging as a key European player in the AI supply chain, with growing confidence that its compound semiconductor technology will become essential for powering next-generation data centers. The company expects strong medium-term demand as AI infrastructure accelerates, positioning it for renewed growth momentum from 2027 onward.

- The best performing stock this week was Carpenter Technology, rising 3.54% after management reported strong demand across key end markets, particularly in aerospace, where order intake reached its highest level in over a year. With operating income up 31% year-over-year and management guiding for continued growth through 2027, the company’s high operating leverage positions it to convert revenue gains into significant margin expansion.

Weaknesses

- The Adeia lawsuit against AMD creates legal and operational uncertainty across the semiconductor sector. Ongoing litigation over hybrid bonding and process node patents could delay innovation and impact AMD’s partnerships and product rollout.

- Nvidia’s inability to ship AI chips to China limits access to a major market. The company remains dependent on U.S. regulatory changes and geopolitical conditions before any reentry becomes possible, restricting short-term revenue growth.

- The worst performing stock in the XAR ETF this week was , which declined -% after

Opportunities

- Microsoft and IREN signed a $9.7 billion AI infrastructure agreement, with Dell supplying $5.8 billion worth of hardware. This reflects the ongoing surge in global demand for AI computing capacity and opens new opportunities for suppliers across data centers and semiconductor manufacturing.

- Kratos’ acquisition of Israel’s Orbit Technologies for $356 million strengthens its satellite communication and electronic warfare portfolio. The deal supports expansion into space defense systems and aligns with rising demand for low-cost autonomous platforms.

- The UK and Germany have started a joint program to develop a 2,000-kilometer, long-range precision missile that will exceed Storm Shadow and Taurus capabilities. The initiative enhances NATO’s deterrence capacity and fuels industrial collaboration across Europe’s defense sector.

Threats

- Rising U.S.–Mexico tensions over potential military operations against drug cartels could strain diplomatic relations and disrupt cross-border logistics and trade security.

- Fortinet’s FortiGuard Labs uncovered the TruffleNet campaign using stolen AWS credentials in large-scale email compromise attacks. This exposes persistent cybersecurity vulnerabilities across critical AI and cloud infrastructure.

- The expansion of U.S. tethered radar systems in the Caribbean reflects increasing regional security concerns. Heightened surveillance and defense activity may indicate growing instability and potential for geopolitical escalation.

Gold Market

This week gold futures closed the week at $4,014.10, up $17.60 per ounce, or 0.44%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.10%. The S&P/TSX Venture Index came in off 8.53%. The U.S. Trade-Weighted Dollar fell 0.30%.

Strengths

- The best-performing commodity for the week was gold, up 0.44%. Gold rose as investors sought safety amid mounting concerns over the U.S. economy and uncertainty surrounding the prolonged government shutdown. Supported by expectations of rate cuts, falling bond yields and continued central bank demand—including China’s 12th consecutive month of purchases—the metal remains on track for its best yearly performance since 1979 despite recent volatility.

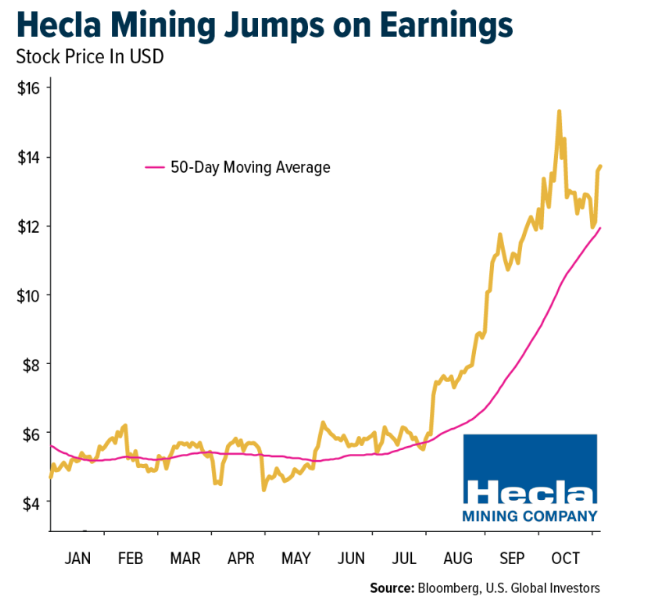

- Hecla Mining surged 12% after reporting a blowout third quarter, with sales of $409.5 million (vs. $310.8 million estimated), silver output of 4.59 million ounces and adjusted EBITDA of $195.7 million, marking strong performance across its portfolio. The company raised 2025 capital guidance for Keno Hill to $48 – $54 million as mine development runs ahead of schedule, tightened Lucky Friday’s silver production range to 4.9 – 5.1 million oz, and reaffirmed 2025 cost guidance, with all four operating assets generating positive free cash flow for a second straight quarter.

- Gold steadied near $4,000 an ounce as markets digested China’s decision to end a long-standing value-added tax rebate for gold retailers, a move expected to weigh on jewelry and industrial demand in the world’s largest consumer market. While analysts see the change pressuring sentiment and margins for Chinese jewelers, gold’s broader uptrend remains supported by central bank buying and safe-haven flows, keeping prices resilient despite softer retail demand.

Weaknesses

- The worst-performing precious metal this week was palladium, which fell 2.65% amid a broader correction in the group. Prices slipped as ETFs continued to offload holdings, adding pressure to an already soft market. The sustained outflows reflected investor rotation into silver and waning speculative interest in the auto-catalyst metal amid concerns over slowing industrial demand.

- SSR Mining shares fell sharply after reporting lower-than-expected gold output at its Seabee and Marigold mines and guiding full-year 2025 production to the bottom of its range, with costs trending higher. However, the company still beat analyst consensus estimates on both revenue ($385.8 million vs. $369.8 million expected) and EPS ($0.34 vs. $0.30 expected), supported by higher realized gold and silver prices.

- B2Gold’s latest results fell short of expectations, with downward revisions heading into earnings and a miss on consensus estimates as the company underperformed both gold and silver benchmarks in revenue and free cash flow per share quarter-over-quarter. However, it posted year-over-year gains in both metrics, reflecting modest operational recovery despite near-term execution challenges and weaker quarterly momentum.

Opportunities

- The Coeur acquisition of New Gold underscores a growing trend of consolidation in the gold sector, as producers race to expand reserves and secure low-cost, long-life assets amid a constrained project pipeline. The deal is immediately accretive to Coeur’s NAV, operating cash flow and free cash flow per share, signaling renewed M&A momentum as mid-tier miners pursue scale and stronger financial positioning ahead of a potential gold upcycle.

- Founders Metals announced a C$50 million strategic investment from Gold Fields, which will acquire 12 million shares at C$4.15 each through a non-brokered private placement to fund land consolidation and exploration at the Antino Gold Project in Suriname. The agreement includes investor rights granting Gold Fields board representation and technical collaboration privileges, underscoring the project’s growing profile as one of the most advanced gold exploration assets in the Guiana Shield.

- Torex Gold unveiled its first capital return program, combining a C$0.15 quarterly dividend with ongoing share repurchases to reward shareholders following the successful ramp-up of its Media Luna project and a return to strong free cash flow. CEO Jody Kuzenko said the initiative marks the beginning of a broader capital return strategy set to expand through 2026, supported by Torex’s solid balance sheet, debt reduction goals, and continued investment in Morelos, Los Reyes and exploration growth across Mexico and Nevada.

Threats

- As of November 7, 2025, both gold and silver remain in correction, with gold stabilizing around $3,900–$4,000 per ounce and silver near $48.60 per ounce, down roughly 14% from its peak versus gold’s 9% decline. Silver’s higher beta continues to amplify moves in either direction, and with more than 80% of its value still correlated to gold, portfolios long gold and short silver remain better positioned amid ongoing volatility.

- Fortuna Mining faces mounting cost pressures, with all-in sustaining costs (AISC) rising to $1,987 per ounce in Q3 2025 from $1,932 per ounce in the prior quarter, driven by higher royalties, consumables and maintenance expenses. This trend threatens to compress margins and weaken free cash flow, particularly as the company reinvests heavily in exploration and development projects such as Diamba Sud, limiting its ability to offset escalating operating costs.

- Galiano Gold’s operations are under strain from rising tax burdens in Ghana, including a recent 2% increase to the Growth and Sustainability Levy, which is expected to raise royalties and push AISC toward $2,200–$2,300 per ounce. The temporary shutdown at the Esaase deposit further compounds pressure on margins and guidance, as lower-grade stockpiles replace mined ore, threatening near-term production stability and free cash flow.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2025):

United Parcel Service Inc.

Kuehne + Nagel International

El Al Israel Airlines

Deutsche Lufthansa AG

Deutsche Post AG

AP Moller-Maersk A/S

American Airlines Group Inc.

Air France-KLM

Mercedes-Benz Group AG

Hermes International SCA

Norwegian Cruise Line Holdings

Ferrari NV

The Goldman Sachs Group Inc.

NVIDIA Corp.

Microsoft Corp.

Dell Technologies Inc.

Abaxx Technologies

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

MSCI Canada Index: A market capitalization–weighted index designed to measure the performance of the large- and mid-cap segments of the Canadian equity market.

ISM Index: A monthly economic indicator published by the Institute for Supply Management that measures U.S. manufacturing and service sector activity based on surveys of purchasing managers.

The State Tax Competitiveness Index evaluates how well states structure their tax systems and provides a road map for improvement.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Read additional important information. +

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All